1. Think it is important to understand what just happened to the 2020 RVOs in yesterday's EPA rulemaking. Here is a link to the rulemaking (warning don't print it out unless you want to use a lot of paper) epa.gov/sites/default/…

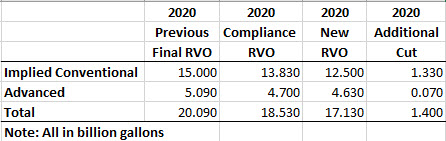

2. So let's review. The EPA issued a final rulemaking on the 2020 RVOs in late 2019 under the Trump Admin. We thought it was FINAL. The first column in the chart shows the RVOs in that FINAL rulemaking. Implied conventional (corn ethanol) was at the statutory level of 15BG.

3. Once the RVOs in gallons are finalized, then they are enforced in % terms on obligated parties (refiners). The base for the % RVOs is projected gasoline and diesel use in 2020 with some adjustments. That base number was 173.82BG in the FINAL rule.

4. The RVOs are enforced in % terms because this allows compliance to adjust or "float" as actual gasoline and diesel use differs in a year from what was projected when the FINAL rulemaking was made.

5. So when the COVID pandemic hit in March 2020 there was an automatic adjustment mechanism built into RFS compliance for 2020. The %s were fixed, not the volumes. The key is that COVID should not be a valid reason to change the FINAL rulemaking. It could adjust.

6. So, now we have the actual values for all the data needed to compute volumes for 2020 compliance. Published in the rulemaking released yesterday. The new base number is 160.37 compared to 173.82 in the FINAL rulemaking.

7. The second column in the table shows the RVO compliance volumes that would have been enforced if the FINAL rulemaking for 2020 had been left in place. The total RVO would have dropped 1.56BG automatically.

8. But, no the automatic downward adjustment in the 2020 RVOs was not good enough for the refiners. They pushed for new RVOs set way below what even the automatic adjustment would have been. The third column shows these new SECOND FINAL RVOs.

9. Bottom-line: the SECOND FINAL (just love the ridiculous sound of that) RVO for 2020 released yesterday is a cut of 1.4BG over and above what would have simply happened automatically. That is not chump change and should not be glossed over. Big win for refiners.

• • •

Missing some Tweet in this thread? You can try to

force a refresh