Naive view but I think Hunting #HTG may be on its way back to Covid lows because it's orphaned on the wrong market and there's an information disconnect - if so, my guess is that it's pretty oversold here.

The company isn't a pure play but it's good enough to say it's very shale exposed, towards the completion side vs the drilling side of things.

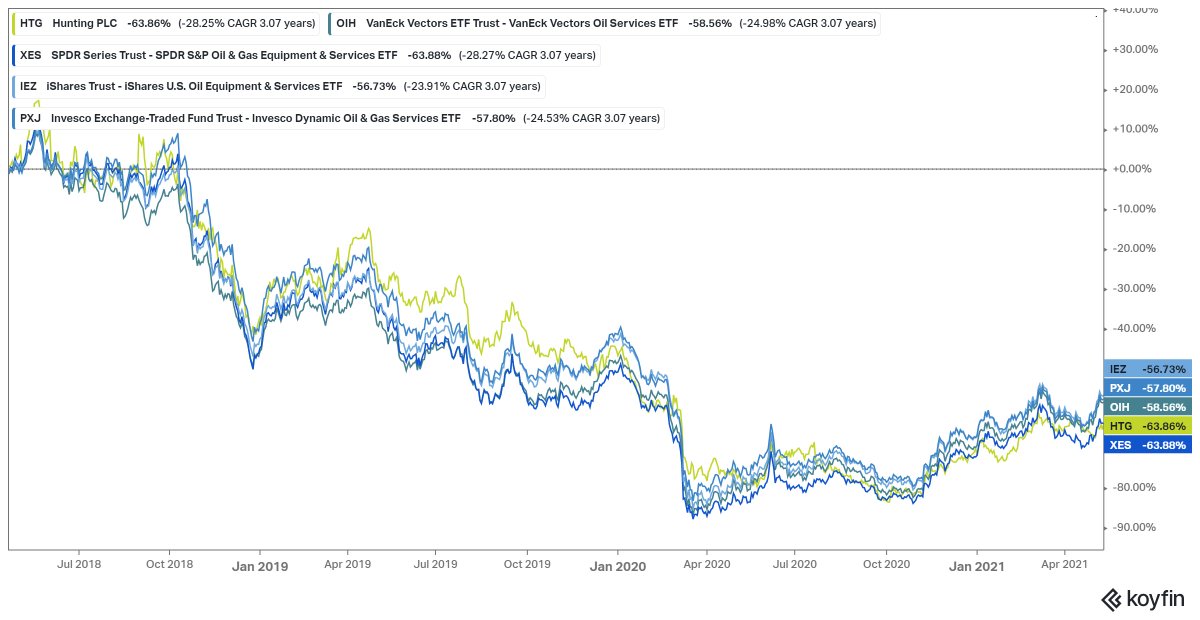

Three year chart to around May 2021: HTG in green vs several US oil services ETFs - as you can see, they trade in lockstep.

Three year chart to around May 2021: HTG in green vs several US oil services ETFs - as you can see, they trade in lockstep.

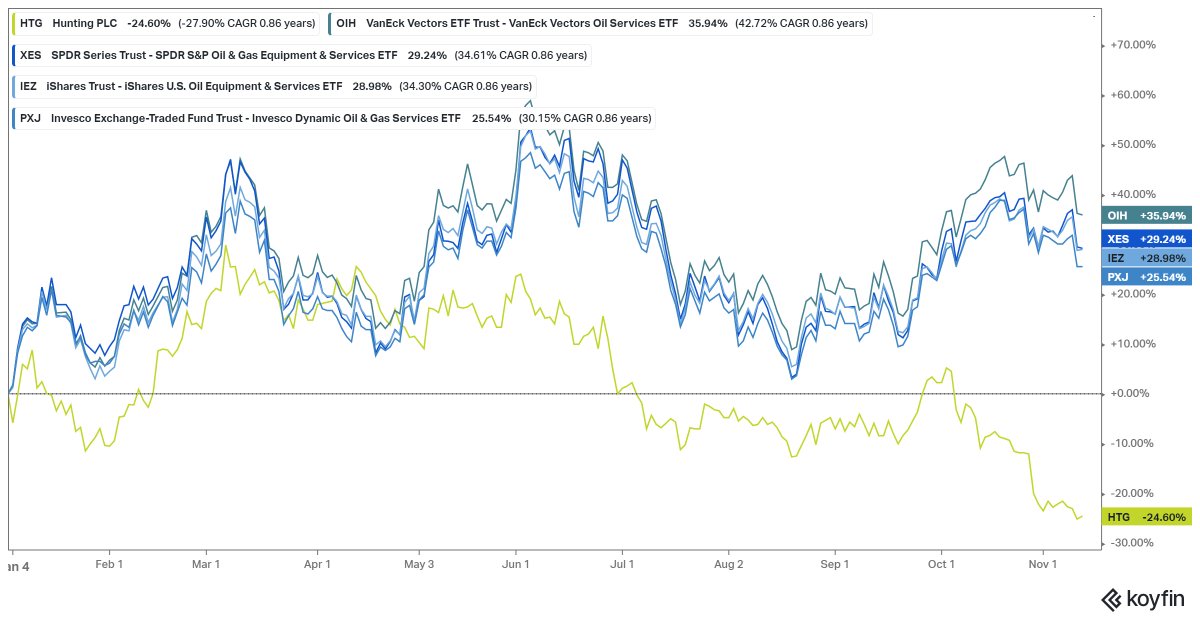

Same chart but on a 2021 YTD basis and it starts diverging somewhere around mid summer.

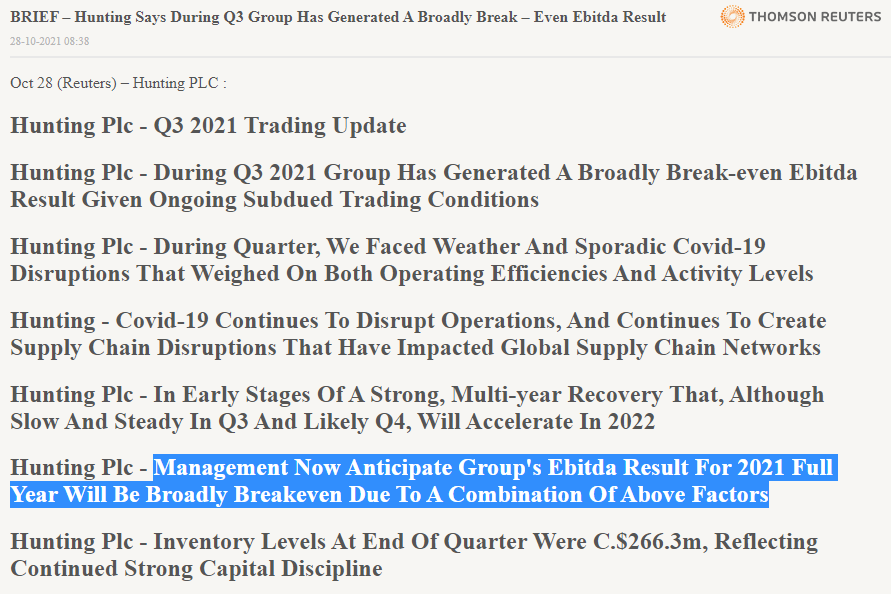

The quick and dirty is that the first half had the first signs of a little recovery but then guided to a 2021 EBITDA result "below previous expectations, but ahead of the 2020 full year result of $26.1m", then in Q3 lowered it from that to breakeven.

Disappointing sure but it's par for the course. Here's that 3 year to Summer chart in HTG vs $NOV - "no other vendor", services bellweather etc and again, it's lockstep.

Here's the last 3 halves of HTG's revenue vs $NOV's, the cadence is the same. Since it's orphaned in the UK without domestic comps, quarterly reporting or calls - we need to look to the US to find out what's going on

Here's what NOV say at Q3 - a similar H2 to HTG but look to 22

"While fourth-quarter results will be muted by ongoing supply chain challenges and cost inflation, recent orders growing global drilling activity, and improved pricing have us increasingly optimistic regarding 2022."

"While fourth-quarter results will be muted by ongoing supply chain challenges and cost inflation, recent orders growing global drilling activity, and improved pricing have us increasingly optimistic regarding 2022."

"Book-to-bills in excess of a 100% for the second quarter in a row for both the Completion and Production Solutions and RIG Technologies. I'm decidedly more positive about the outlook for the coming year... supply chain issues are making business challenging in the short run"

B2Bs up, quiet inflections happening.

"In our aftermarket business, we realized our third straight quarter of improved spare part bookings.. we expect this trend to continue into the fourth quarter"

"In our aftermarket business, we realized our third straight quarter of improved spare part bookings.. we expect this trend to continue into the fourth quarter"

DNOW - a distributor - same H2, same issues with logistics. Revenue cadence between this and HTG similar too.

You can break these segments out of dozens of companies and see the same trends and outlook everywhere. HTG is nothing special but I think the odds are more likely it's just operating in a UK information vacuum

What are the odds the UK market is somehow correctly identifying idiosyncratic problems with its single shale services company? Or that the UK is pricing in the shale capex outlook more accurately than the entire US market? I have my doubts.

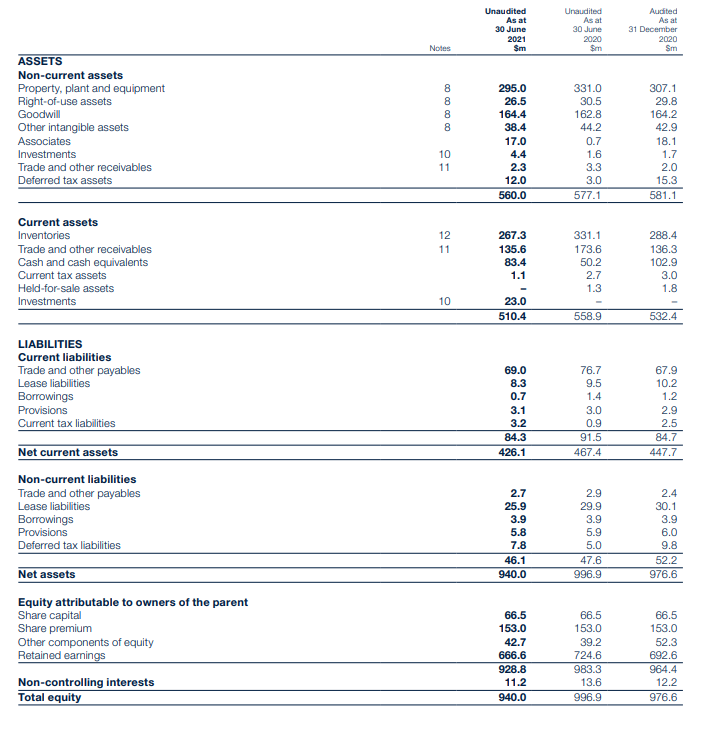

HTG balance sheet. Just a collection of cash and assets, not going bust before the uranium dawn arrives.

Red line trading here at historic price to book lows, first green line's a double, second's a triple. If the US oil sector turns out to be correct and HTG is just another middle of the pack services co, it should do fine.

In the context of commentary from US peers and sat at 52 week lows, this is about as bullish an update as you could wish for from #HTG

• • •

Missing some Tweet in this thread? You can try to

force a refresh