Lots of people liking the squeeth. Also lots of questions about the squeeth.

Below are some of the topics and details that made the squeeth "click" for me. It's a non-exhaustive list, but I hope it's helpful for you too!

Below are some of the topics and details that made the squeeth "click" for me. It's a non-exhaustive list, but I hope it's helpful for you too!

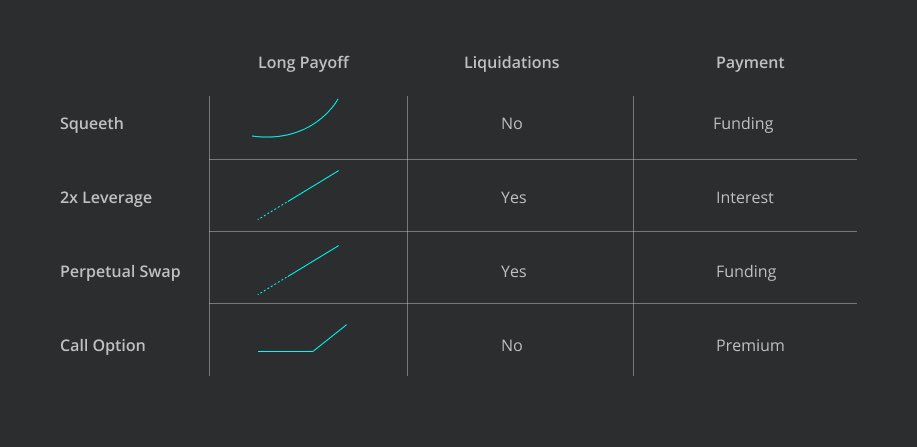

Mechanism-wise, Squeeth functions similar to a perpetual swap, tracking the index of ETH² rather than ETH.

If you don't know what a perpetual swap is, check out @apalepu23's primer. It's a great read.

firefly.exchange/blog/primer-on…

If you don't know what a perpetual swap is, check out @apalepu23's primer. It's a great read.

firefly.exchange/blog/primer-on…

Convexity:

Convexity is a cool word. It's also fundamental to understanding how Squeeth has a better payoff and less downside risk than 2x levered perps. In terms of options, convexity is also known as gamma.

@james_bachini shows the benefits of Squeeth's convexity below 👇

Convexity is a cool word. It's also fundamental to understanding how Squeeth has a better payoff and less downside risk than 2x levered perps. In terms of options, convexity is also known as gamma.

@james_bachini shows the benefits of Squeeth's convexity below 👇

Funding Rate & In-kind Funding

Once you understand Squeeth's funding mechanism, everything else becomes so much easier to understand! In short, if you buy Squeeth, in-kind funding is paid out of your position slowly over time.

More details:

Once you understand Squeeth's funding mechanism, everything else becomes so much easier to understand! In short, if you buy Squeeth, in-kind funding is paid out of your position slowly over time.

More details:

https://twitter.com/wadepros/status/1473724744398692353?s=20

Premium Funding <> Premium Yield

Remember the benefits of convexity? Compared to a 2x leveraged position, Squeeth funding rates are expected to be higher due to exposure to pure convexity.

The "premium funding" longs pay for convexity translates to "premium yield" for shorts!

Remember the benefits of convexity? Compared to a 2x leveraged position, Squeeth funding rates are expected to be higher due to exposure to pure convexity.

The "premium funding" longs pay for convexity translates to "premium yield" for shorts!

Long Squeth is a short to medium-term trade

The ideal market condition to hold Squeeth is when a trader has conviction in the upward price movement of ETH in the short to mid-term.

The ideal market condition to hold Squeeth is when a trader has conviction in the upward price movement of ETH in the short to mid-term.

Long Squeth is a short to medium-term trade

Holding a Long Squeeth position for an extended period (> 1 year), during which ETH trades sideways or goes down in value, will likely cause a loss in ETH² exposure due to in-kind funding paid to Short Squeeth sellers.

Holding a Long Squeeth position for an extended period (> 1 year), during which ETH trades sideways or goes down in value, will likely cause a loss in ETH² exposure due to in-kind funding paid to Short Squeeth sellers.

Short Squeeth is collateralized in ETH

At the recommended collateralization ratio of 200%, the ideal market condition to short Squeeth is when there is conviction the market is overpricing volatility and the price of ETH will trade sideways.

At the recommended collateralization ratio of 200%, the ideal market condition to short Squeeth is when there is conviction the market is overpricing volatility and the price of ETH will trade sideways.

Short Squeeth is collateralized in ETH

Right now long ETH short Squeeth at 200% collateralization ratio is close to delta neutral. If you can deposit USDC to borrow Squeeth and sell it, you can be truly short ETH delta and short the ETH² payoff

Right now long ETH short Squeeth at 200% collateralization ratio is close to delta neutral. If you can deposit USDC to borrow Squeeth and sell it, you can be truly short ETH delta and short the ETH² payoff

https://twitter.com/eulerfinance/status/1481315205011611648?s=20

Squeeth Strategies will make capturing premium yield more accessible to DeFi users. Users simply deposit ETH and the contract automatically manages the strategy. The Crab Strategy will be the first Squeeth Strategy to launch on January 24!

https://twitter.com/wadepros/status/1476973710150152194?s=20

Implied Volatility

Implied volatility is another important concept to grasp. The price of Squeeth can be used as a volatility oracle; a predictor of how much volatility we expect in ETH over the short term.

Check out @GenesisVol's video on IV 👇

Implied volatility is another important concept to grasp. The price of Squeeth can be used as a volatility oracle; a predictor of how much volatility we expect in ETH over the short term.

Check out @GenesisVol's video on IV 👇

A few helpful resources to learn more:

Squeeth Explained

Non quant 🧵 on Squeeth

Squeeth Primer

medium.com/opyn/squeeth-p…

Squeeth Explainer Video

Squeeth mental models

Squeeth Explained

https://twitter.com/AlphaSerpentis_/status/1479665823522463746?s=20

Non quant 🧵 on Squeeth

https://twitter.com/antonttc/status/1481265632918347780?s=20

Squeeth Primer

medium.com/opyn/squeeth-p…

Squeeth Explainer Video

Squeeth mental models

https://twitter.com/wadepros/status/1475621813988335618?s=20

• • •

Missing some Tweet in this thread? You can try to

force a refresh