Liquidity vs volume 101 - in my flow 101 I talked about forced selling/inelastic flow. Selling at any price. That inelastic flow tends to have a large impact on price. I want to talk about volume in this context. My view of normal conditions in markets is that supply and demand

Are both highly elastic for around last sale. This creates the conditions necessary for tons of volume. However I think when a large inelastic player enters the market it overwhelms the local elasticity and pushes into a portion of the elasticity curve that is much less elastic.

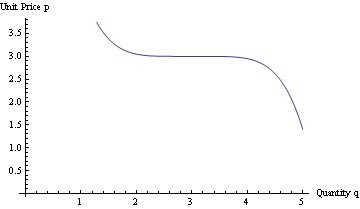

Of course at some price change extremely high elasticity returns. So conceptually something like this

I've seen practical examples of this effect when pricing large bought deals of secondary stock offerings. Huge local volume stock has a large dead zone of demand as price moves without true long term investors seeing the move. They then step in.

Think about liquidity providers when working through this concept. Tons of capital at the last sale. But when that sizable capital is chewed through the next tier wakes up. But slowly. And the next tier after that. Finally the long term holder.

It's possible that the curve has more steep sections and more flat sections along the way. And I could be totally wrong and there are infinite steep and flat making the curve classically concave. But I think it is S shaped.

Also I want to differentiate between liquidity related changes in price and changes in the equilibrium price based on changes in information. Obviously all of this is going on at the same time. Furthermore these elasticity curves are not stable through time.

However if you are with me on the S shape nature you can see how an asset with tremendous volume generated by steep local elasticity may actually be fairly illiquid when faced with an inelastic seller.

Volume is one measure. It can be very high if local elasticity and temporary liquidity provided by market makers is high. Elasticity can be extremely flat or even negative once that demand is chewed through. Eventually long term holders steepen the elasticity again. Estimating

This elasticity curve is table stakes for every large asset manager who may in the future need to move a large block of an asset. They do it by measuring every large trade they do. If they are big enough they have a ton of info on the shape. Tables stakes and well understood

Btw ignore the axis. It's the shape that matters

Thanks for the RT

• • •

Missing some Tweet in this thread? You can try to

force a refresh