Couple charts I think are interesting. First is that LA ports are unloading small ships and wait is now around a month to unload from anchoring.

Scarcity effect will continue for some time given that backlog.

1/x

Scarcity effect will continue for some time given that backlog.

1/x

We have the Survey of Professional Forecasters next month and the revisions are likely to pick up at least 10bp for 22 & 23.

That will go into the FOMC SEP.

2/x

That will go into the FOMC SEP.

2/x

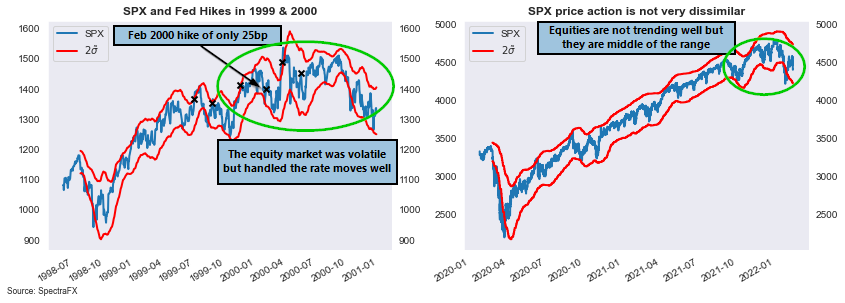

We're pricing a lot for the Fed but there is still scope for front to steepen.

3/x

3/x

Rates positioning by the market is short but not max short. So we can still get some movement.

4/x

4/x

And the pricing of liftoff for the ECB is still "tame". I expect pushback (given Lane's transitory comments) but the risk is for the market to tell Lagarde differently.

Though short EURUSD makes sense (as market would then price a more aggressive Fed imo).

5/5

Though short EURUSD makes sense (as market would then price a more aggressive Fed imo).

5/5

• • •

Missing some Tweet in this thread? You can try to

force a refresh