If I have to name someone who taught me most about:

Risks, volatility and market cycles

It has to be Howard Marks from Oaktree Capital.

Buffett once said: "When I see memos from Howard Marks in my mail, they're the first thing I open and read."

Here are my key insights:

Risks, volatility and market cycles

It has to be Howard Marks from Oaktree Capital.

Buffett once said: "When I see memos from Howard Marks in my mail, they're the first thing I open and read."

Here are my key insights:

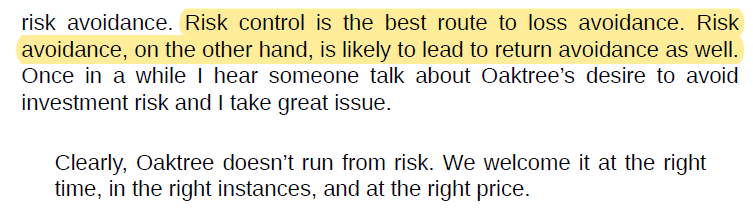

1. Risk Management

Investment isn't about avoiding risk altogether.

Risk-free investments will usually bring risk-free returns (mediocre).

Rather, we should think about managing risk instead using tools such as:

Diversification, rebalancing, long time horizon, etc.

Investment isn't about avoiding risk altogether.

Risk-free investments will usually bring risk-free returns (mediocre).

Rather, we should think about managing risk instead using tools such as:

Diversification, rebalancing, long time horizon, etc.

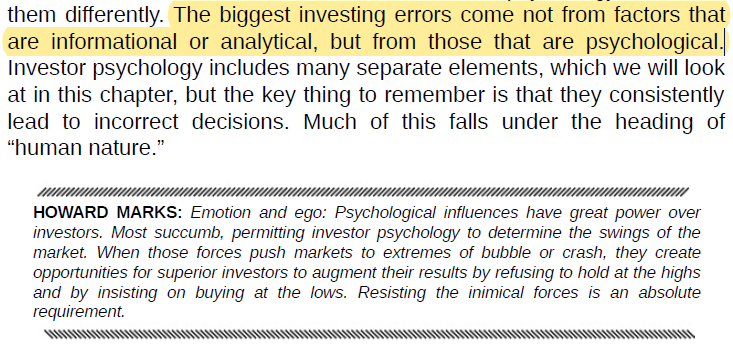

2. We are our own worst enemies

Investors make most of their mistakes not because of informational or analytical factors, but because of psychological ones.

The internet has made tons of information readily to all investors.

What counts is how we react to those information.

Investors make most of their mistakes not because of informational or analytical factors, but because of psychological ones.

The internet has made tons of information readily to all investors.

What counts is how we react to those information.

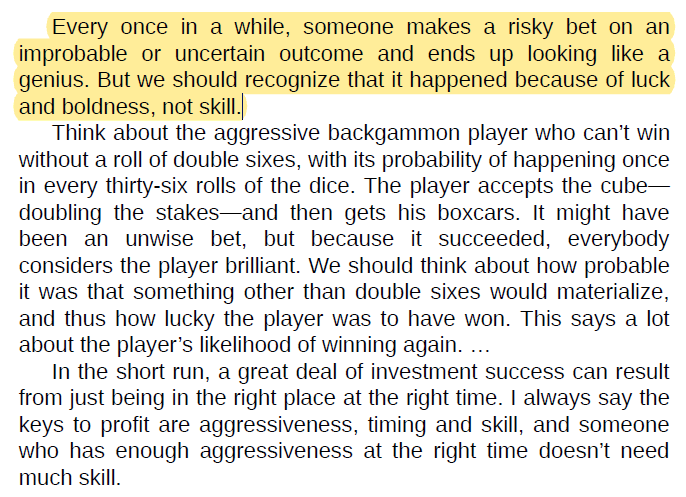

3. The difference between luck and skill

Don't follow an investor just because of great results for that year or two.

Investing like like a game of poker, not chess.

Success could be temporary due to luck.

Look into his/her investment process to determine if it makes sense.

Don't follow an investor just because of great results for that year or two.

Investing like like a game of poker, not chess.

Success could be temporary due to luck.

Look into his/her investment process to determine if it makes sense.

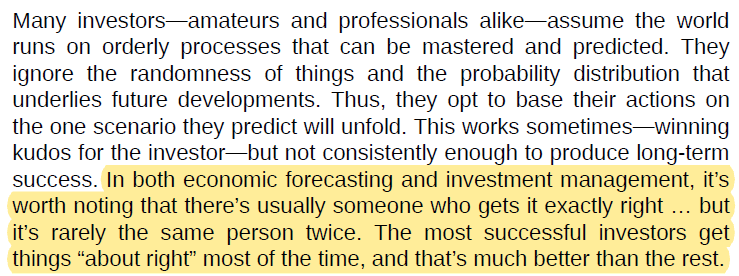

4. On forecasting

One recurring theme from great investors is that they ignore forecasts of all sorts.

It may be tempting to scratch the itch of thinking you can get a glimpse into the future by following gurus.

But remember, a broken clock is right twice a day.

One recurring theme from great investors is that they ignore forecasts of all sorts.

It may be tempting to scratch the itch of thinking you can get a glimpse into the future by following gurus.

But remember, a broken clock is right twice a day.

5. Human nature

The swing between greed and fear is ingrained in the market.

It often swings to excesses and then overcorrects.

The swing between greed and fear is ingrained in the market.

It often swings to excesses and then overcorrects.

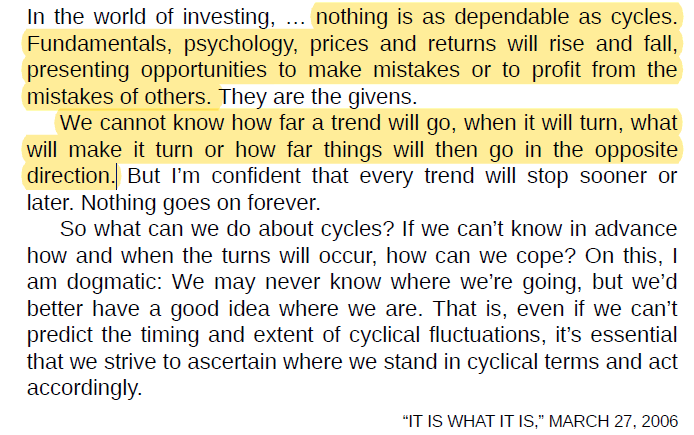

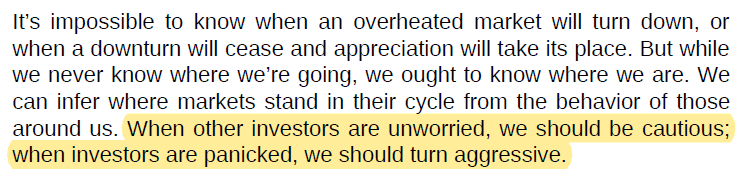

6. Switching between a cautious and aggressive mode

It's impossible to know when the tide will turn.

Many investors are paralyzed by indecision when a market does turn.

Market drawdowns often change the narrative of a business.

Even when fundamentally nothing has changed.

It's impossible to know when the tide will turn.

Many investors are paralyzed by indecision when a market does turn.

Market drawdowns often change the narrative of a business.

Even when fundamentally nothing has changed.

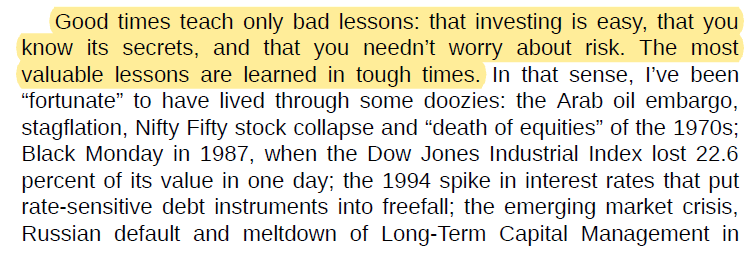

7. A bull market is a bad teacher

It makes you feel invincible, throws you off your position sizing and become aggressive with your forecasts.

Whenever there's a drawdown, make use of the opportunity to reflect and refine your investment philosophy.

It makes you feel invincible, throws you off your position sizing and become aggressive with your forecasts.

Whenever there's a drawdown, make use of the opportunity to reflect and refine your investment philosophy.

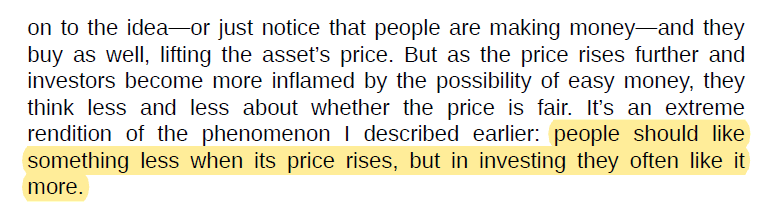

8. Rewire your brain to like low prices

People should like something less when its price rises, but in investing they often like it more.

If you are going to be a net saver for some time, you should welcome market declines!

People should like something less when its price rises, but in investing they often like it more.

If you are going to be a net saver for some time, you should welcome market declines!

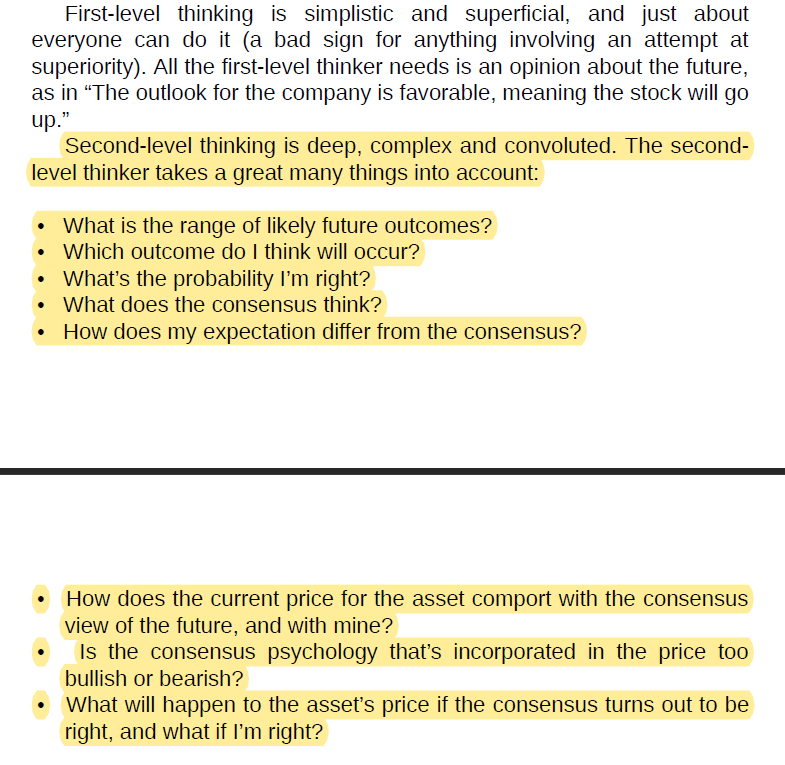

9. Second-level thinking

First-level thinkers look for simple formulas and easy answers.

Second-level thinkers know that success in investing is the antithesis of simple

It is deep, complex, and convoluted.

First-level thinkers look for simple formulas and easy answers.

Second-level thinkers know that success in investing is the antithesis of simple

It is deep, complex, and convoluted.

10. Anti-fragility

Develop a respect for tail-end risks.

Put yourself in a position where you are not forced out of the market even when shit hits the fence.

Do not:

-Borrow to invest

-Sell naked puts and calls

-Invest your emergency fund

Develop a respect for tail-end risks.

Put yourself in a position where you are not forced out of the market even when shit hits the fence.

Do not:

-Borrow to invest

-Sell naked puts and calls

-Invest your emergency fund

This is the end of my key takeaways from Howard Marks' memos!

I hope you enjoyed it.

If you like this, follow me here @steadycompound

I write about investment concepts, business breakdowns and growth philosophies.

I hope you enjoyed it.

If you like this, follow me here @steadycompound

I write about investment concepts, business breakdowns and growth philosophies.

Investoholics are going to enjoy my newsletter where I share my thoughts and the most insightful information I discovered in the past week.

steadycompounding.com

steadycompounding.com

For the uninitiated, Howard Marks has a favorite catchphrase:

"The most important is...."

And then he'll go on to list and explain all those things.

Over the years, this phrase eventually morphed into the title of his book.

amzn.to/3riKKAT

"The most important is...."

And then he'll go on to list and explain all those things.

Over the years, this phrase eventually morphed into the title of his book.

amzn.to/3riKKAT

• • •

Missing some Tweet in this thread? You can try to

force a refresh