Some takeaways from Morgan Stanley's Q4 CIO survey

- Software has the highest growth expectations in IT

- Strong demand in software persisting (not simply pull forward in 2021)

- Cloud computing remains CIO's top priorities

- Security software most defensible

More graphs below

- Software has the highest growth expectations in IT

- Strong demand in software persisting (not simply pull forward in 2021)

- Cloud computing remains CIO's top priorities

- Security software most defensible

More graphs below

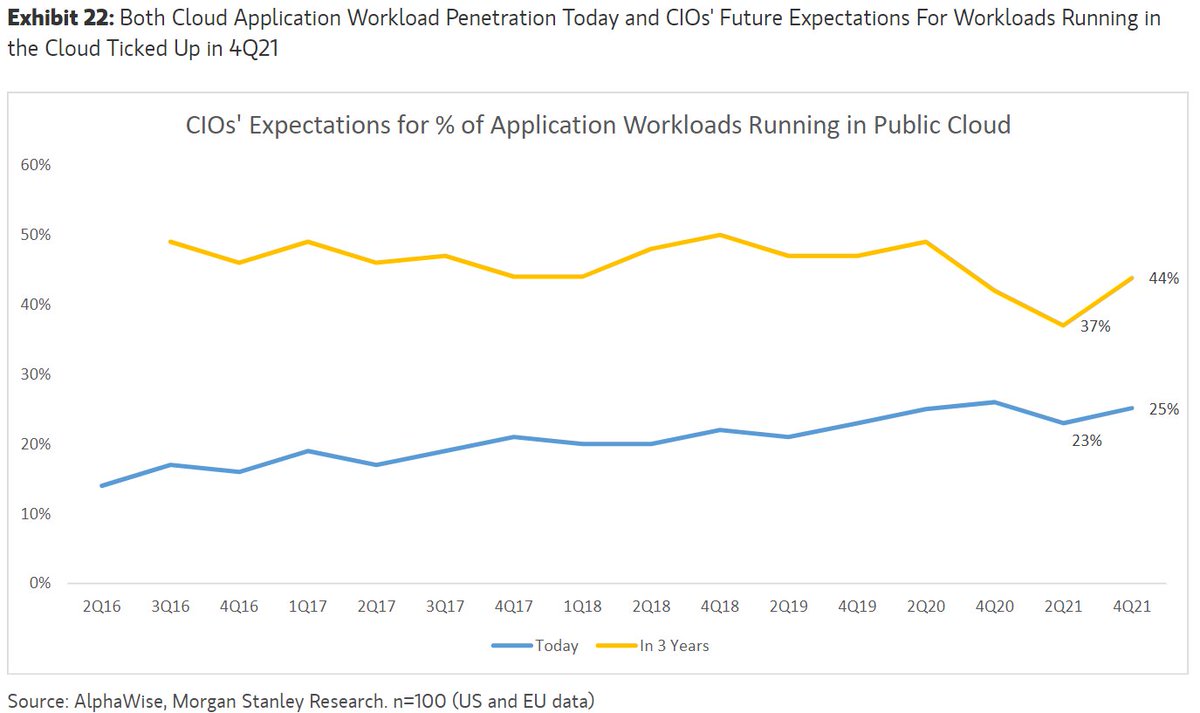

"Survey data suggests 25% of application workloads are running in the public cloud today, up from 23%... in 2Q21. The multi-year trend in the migration of applications to the cloud remains intact, with CIOs expecting 44% of workloads to reside in public cloud by 2024"

Similar data but presented differently. We're in the early innings of the cloud

Cloud computing, security software, and digital transformation are the top 3 priorities

Security software remains the most defensible category

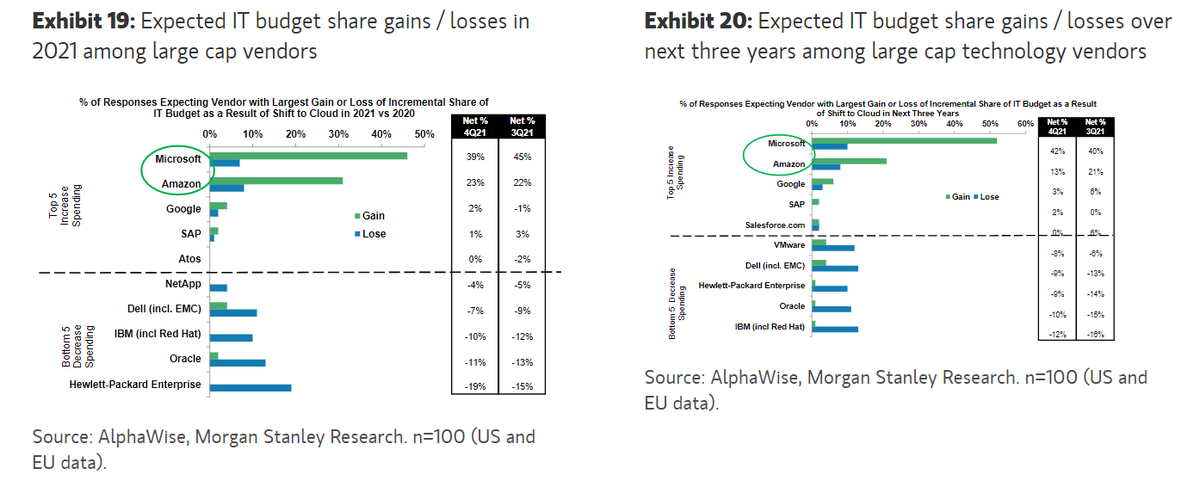

"As workloads continue to shift from on-premise to the cloud, Microsoft and Amazon remain the largest beneficiaries , both in 2021, as well as over the next three years"

"Snowflake screens as the vendor with the highest weighted average growth expectations in 2022 at +7.1%...30% of CIOs surveyed expecting spend to increase in 2022, vs. 0% of CIOs expecting spend to decrease."

Microsoft has the highest up-to-down ratio of 70%

Microsoft has the highest up-to-down ratio of 70%

Maybe most importantly:

"Expectations for software spending growth in 2022 remain ahead of historical levels, refuting the notion of a pull forward in demand in CY21"

"Expectations for software spending growth in 2022 remain ahead of historical levels, refuting the notion of a pull forward in demand in CY21"

• • •

Missing some Tweet in this thread? You can try to

force a refresh