Sales of new single‐family houses in Nov 2021 were at a seasonally adjusted annual rate of 744,000, this is 12.4% above the revised (down) Oct. rate of 662,000. The median sales price of new houses sold in Nov. was $416,900, 18.8% higher than one year ago and a new record high.

By stage of construction, the share of completed homes sold was 22%, down from 25% one year ago. Prior to the pandemic, completed homes made up the largest share of new homes sold. Today, it is homes under construction.

By stage of construction, the share of completed homes/ready to occupy inventory in November was 9.7%, down from 14.5% one year ago. While the share of new home inventory that is not started increased from 22% to 27%.

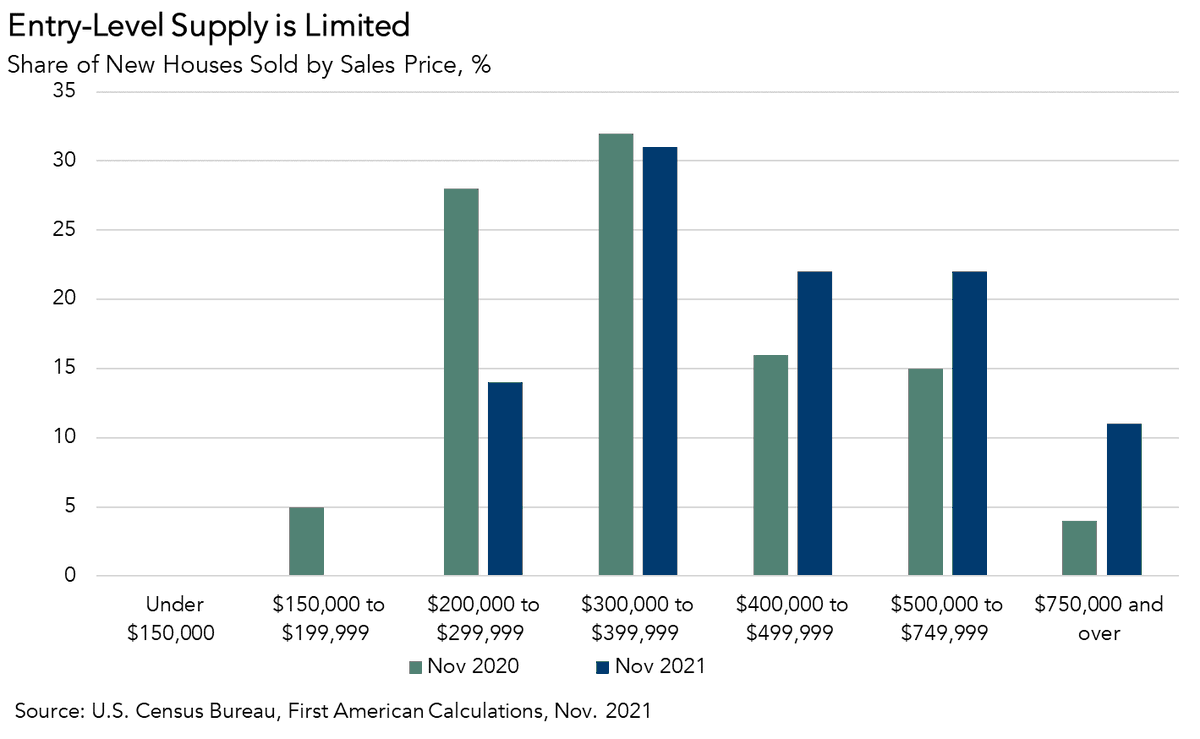

Record level new home prices may be pricing out some buyers. In Nov 2020, 33% of new home sales were priced below $300,000. In Nov 2021, only 14% of new home sales were priced <$300,000. Demand for new homes remains strong, but construction costs & prices have increased.

Borrowing costs remain low, demographic demand high and existing-home inventory remains near record lows, making a new home an attractive option. Yet higher construction costs (labor, lumber, materials) are being passed on to the consumer, resulting in higher new home prices.

• • •

Missing some Tweet in this thread? You can try to

force a refresh