Squeeth is a new DeFi primitive. It's an extension of everlasting options and as a power perpetual, it has characteristics similar to perpetual swaps.

Let's take a look at perpetual swaps and everlasting options to better understand squeeth! 😎

h/t @_Dave__White_ @AlexisGauba

Let's take a look at perpetual swaps and everlasting options to better understand squeeth! 😎

h/t @_Dave__White_ @AlexisGauba

Perpetual Swaps:

A perp swap allows people to bet on the potential increase or decrease of the price of an asset (eg ETH).

• If you are long the perp swap, you think the price of ETH will go up

• If you are short the perp swap, you think the price of ETH will go down

A perp swap allows people to bet on the potential increase or decrease of the price of an asset (eg ETH).

• If you are long the perp swap, you think the price of ETH will go up

• If you are short the perp swap, you think the price of ETH will go down

Each day the perp swap updates to reflect the new price of ETH, which it fetches from an oracle (eg price of ETH on a spot exchange like Coinbase). Depending on supply/demand for the perps, long-holders pay short-holders or short-holders pay long-holders to hold the position.

Example: ETH is currently at $2000 and the price of the perp swap is $2500

In this case, there is an arbitrage that exists where I could buy ETH for $2000 and sell the perp swap to get $2500, earning $500. Thus, in this case the longs pay $500 to the shorts.

In this case, there is an arbitrage that exists where I could buy ETH for $2000 and sell the perp swap to get $2500, earning $500. Thus, in this case the longs pay $500 to the shorts.

Example: ETH is currently at $2000 and the price of the perp swap is $1800

Then there is an arbitrage that exists where I could buy the perp swap for $1800 and sell ETH for $2000, earning $200. Thus, in this case the shorts pay $200 to the longs.

(arb is a bit more complicated)

Then there is an arbitrage that exists where I could buy the perp swap for $1800 and sell ETH for $2000, earning $200. Thus, in this case the shorts pay $200 to the longs.

(arb is a bit more complicated)

The previous (slightly oversimplified) examples hold by the no-arbitrage rule, which means that if there is an arbitrage that exists, people will execute it until it no longer exists, since people receive "free money."

Introducing some terminology, we call the price of the perp *Mark* and the price of ETH *Index*

This means that Funding = Mark - Index

And as we saw in the above example:

• if Mark > Index, the longs pay the shorts

• if Index > Mark, the shorts pay the longs

This means that Funding = Mark - Index

And as we saw in the above example:

• if Mark > Index, the longs pay the shorts

• if Index > Mark, the shorts pay the longs

How do we get the Mark of a perp swap, aka its price?

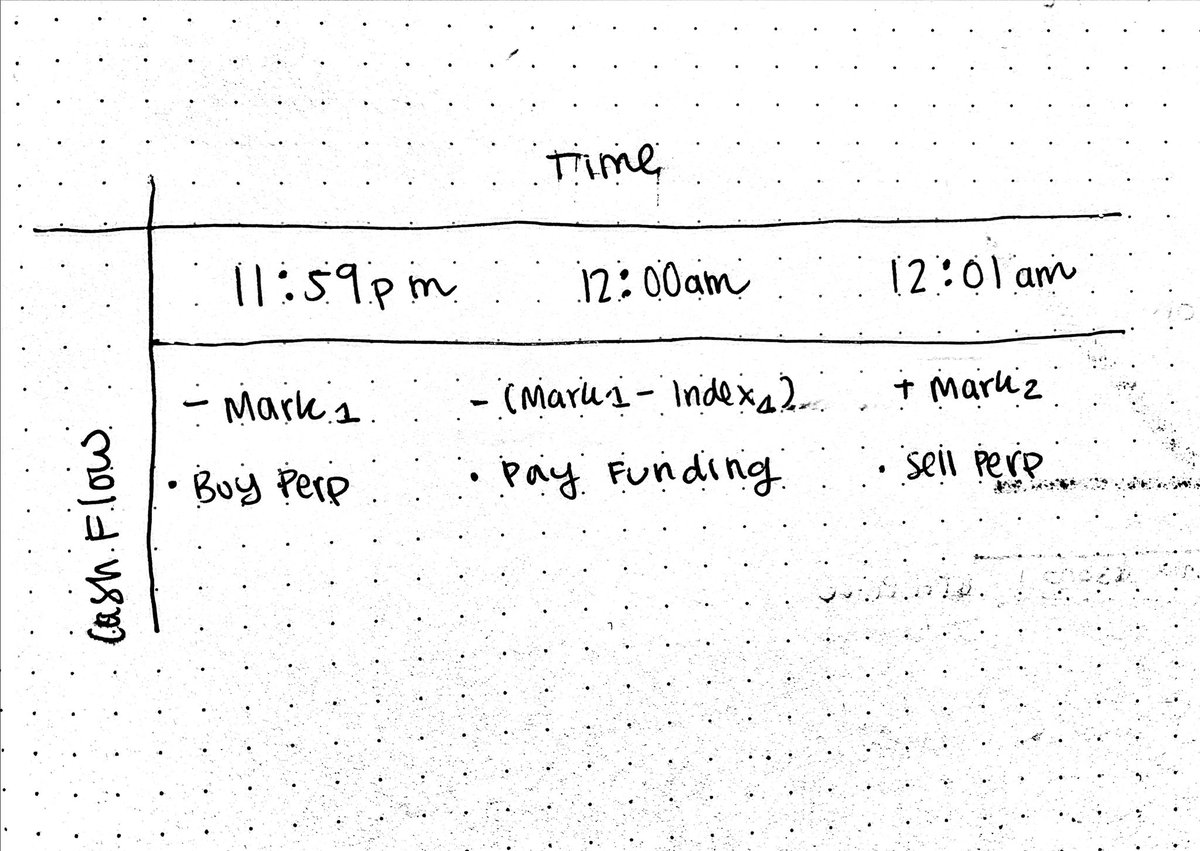

Consider the below example of buying a perp one minute before expiry, paying funding at expiry, and selling the perp one minute after expiry

For the no-arbitrage rule to hold, the result must be a payoff of 0.

Consider the below example of buying a perp one minute before expiry, paying funding at expiry, and selling the perp one minute after expiry

For the no-arbitrage rule to hold, the result must be a payoff of 0.

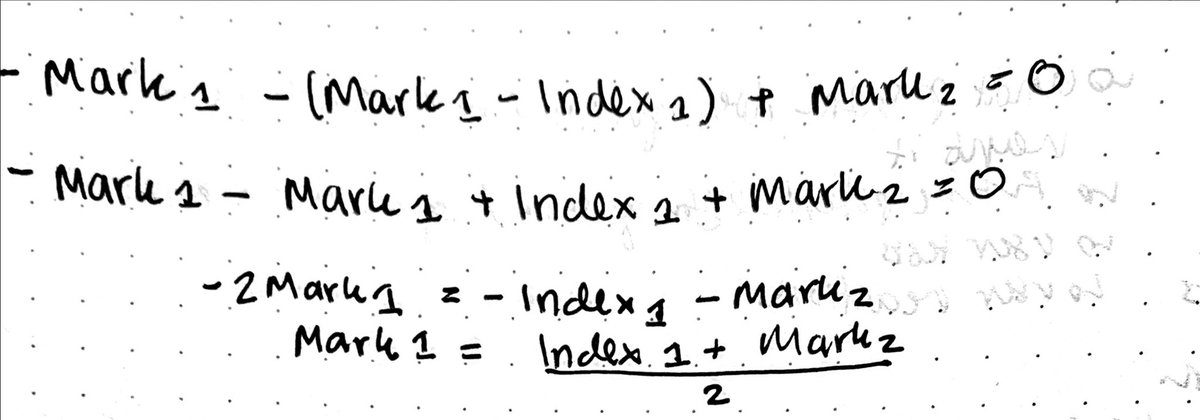

Solving for a Mark₁, we get (first photo)

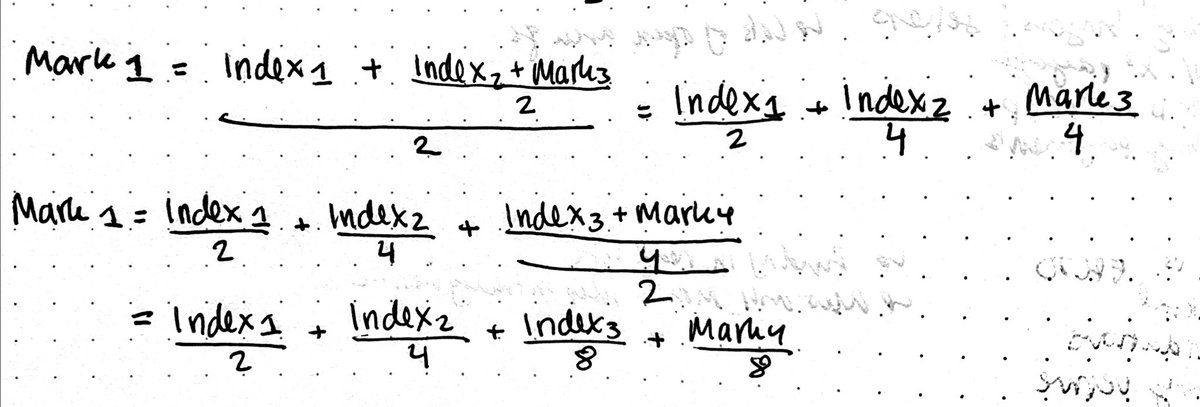

Then, taking this further substituting Mark₂, Mark₃ and so on, we see a pattern emerging (second photo)

Then, taking this further substituting Mark₂, Mark₃ and so on, we see a pattern emerging (second photo)

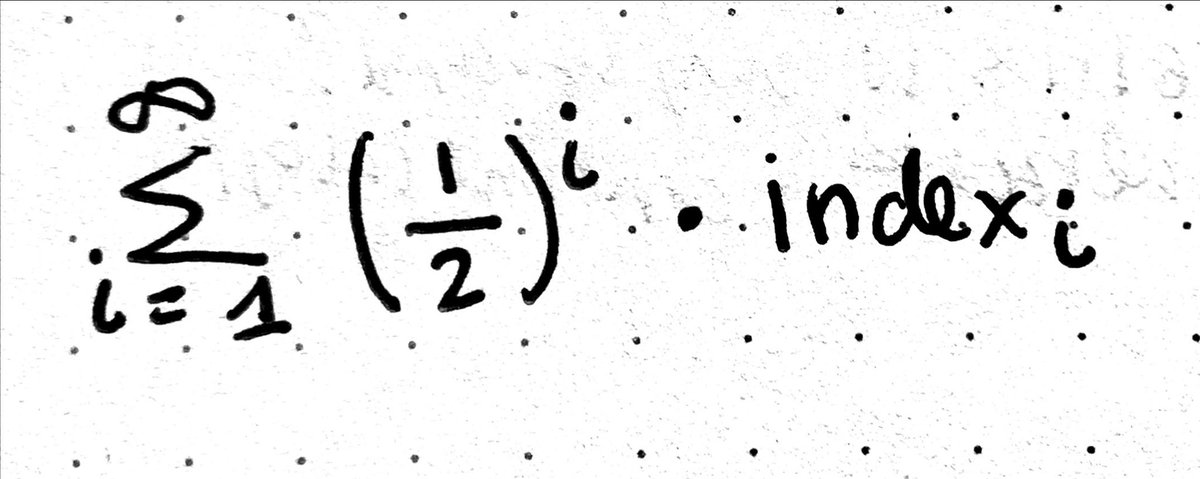

The result is the below summation

This summation gives us a formula for the funding of ANY perpetual instrument. Remember that perpetual swaps can be used for ANY asset as long as we have an oracle for the Index price, so this holds true for any arbitrary price feed 😎

This summation gives us a formula for the funding of ANY perpetual instrument. Remember that perpetual swaps can be used for ANY asset as long as we have an oracle for the Index price, so this holds true for any arbitrary price feed 😎

Now.. Let's get into options, but before we dive into everlasting options, let's review the payoffs for vanilla call and put options since we'll refer to them later.

A call option gives the holder the right, but not the obligation, to BUY the underlying asset at the strike price by a given expiry

So, if ETH is $2000 at expiry & the strike price of the call option is $3000, the option is out of the money, and the option expires worthless ($0)

So, if ETH is $2000 at expiry & the strike price of the call option is $3000, the option is out of the money, and the option expires worthless ($0)

Now if ETH is $4000 at expiry & the strike price of the call option is $3000, the option is in the money, and the option holder receives $1000, which is the difference between the ETH price and the strike price.

Now, let's call ETH price = E, strike price = K, & option price = C. We get the payoff of a call option:

C = max(E-K, 0)

If the call option expires ITM, (ETH price > strike price), E-K is positive

If the call option expires OTM, (ETH price < strike price), E-K is negative

C = max(E-K, 0)

If the call option expires ITM, (ETH price > strike price), E-K is positive

If the call option expires OTM, (ETH price < strike price), E-K is negative

The below diagram shows the call option payoff as well:

• Blue line is the payoff of an out of the money option, $0

• Green line is the payoff of an in the money option, E-K

• Red line is the payoff of the option as a whole, taking the max of the blue line and green line

• Blue line is the payoff of an out of the money option, $0

• Green line is the payoff of an in the money option, E-K

• Red line is the payoff of the option as a whole, taking the max of the blue line and green line

A put option gives its holder the right, but not obligation, to SELL the underlying asset at the strike price by a given expiry

So, if ETH is $2000 at expiry & the strike price of the put option is $1500, the option is out of the money, and the option expires worthless ($0)

So, if ETH is $2000 at expiry & the strike price of the put option is $1500, the option is out of the money, and the option expires worthless ($0)

Now if ETH is $1000 at expiry & the strike price of the put option is $2000, the option is in the money, and the option holder receives $1000, which is the difference between the ETH price and the strike price.

Now, let's call ETH price = E, strike price = K, and option price = P. We get the payoff of a put option:

P = max(K-E, 0)

If the put option expires ITM, (strike price > ETH price), K-E is positive

If the put option expires OTM, (strike price < ETH price), K-E is negative

P = max(K-E, 0)

If the put option expires ITM, (strike price > ETH price), K-E is positive

If the put option expires OTM, (strike price < ETH price), K-E is negative

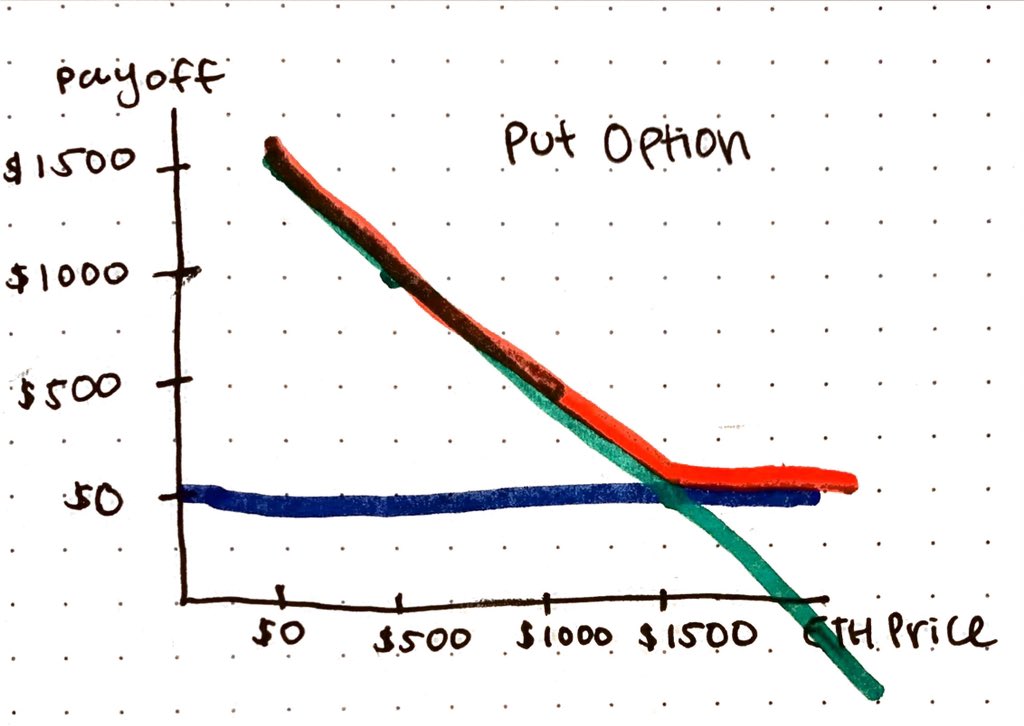

The below diagram shows the put option payoff as well:

• Blue line is the payoff of an out of the money option, $0

• Green line is the payoff of an in the money option, K-E

• Red line is the payoff of the option as a whole, taking the max of the blue line and green line

• Blue line is the payoff of an out of the money option, $0

• Green line is the payoff of an in the money option, K-E

• Red line is the payoff of the option as a whole, taking the max of the blue line and green line

Now, finally, Everlasting Options!

An everlasting option is an extension of a perpetual swap, where instead of tracking the price of ETH, we are tracking the price of an option. Compared to the vanilla options we looked at above, everlasting options NEVER expire.

An everlasting option is an extension of a perpetual swap, where instead of tracking the price of ETH, we are tracking the price of an option. Compared to the vanilla options we looked at above, everlasting options NEVER expire.

Just like a normal option, the person long the everlasting option must pay for that optionality. The option premium in this case is paid through funding.

For EOs, longs almost always pay shorts, since the longs have access to optionality with unlimited upside & limited downside.

For EOs, longs almost always pay shorts, since the longs have access to optionality with unlimited upside & limited downside.

Note that funding for everlasting options is still fundamentally governed by supply and demand, so if there are more shorts than longs, then longs could end up paying shorts.

To get the funding for an everlasting option, we revisit Mark - Index, but instead of Index being the price of ETH, instead it is the option payoff that we came up with earlier: max(E-K, 0) for a call and max(K-E, 0) for a put.

If we have daily funding, then max(E-K, 0) for a call and max(K-E, 0) for a put is the option payoff for the option expiring in one day's time. Up until expiry, we need to use the one-day options price to value Index, since Index is the payoff of the option expiring in one day.

So prior to expiry, we could use Black Scholes to get the value of Index. If the value of Index was not the option's price, there would be an arbitrage opportunity where one could buy the EO (if cheaper) and then sell the one day expiring option, or vice versa.

FINALLY, what is Squeeth?

Everlasting options remove expiries from an option, which is a desirable feature for DeFi users who prefer instruments they can hold perpetually without having to remember expiries. However, everlasting options do not remove option strike prices..

Everlasting options remove expiries from an option, which is a desirable feature for DeFi users who prefer instruments they can hold perpetually without having to remember expiries. However, everlasting options do not remove option strike prices..

Recall that with a perp swap, we can track ANY Index as long as we have a payoff for that Index. If we put x² as that index, then we get a payoff that on the long side resembles a call option, giving users pure convexity with unlimited upside and limited downside.

With squeeth, unlike traditional perps, funding is NOT designed to bring mark price back to index, but rather to "align" them & keep the difference at a reasonable premium. In this case, we expect squeeth to almost always trade above index bc it has positive gamma, like an option

In squeeth's case, Index is ETH², which is why it's called squeeth (squared ETH) 😎

Squeeth is a perpetual instrument that gives squeeth holders a payoff of ETH². For an overview of long squeeth, check out the below thread:

Squeeth is a perpetual instrument that gives squeeth holders a payoff of ETH². For an overview of long squeeth, check out the below thread:

https://twitter.com/wadepros/status/1444690047639461893?s=20

The real research heroes are @_Dave__White_ @danrobinson @snarkyzk @andrewjleone @AlexisGauba @aparnalocked @HS10010110 @antonttc @alpinechicken @llllvvuu for the concept, design, and development of squeeth 🧠🎨

Research references:

Everlasting Options research paper ↓

paradigm.xyz/2021/05/everla…

Power Perpetuals research paper ↓

paradigm.xyz/2021/08/power-…

Dave White's cartoon guide to perps ↓

research.paradigm.xyz/cartoon-guide-…

Dave White's convexity in options ↓

Everlasting Options research paper ↓

paradigm.xyz/2021/05/everla…

Power Perpetuals research paper ↓

paradigm.xyz/2021/08/power-…

Dave White's cartoon guide to perps ↓

research.paradigm.xyz/cartoon-guide-…

Dave White's convexity in options ↓

https://twitter.com/_Dave__White_/status/1423740205874302976?s=20

• • •

Missing some Tweet in this thread? You can try to

force a refresh