This is the story of the Phillips curve—the supposed tradeoff between inflation and unemployment—and decades of policymaking based on it.

What if it was all wrong? What if there is no simple, law-like relationship between unemployment and inflation?

🧵

apricitas.substack.com/p/the-life-dea…

What if it was all wrong? What if there is no simple, law-like relationship between unemployment and inflation?

🧵

apricitas.substack.com/p/the-life-dea…

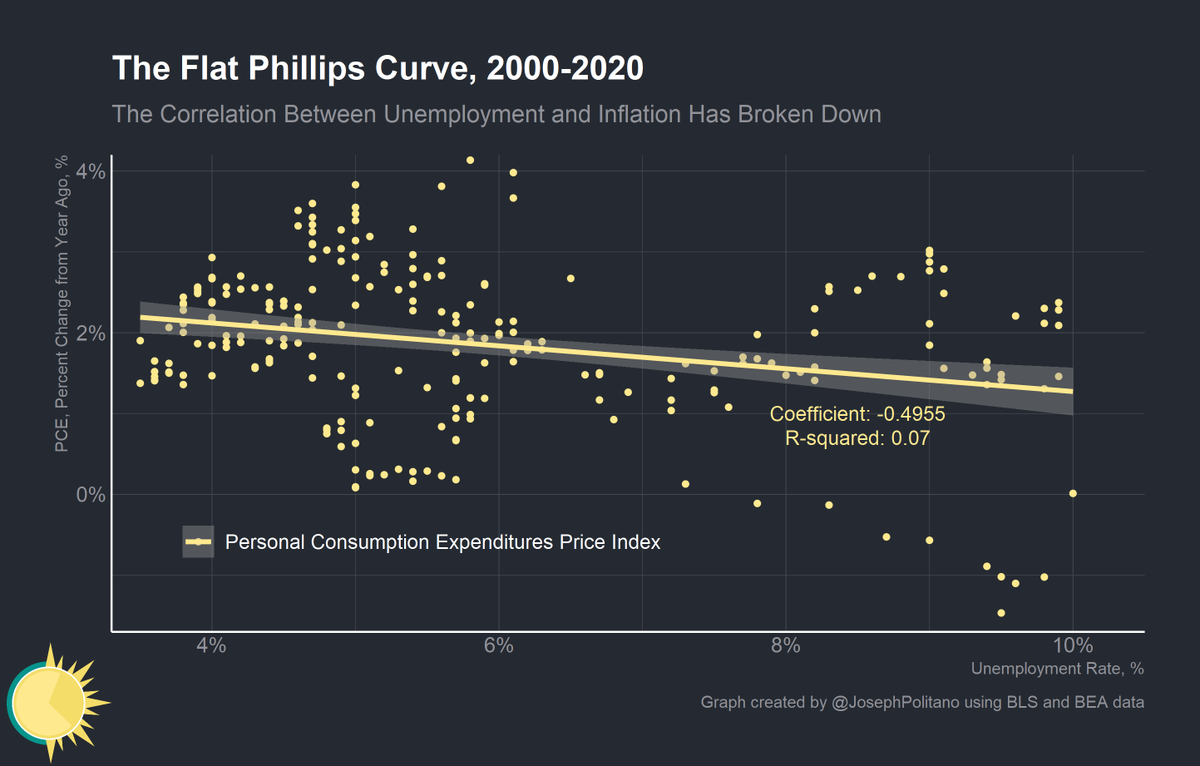

For the last twenty years, the observed Phillips curve relationship in the United States has been extremely flat. In other words, the unemployment rate no longer seems to predict inflation the way it previously did. This has lead many to declare the Phillips curve dead.

But what if it was always dead? Hazell, Herreño, Nakamura, and Steinsson constructed state level price indexes of non-tradeable goods to measure the Phillips curve at different points in time.

Their results? A Phillips curve that is consistently flat!

Their results? A Phillips curve that is consistently flat!

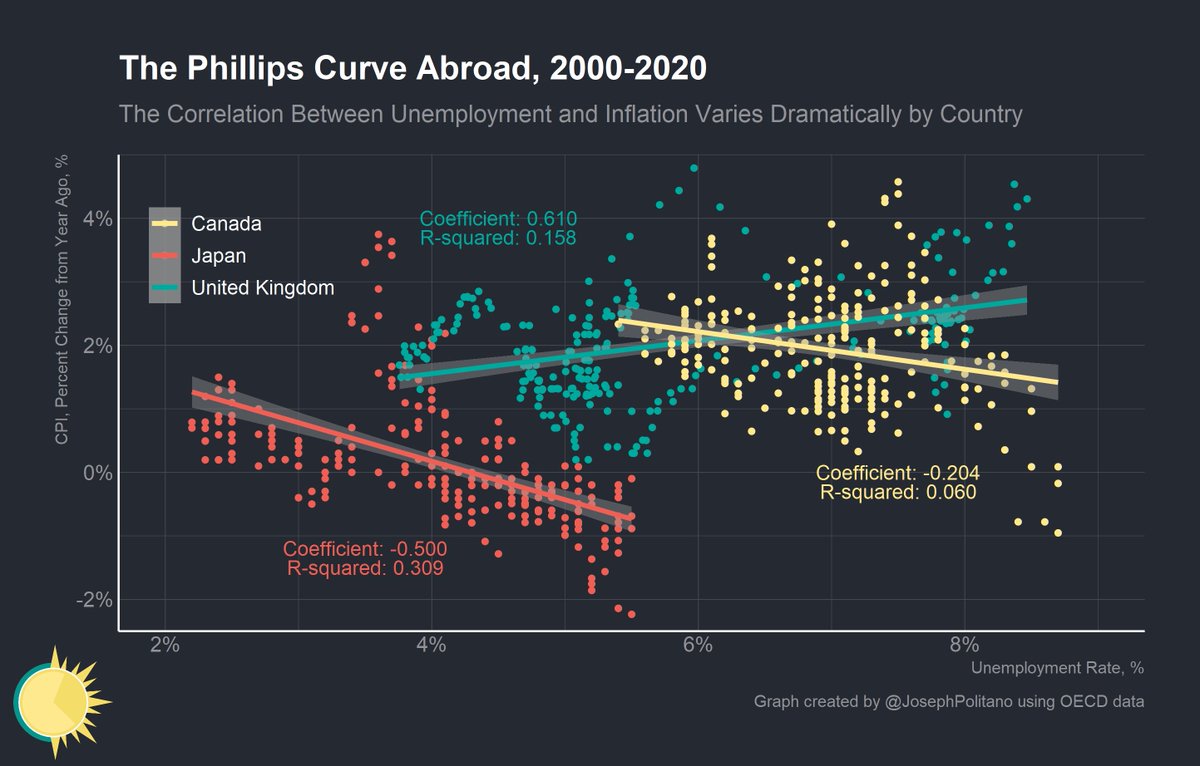

This makes more sense when we examine countries outside the US.

The Phillips curve relationship is not stable across countries or time periods, making it a terrible way to predict variation in inflation!

The Phillips curve relationship is not stable across countries or time periods, making it a terrible way to predict variation in inflation!

This hasn't stopped central banks from codifying the Phillips curve in their economic models and measures. The Federal Reserve's use of the "Non-accelerating inflation rate of unemployment" is based on the Phillips curve supposition that too low unemployment will spur inflation.

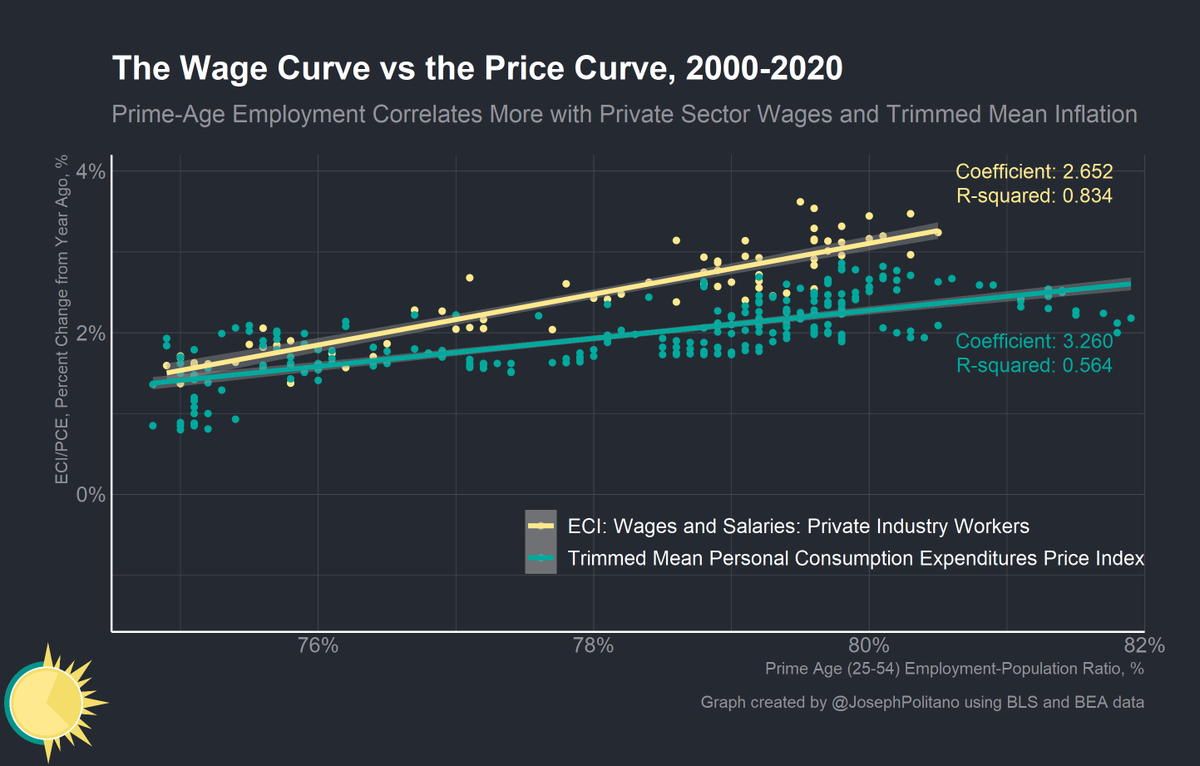

However, using a better measure of labor utilization we can see that the relationship between employment and wage growth is much stronger than the relationship between employment and inflation

High real wage growth is therefore strongly correlated with tight labor markets!

High real wage growth is therefore strongly correlated with tight labor markets!

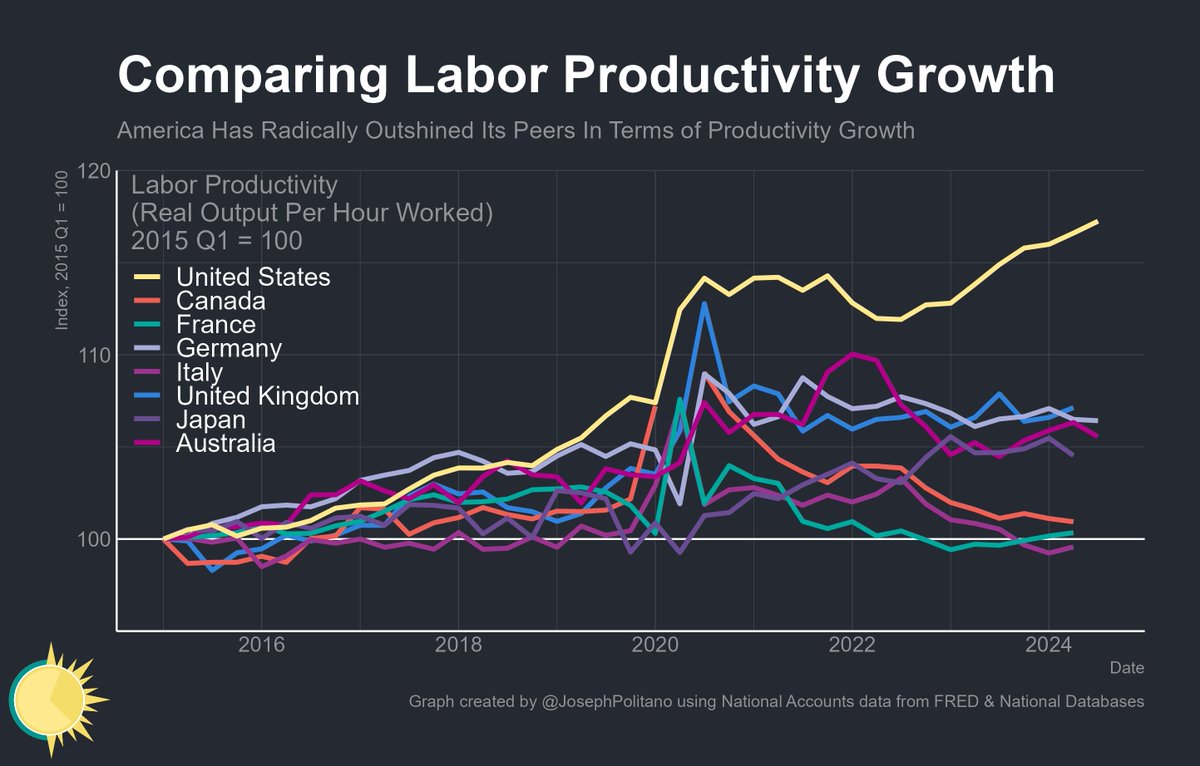

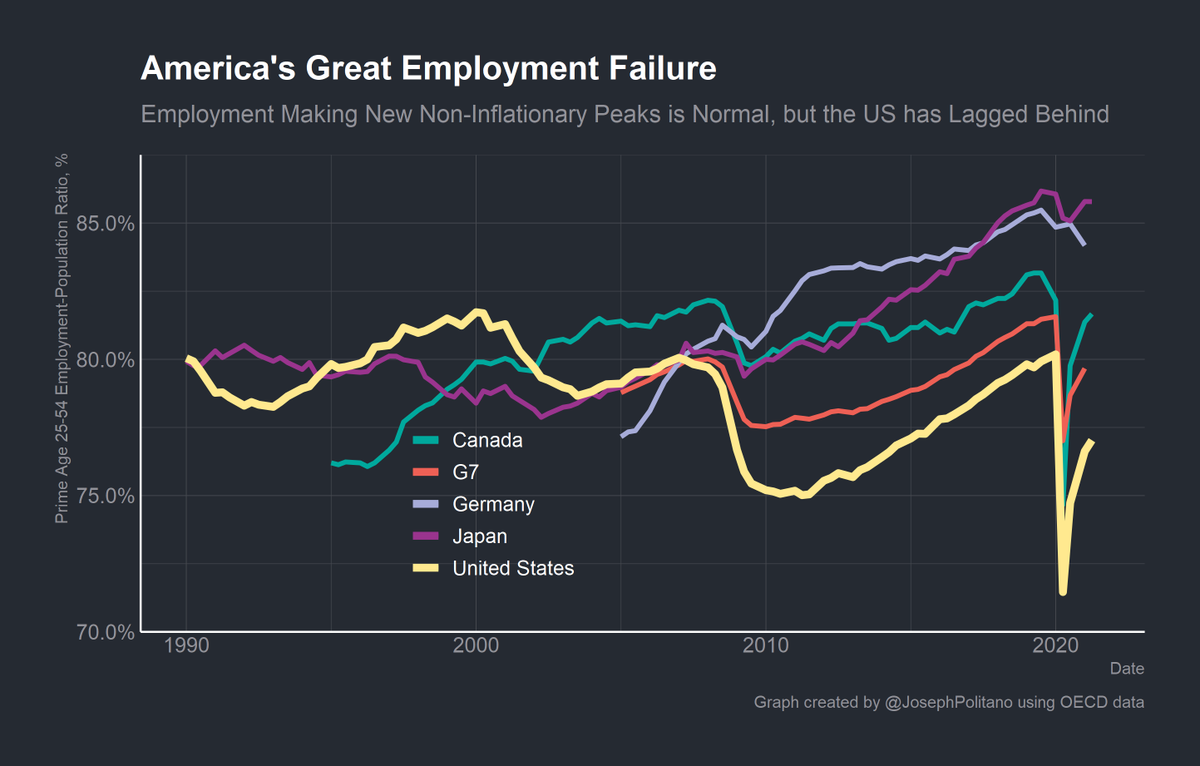

Employment is a proxy for labor utilization which itself is a proxy for capacity utilization. In the long run, we shouldn't expect any relationship between employment and inflation to hold—which is why other nations have achieved higher employment levels without higher inflation.

If we want to achieve full employment, we should focus on keeping nominal income growth stable at its maximum value. We should never worry about unemployment getting "too low." Policymakers ought to abandon attempts to divine "natural" rates of unemployment.

If you like what I write, consider subscribing! It's free and helps me out a ton.

I wouldn't be able to write this newsletter without the support and feedback of my readers.

apricitas.substack.com

I wouldn't be able to write this newsletter without the support and feedback of my readers.

apricitas.substack.com

• • •

Missing some Tweet in this thread? You can try to

force a refresh