Potential Multibagger stocks on the basis of techno funda divided in 3 categories

a. Share Price, Sales & Profit at all time high

b. Sales & Profit ath but not Price

c. Dark horses

Sectors covered

Automobiles

Banks

Bearings

Cables

Capital goods (electric & non electric)

🧵👇

a. Share Price, Sales & Profit at all time high

b. Sales & Profit ath but not Price

c. Dark horses

Sectors covered

Automobiles

Banks

Bearings

Cables

Capital goods (electric & non electric)

🧵👇

Automobiles

Tata motors (invested)

Tata motors (invested)

Banks

Companies in our watchlist

SBIN

Axis Bank

Canara bank (invested)

Indian Bank

Federal Bank

Union Bank

Indian Overseas Bank

Companies in our watchlist

SBIN

Axis Bank

Canara bank (invested)

Indian Bank

Federal Bank

Union Bank

Indian Overseas Bank

Bearings Sectors

Schaffler india (invested)

Schaffler india (invested)

Cables Sectors

Our Watchlist companies

Dynamic Cables

Polycab

FInolex cables

Our Watchlist companies

Dynamic Cables

Polycab

FInolex cables

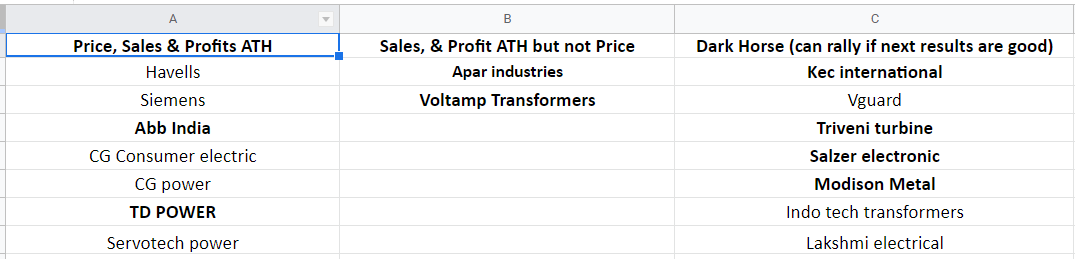

Capital Goods: Electric

Our Watchlist companies

ABB india

TD Power (recently invested)

Voltamp Transformers (invested)

Apar industries

Kec international

Triveni turbine (invested)

Salzer electric

Modison Metal

Our Watchlist companies

ABB india

TD Power (recently invested)

Voltamp Transformers (invested)

Apar industries

Kec international

Triveni turbine (invested)

Salzer electric

Modison Metal

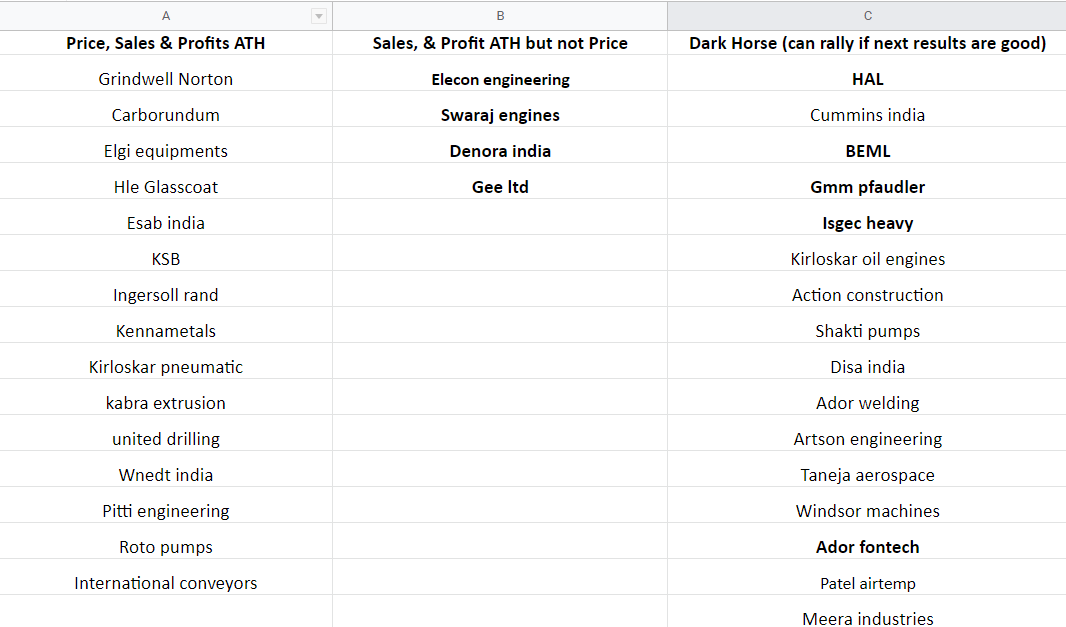

Capital Good: Non Electric

Our Watchlist companies

Elecon engineering

Swaraj engines

Denora India

Gee ltd

HAL

BEML

Gmm Pfaudler

Isgec heavy

Ador Fontech

Our Watchlist companies

Elecon engineering

Swaraj engines

Denora India

Gee ltd

HAL

BEML

Gmm Pfaudler

Isgec heavy

Ador Fontech

• • •

Missing some Tweet in this thread? You can try to

force a refresh