I spent 2 months doing a deep dive into DEXs, Governance Tokens, Staking, and Liquidity Pools. What I found was not expected. Rather than being considered low risk, DEX investments can have lots of risk, but if executed properly offer investors massive alpha. Let's dive in:

Something that is still missing from the Web3 discourse is a new fundamental understanding of intrinsic value as it pertains to decentralized assets. Traditional financial investment philosophy has offered standardized models of intrinsic value calculations across numerous styles

However, since dAssets have emerged recently, they represent entirely new paradigms for investment assets. dAsset classes are still not well understood, and the proper methodologies to find intrinsic values are still debated. This thread looks at DEXs through this lens:

Ownership in DEXs is represented by governance tokens, which represent a couple of things:

1. Voting (Governance) Power

2. An unleveraged long interest in the price performance of the governance token

3. In specific cases, the ability to earn yield on the tokens through staking

1. Voting (Governance) Power

2. An unleveraged long interest in the price performance of the governance token

3. In specific cases, the ability to earn yield on the tokens through staking

There are 3 types of governance tokens:

1. GO: Governance Only (no economic interest; only voting power in governance)

2. GY: Governance + Yield (both gov. voting power & opportunity to earn yield)

3. GO→GY: Governance Only → Yield (GO tokens that can convert into GY tokens)

1. GO: Governance Only (no economic interest; only voting power in governance)

2. GY: Governance + Yield (both gov. voting power & opportunity to earn yield)

3. GO→GY: Governance Only → Yield (GO tokens that can convert into GY tokens)

Understanding the intrinsic value of tokens offered by DEXs, it is necessary to understand both the value of the governance power of the token and the value of the future yield of the token. Let’s take them one at a time - first focusing on the value assigned to governance power:

The value of a GO token is proportional to the influence that token has on the direction of the DEX. When the voting power of a protocol is centralized, governance tokens hold less value; conversely, when token ownership is decentralized, governance tokens become more valuable.

But there is a nuance here. When protocols are launched they ought to be more centralized, and as they mature they should be more decentralized. As you can see in the graphic above, having sophisticated investors with concentrated ownership can be assigned higher intrinsic values

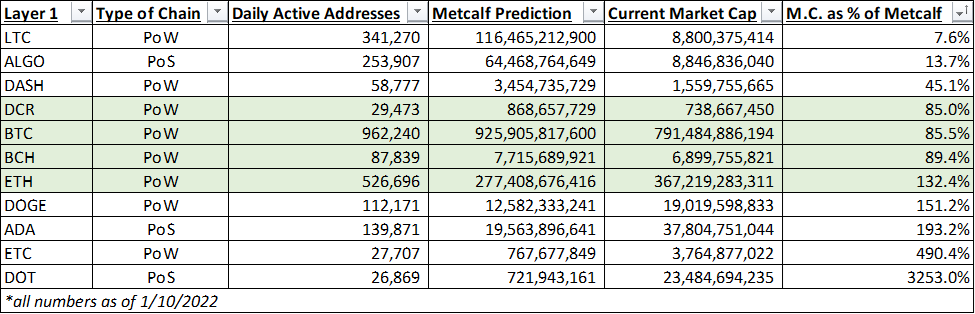

Here is an example of how one might look at the ownership structures of different DEXs (merely examples - please let me know if any of this data should be updated:

Another consideration re: the intrinsic value of GO tokens: if the DEX has rules that limit the participation of smaller token holders the DAO should be considered as highly centralized, even if the tokens have a high level of distribution.

Uniswap is a perfect example of a ‘decentralized’ DEX that currently operates as an oligopoly - effectively 63 addresses control the entire protocol AND the tokens are currently GO, so smaller holders can’t even earn yield in exchange for holding $UNI bags.

To wrap up the idea, a framework for the sophisticated investor looking at GO, GO→GY, and GY tokens might look something like this:

Next, let’s look at tokenomics. The important themes to understand about the tokenomics of a DEX prior to investing include (de)centralization, governance policies and inflation. First, let’s talk about decentralization over time using two separate examples - BAL and CRV:

Remember, the most ideal tokenomics structures are those that start centralized and are decentralized in their end-state. The CRV tokenomics model achieves the desired end-state, but seems to be too decentralized from the outset.

On the other hand, Balancer $BAL shows a perfect example of how governance can eventually be turned over to the community - exactly 3 years from launch, the governance of the DEX shifts from the core team and investors to the community:

The holder of governance tokens - whether GO or GY - should fully understand the tokenomics models of the tokens that they are buying prior to making a purchase. Now, let’s move into the next level of complexity: staking for yield with GY tokens.

By staking the investor is telling the protocol that they are a long-term HODLer and that they would like to receive part of the income generated by the DEX. The income is usually derived as a percentage of the total volume exchanged on the DEX in any given period.

An example calc of staking yield (from SushiAnalytics):

Total xSUSHI= 58.6mm = $628.7M TVL

Investor stakes 10,000 xSUSHI = $107,300 (0.017% of pool)

Staking Reward = 0.05% of all volume

DEX Volume = $174.2B

Investor Reward = $174.2B*0.05% * 0.017% = $14,807

Investor APY = 13.8%

Total xSUSHI= 58.6mm = $628.7M TVL

Investor stakes 10,000 xSUSHI = $107,300 (0.017% of pool)

Staking Reward = 0.05% of all volume

DEX Volume = $174.2B

Investor Reward = $174.2B*0.05% * 0.017% = $14,807

Investor APY = 13.8%

The best way to think about yield is as a dividend paid on the GY token. The analysis conducted prior to staking must incorporate the risk of the DEX's failure during the life of the investment. If the DEX fails or the token price goes to $0, any principal and yield will be lost.

Fortunately, we can use traditional finance as a parallel to understand how to value yields of GY tokens. Typically a simple DCF will do, unless the tokenomics are exceedingly complicated:

In the model above, the NPV of the yields are lower than the current token price. This may happen for a number of reasons:

1. Holders foresee increased yields in the future

2. Holders assign $1.95 of value to the governance of the DAO.

1. Holders foresee increased yields in the future

2. Holders assign $1.95 of value to the governance of the DAO.

3. Holders believe the market is overestimating the riskiness of the protocol (discount rate is too high)

4. Holders foresee reward %s increasing in the future

5. A combination of two or more of the above

4. Holders foresee reward %s increasing in the future

5. A combination of two or more of the above

In the valuation of any GY token, a portion of the intrinsic value should be allocated to the value of governance, and a portion should be assigned to the NPV of the token’s yield. The investor will determine which assumptions they value more or less highly.

Now, let’s dive into the final (and most complex topic) - farming liquidity pools:

***Before ever providing liquidity into a pool, the investor should understand the following terms: AMM, liquidity pool, and impermanent loss (also called divergence loss). If you don’t, you will likely lose money by choosing the wrong farms.***

Understanding the risks of LP farming is more important than examples of successful farming operations, so we will talk about liquidity pool size, impermanent loss (IL), and token devaluation first, and then to wrap up an example of a successful farm will be given.

The first risk isn’t a risk as there is no risk of capital loss due to the changing size of a liquidity pool, assuming that prices and correlation between the two tokens in a pool remain constant. If either price or corelation change, an investor will face IL & devaluation risks.

Impermanent loss is very complicated and there are lots of good resources explaining it - check out this thread by @jonwu_ :

I will try not to be repetitive, so let’s instead talk about the main drivers of impermanent loss and how to deal with them.

https://twitter.com/jonwu_/status/1389782646000078850.

I will try not to be repetitive, so let’s instead talk about the main drivers of impermanent loss and how to deal with them.

IL Risk is increased exponentially by decreasing price correlation between assets in a pool. Read that again. This graph proves the point. If token price correlation is <30%, or assets are inversely correlated, you will lose principal farming, regardless of how high the yield is.

Therefore, a proposed rule: if an investor is considering providing liquidity and farming a pool, they should only do so if the price correlation between assets is >30%, or 40% if they want a margin of safety.

Devaluation risk occurs when one token in a pool suddenly loses its value. This will cause permanent loss of an investor's capital. Deep DD to understand that both tokens are fundamentally sound should always be completed. @jonwu_ 's thread explains the math of devaluation risk.

Even if you don't follow the math, understand that the risk of one of the currencies in a liquidity pool dropping substantially can be more harmful to an investor's capital than if they had not farmed at all.

Finally, let’s look at what a successful farming investment looks like, using the $ETH<> $ENS pool on #Sushiswap from November 9 through December 10, 2021 as an example:

An investor stakes:

1.25 ETH = $6,186 @ $4,814.01

140 ENS = $6,522 @ $46.59

Total Invested Capital: $12,709

The investor then decides to de-stake on 12/10. During that time:

ETH decreased to $4,045.53, or -16.0%

ENS decreased to $44.16, or -5.2%

Impermanent Loss = -0.2%

1.25 ETH = $6,186 @ $4,814.01

140 ENS = $6,522 @ $46.59

Total Invested Capital: $12,709

The investor then decides to de-stake on 12/10. During that time:

ETH decreased to $4,045.53, or -16.0%

ENS decreased to $44.16, or -5.2%

Impermanent Loss = -0.2%

Sushiswap offers 0.25% to LPs, so we expect to see positive yield from this liquidity pool investment. The investor’s wallet shows:

1.577 ETH = $6,379.80

144.3 ENS tokens = $6,372.29

Total Divested Value = $12,752.09, a gain of 0.34%

1.577 ETH = $6,379.80

144.3 ENS tokens = $6,372.29

Total Divested Value = $12,752.09, a gain of 0.34%

Initially we can see that the investment was successful - the investor has more money than they started with - but in order to determine relative profitability, we have to analyze the total gain from the pool relative to the value of the tokens had they chosen only to hold them:

Had we just bought and held the individual tokens:

ETH Value: $4,045.53 * 1.258 = $5,199.19

ENS Value: $44.16 * 140.0 = $6,182.40

Current Value if Assets Only Held, Not Invested = $11,381.59, a loss of 10.45%

Now it becomes more obvious why this investment was so successful:

ETH Value: $4,045.53 * 1.258 = $5,199.19

ENS Value: $44.16 * 140.0 = $6,182.40

Current Value if Assets Only Held, Not Invested = $11,381.59, a loss of 10.45%

Now it becomes more obvious why this investment was so successful:

Divested Value: $12,752.09

Held Assets Value: $11,381.59

Rewards Gained From Providing Liquidity: $1,370.50, or a 10.8% relative return vs. not investing

Even including the 0.18% impermanent loss, the investor in this trade came out very far ahead.

Held Assets Value: $11,381.59

Rewards Gained From Providing Liquidity: $1,370.50, or a 10.8% relative return vs. not investing

Even including the 0.18% impermanent loss, the investor in this trade came out very far ahead.

Now it’s clear why staking to the $ETH<> $ENS pool was a successful endeavor. While the token pair sold off 10.5%, by providing liquidity and earning yield, the investor has instead fully hedged their downside and has instead realized a gain of 0.34%.

Hopefully this thread will help those trying to understand DEXs, how to invest in their governance tokens, and will lead to further discussion of the intrinsic value of these tokens.

• • •

Missing some Tweet in this thread? You can try to

force a refresh