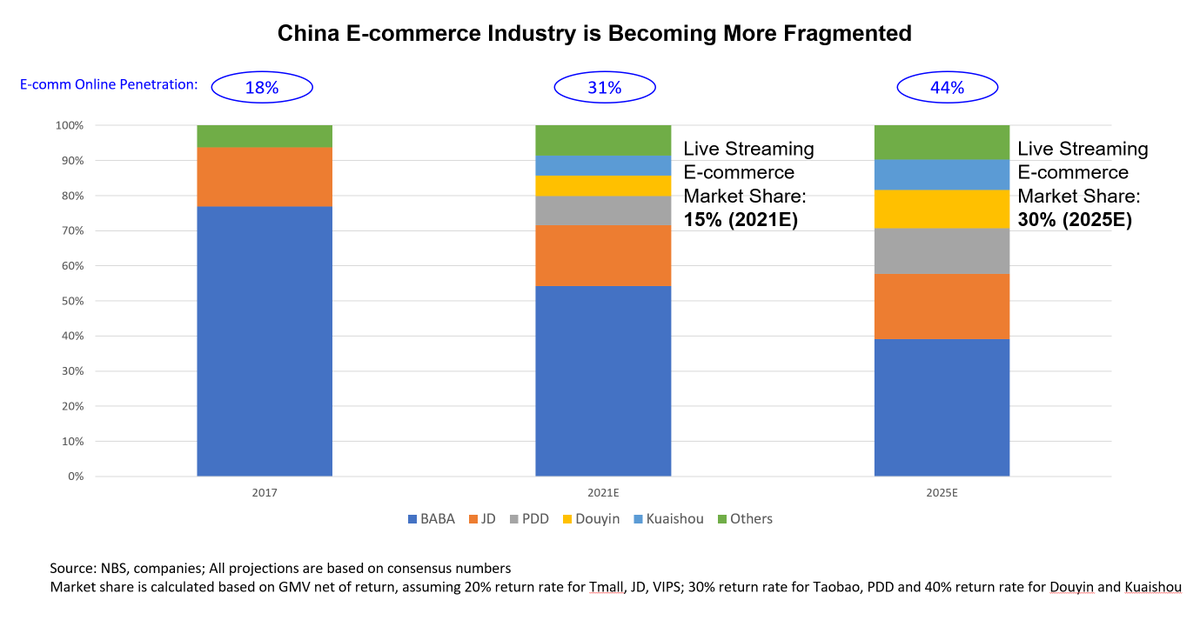

1/ China’s e-commerce, with the highest online penetration (30%+), serves as a playbook of how the industry might evolve:

Search-based -> Social E-comm (2018) -> On-demand (2020) -> Live Streaming (2021+)

The industry, though very mature, has become MORE fragmented over time

Search-based -> Social E-comm (2018) -> On-demand (2020) -> Live Streaming (2021+)

The industry, though very mature, has become MORE fragmented over time

2/ Where’s the rest of the world following China’s playbook:

- US: early days for Live Streaming E-commerce (all big platforms plus start-ups)

- SEA and LatAm: social e-commerce (Shopee)

Globally, the line between online media and e-commerce platforms is blurring...

- US: early days for Live Streaming E-commerce (all big platforms plus start-ups)

- SEA and LatAm: social e-commerce (Shopee)

Globally, the line between online media and e-commerce platforms is blurring...

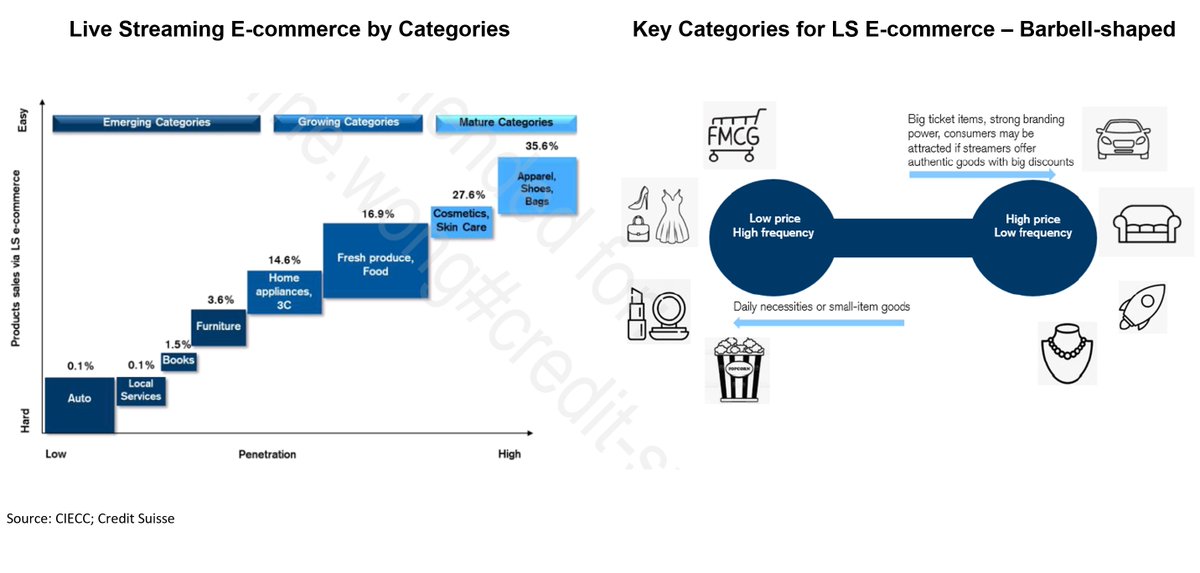

3/ Key stats of China's Live Streaming E-commerce:

- 400mm users (50% of total e-commerce users)

- Already a $200bn market (15% of total e-comm), expect to take 30% market share by 2025E

- Growing 3x faster vs. industry

- Top platforms: Taobao Live + Douyin + Kuaishou

- 400mm users (50% of total e-commerce users)

- Already a $200bn market (15% of total e-comm), expect to take 30% market share by 2025E

- Growing 3x faster vs. industry

- Top platforms: Taobao Live + Douyin + Kuaishou

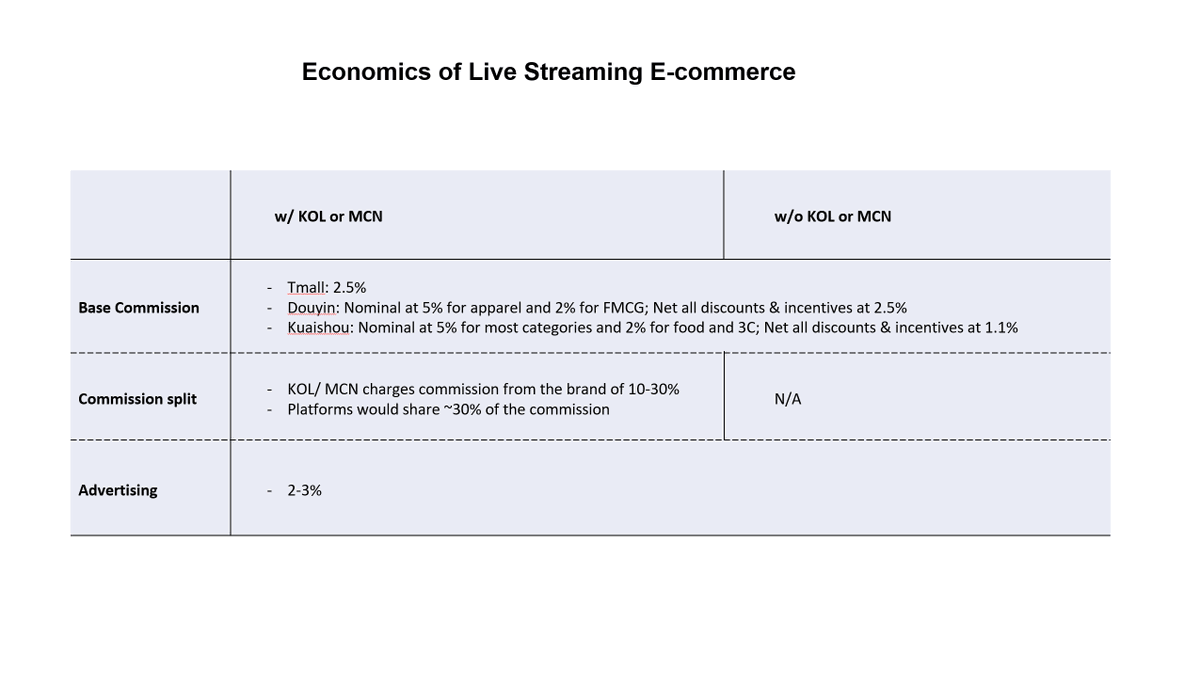

4/ Unit Economics of Live Streaming E-commerce:

- KOLs and celebrities take 20%+

- Increasingly we are seeing GMVs generated by brands themselves

- KOLs and celebrities take 20%+

- Increasingly we are seeing GMVs generated by brands themselves

• • •

Missing some Tweet in this thread? You can try to

force a refresh