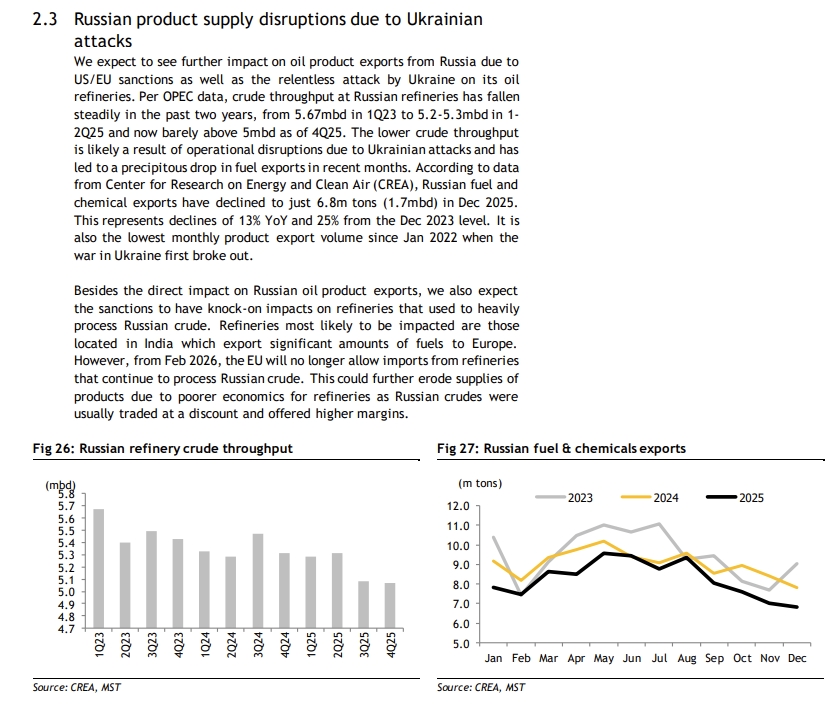

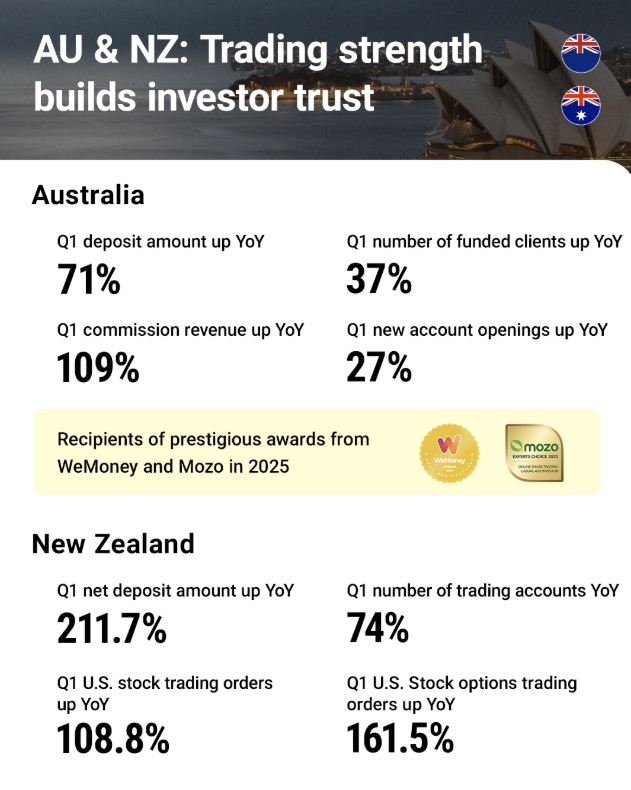

(1/12) Briq Properties

Börsvärde: €75m

Hyresintäkter per år: €7,7m

Vakans: 1%

WAULT: 8,75 år

GAV: €114m (NAV €84,5m)

LTV: (net) 20%

47% Logistik

30% Kontor

17% Hotell

Greklands första ESG-klassade fastighetsbolag

En mindre pitch (& komplettering till Premia)

Börsvärde: €75m

Hyresintäkter per år: €7,7m

Vakans: 1%

WAULT: 8,75 år

GAV: €114m (NAV €84,5m)

LTV: (net) 20%

47% Logistik

30% Kontor

17% Hotell

Greklands första ESG-klassade fastighetsbolag

En mindre pitch (& komplettering till Premia)

(2/) Briq är sprunget ur ett av Europas bäst avkastande investmentbolag (högre än Latour & Investor): Quest Holdings.

Sfären äger äger ca. 50% av Briq Properties och jag förväntar mig samma goda corporate governance (och aktieägarvärde) här.

Sfären äger äger ca. 50% av Briq Properties och jag förväntar mig samma goda corporate governance (och aktieägarvärde) här.

(3/)

Aspropyrgos:

102 800m2 mark där Fas 1 (20,800m2) nybyggd logistikfastighet tillträds i feb/mar (inräknat i hyresvärdet ovan)

Fas 1

25 Lastramper

29 250 Pallar i utrymme

12,5m högt

Solpaneler på taket

Gross Yield > 8%

Greklands största IT-distributör som hyresgäst

Aspropyrgos:

102 800m2 mark där Fas 1 (20,800m2) nybyggd logistikfastighet tillträds i feb/mar (inräknat i hyresvärdet ovan)

Fas 1

25 Lastramper

29 250 Pallar i utrymme

12,5m högt

Solpaneler på taket

Gross Yield > 8%

Greklands största IT-distributör som hyresgäst

(4/) Sarmed

131 200m2

8 byggnader a 58 600m2

*På* Europaväg

Gross Yield > 7,5%

Vakans: Nej

131 200m2

8 byggnader a 58 600m2

*På* Europaväg

Gross Yield > 7,5%

Vakans: Nej

(5/) 17% av portföljen är Hotell och samtliga drivs av 3e part (tänk Platzer).

Deras Hotell i huvudstaden omnämndes i veckan av "Michelin 2021 Boutique & Luxury Guide". Ett f.d. ambassadhus omgjort till hotell.

Deras Hotell i huvudstaden omnämndes i veckan av "Michelin 2021 Boutique & Luxury Guide". Ett f.d. ambassadhus omgjort till hotell.

(6/) Ett par notes från call med mgmt.

Grekland saknar nästan helt AAA-logistikfastigheter och man ser en möjlighet för greenfield (och ändå få) ~8% gross yield.

T.ex. Aspropyrgos ovan (100k m2 som bara förädlats med 20k byggnad hittills).

Grekland saknar nästan helt AAA-logistikfastigheter och man ser en möjlighet för greenfield (och ändå få) ~8% gross yield.

T.ex. Aspropyrgos ovan (100k m2 som bara förädlats med 20k byggnad hittills).

(7/)

Sista lånet man omförhandlade landade på 2,25% och trenden har varit rakt nedåt.

2020

NP3 2,73%

Nyfosa 1,9%

Sagax 1,8%

Kungsleden 1,8%

Sista lånet man omförhandlade landade på 2,25% och trenden har varit rakt nedåt.

2020

NP3 2,73%

Nyfosa 1,9%

Sagax 1,8%

Kungsleden 1,8%

(8/)

Så, Briq med €7,7m i årliga hyresintäkter (fr.o.m. mars) och net LTV 20% har €75m i börsvärde. Enligt Selin & Mr. Vestum/Stenhus finns det objekt att köpa med yields vi inte har sett i Sverige sen 2008-2009.

Starka kontraster ↘️

Så, Briq med €7,7m i årliga hyresintäkter (fr.o.m. mars) och net LTV 20% har €75m i börsvärde. Enligt Selin & Mr. Vestum/Stenhus finns det objekt att köpa med yields vi inte har sett i Sverige sen 2008-2009.

Starka kontraster ↘️

(9/)

€4,25/sqm i deras senast skrivna hyreskontrakt (tidigare €3,6-€3,9).

Förra veckan såldes en handelsfastighet till 9% över bokfört värdet (2021-06-30, extern värderingsaktör) och 32% över anskaffningsvärdet.

✅Hyreshöjningar

✅Värdeuppgång

Ingredienserna för...

€4,25/sqm i deras senast skrivna hyreskontrakt (tidigare €3,6-€3,9).

Förra veckan såldes en handelsfastighet till 9% över bokfört värdet (2021-06-30, extern värderingsaktör) och 32% över anskaffningsvärdet.

✅Hyreshöjningar

✅Värdeuppgång

Ingredienserna för...

(10/)

Jag håller med Philip Hallberg helt och hållet: inom fastighetsbranschen är alldeles för mycket fokus på substansvärden och alldeles för lite på kassaflödestillväxt.

Missa inte detta avsnittet: efn.se/poster/efn-mar…

Jag håller med Philip Hallberg helt och hållet: inom fastighetsbranschen är alldeles för mycket fokus på substansvärden och alldeles för lite på kassaflödestillväxt.

Missa inte detta avsnittet: efn.se/poster/efn-mar…

(11/) Beräknar kunna nå €150m GAV via 40% gearing och ingen aktieutspädning ö.h.t.

(Utan hyres- & värdeökningar).

2022-2023 (?)

~€10,5-11,5m hyresintäkter

~ €1,4-1,8m räntekostnad

€75m mcap 👀

yield compression på det? 👀

(Utan hyres- & värdeökningar).

2022-2023 (?)

~€10,5-11,5m hyresintäkter

~ €1,4-1,8m räntekostnad

€75m mcap 👀

yield compression på det? 👀

(12/12) Även "the top 1 percent"-gänget måste nog medge att i SBBs årsredovisning 2018, så var det svårt att "bevisa" +550% i avkastning kommande 3 åren. Eller Nyfosas +300%.

Jag kan inte "bevisa" att denna går hem, men jag ser extremt fin R/R.

Premia + Briq = 10% av Depån

Jag kan inte "bevisa" att denna går hem, men jag ser extremt fin R/R.

Premia + Briq = 10% av Depån

• • •

Missing some Tweet in this thread? You can try to

force a refresh