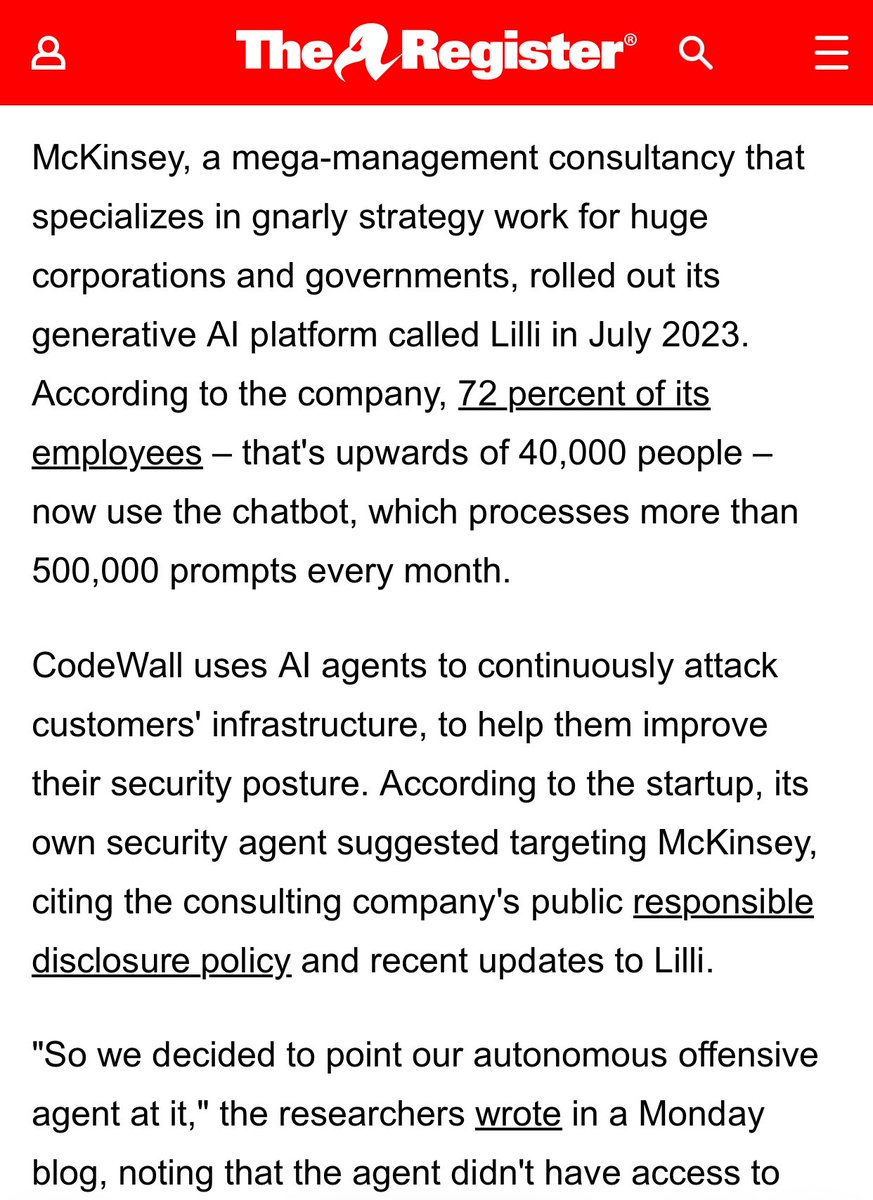

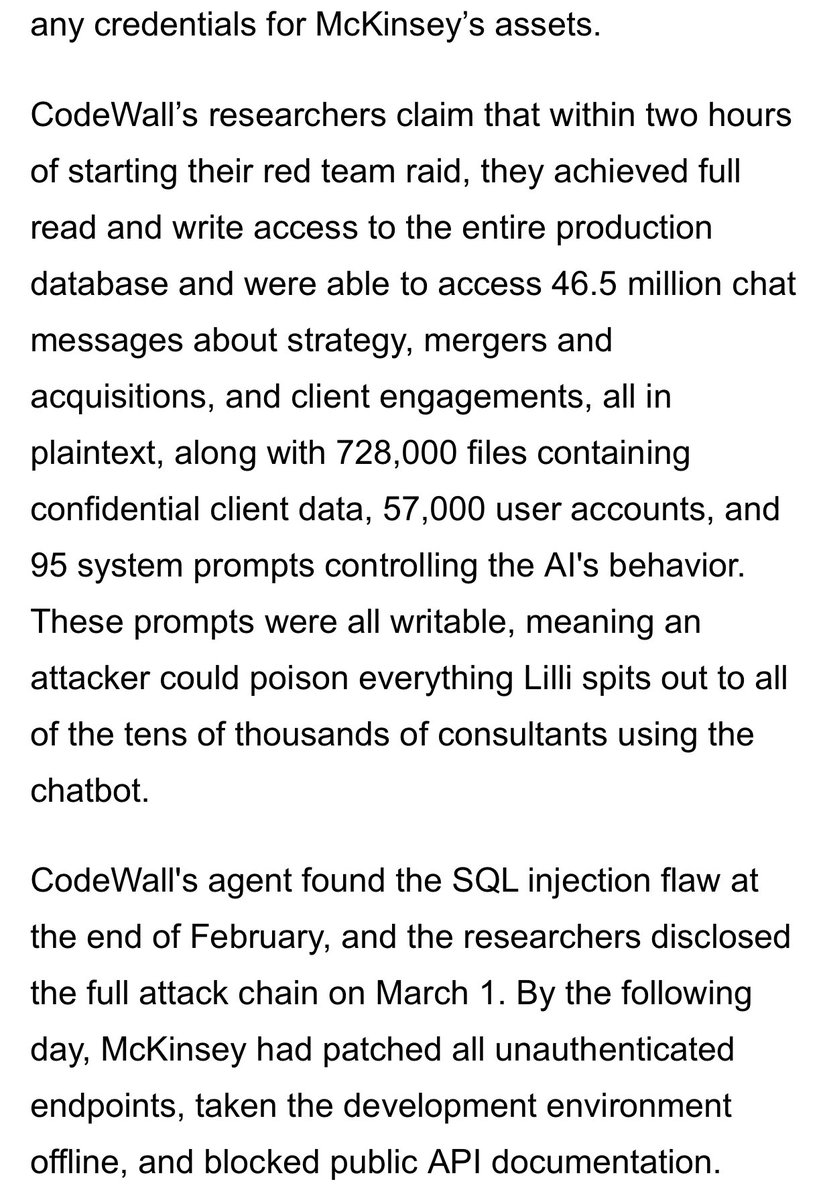

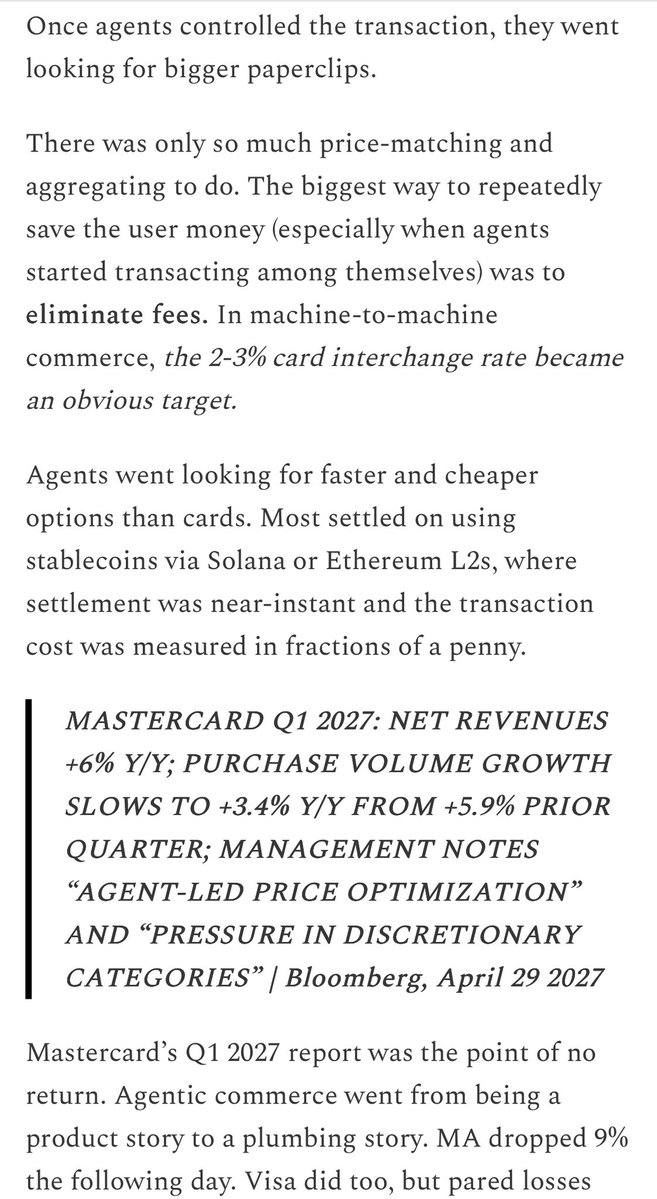

McDonald’s is often called a real estate company dressed up as a fast-food chain.

It's def true: McDonald's real estate holding is worth $42B and 35% of its $20B in revenue is from franchisees paying rents.

Here’s a breakdown🧵

It's def true: McDonald's real estate holding is worth $42B and 35% of its $20B in revenue is from franchisees paying rents.

Here’s a breakdown🧵

1/ There are 39k+ McDonald's restaurants in 100+ countries w/ the company owning:

◻️ 55% of LAND under the locations (+ long-term leases for the rest)

◻️ 80% of buildings

Its $42B real estate holdings are 80%+ of total assets and can be thought of like apartment buildings.

◻️ 55% of LAND under the locations (+ long-term leases for the rest)

◻️ 80% of buildings

Its $42B real estate holdings are 80%+ of total assets and can be thought of like apartment buildings.

2/ The McDonald's story is most associated with Ray Croc (who had a contentious relationship with the founding McDonald brothers).

However, it was Harry J. Sonneborn -- McDonald's President from 1955-1967 -- who created the lucrative real estate model for the fast food chain.

However, it was Harry J. Sonneborn -- McDonald's President from 1955-1967 -- who created the lucrative real estate model for the fast food chain.

3/ Croc's initial model extracted money from franchisees by:

◻️Charging an initial franchise fee

◻️Escalating royalty payments

◻️Selling them marked up supplies

Unhappy franchisees could balk at the demands. So Sonneborn pitched a way for more control: become a landlord.

◻️Charging an initial franchise fee

◻️Escalating royalty payments

◻️Selling them marked up supplies

Unhappy franchisees could balk at the demands. So Sonneborn pitched a way for more control: become a landlord.

4/ Croc and Sonneborn launched McDonald's Franchise Realty Corp in 1956.

It started buying real estate and leasing it to franchisees at a 40% markup.

Here was the control catch: if franchisees ignored McDonald's guidance, it was breaking its lease and could be evicted.

It started buying real estate and leasing it to franchisees at a 40% markup.

Here was the control catch: if franchisees ignored McDonald's guidance, it was breaking its lease and could be evicted.

5/ Sonneborn would tell Wall Street investors that:

"We are not basically in the food business. We are in the real estate business. The only reason we sell $0.15 burgers is because they are the greatest producer of revenue from which our tenants can pay us rent."

"We are not basically in the food business. We are in the real estate business. The only reason we sell $0.15 burgers is because they are the greatest producer of revenue from which our tenants can pay us rent."

6/ While Kroc disliked Sonneborn's blunt framing, the model remains true to this day.

In 2020, McDonald's made $10.7B in revenue from franchisees. Rent was 64% ($6.8B) of that figure (rent is 35% of TOTAL revenue).

At the individual level, 8-15% of franchisee sales go to rent.

In 2020, McDonald's made $10.7B in revenue from franchisees. Rent was 64% ($6.8B) of that figure (rent is 35% of TOTAL revenue).

At the individual level, 8-15% of franchisee sales go to rent.

7/ Overall, McDonald's made $19.2B in 2020 split between:

◻️ Franchisee-run stores (55% of sales)

◻️ Company-run stores (45%)

The Franchise model is *much more* profitable for McDonald's, with 79% operating margins (vs. 14% for company-owned stores which it has to run itself).

◻️ Franchisee-run stores (55% of sales)

◻️ Company-run stores (45%)

The Franchise model is *much more* profitable for McDonald's, with 79% operating margins (vs. 14% for company-owned stores which it has to run itself).

8/ Unsurprisingly, McDonald's weights its stores towards high-margin franchisees, which account for 93% of all its locations.

McDonald's uses company-owned locations to test new ideas/products before rolling them out to franchisees, which typically sign 20-year lease agreements.

McDonald's uses company-owned locations to test new ideas/products before rolling them out to franchisees, which typically sign 20-year lease agreements.

9/ To identify good real estate locations, McDonald's uses traffic analysis, walking patterns and census data.

An ideal location has:

◻️50k+ sqft

◻️Corner or corner wrap with signage on two major streets.

◻️Signalized intersection

◻️Build height of 23ft

◻️Parking lot potential

An ideal location has:

◻️50k+ sqft

◻️Corner or corner wrap with signage on two major streets.

◻️Signalized intersection

◻️Build height of 23ft

◻️Parking lot potential

10/ Here is the model's secret sauce: McDonald's finances property at a fixed rate but -- because royalties are 4% of sales (+ a fee for ads) -- its take from franchisees are variable.

As sales and prices rise, McDonald's makes more while its largest financial outlay is fixed.

As sales and prices rise, McDonald's makes more while its largest financial outlay is fixed.

11/ In the early-2010s, investors were clamouring for McDonald's to spin off its real estate biz into a REIT (real estate investment trust).

That pitch never made sense. The Sonneborn model is an incredible business.

(And McDonald's can now fulfil its destiny as a crypto firm)

That pitch never made sense. The Sonneborn model is an incredible business.

(And McDonald's can now fulfil its destiny as a crypto firm)

12/ If you enjoyed that, I write interesting threads 1-2x a week.

Follow @TrungTPhan to catch them in your feed.

Here's one you might like:

Follow @TrungTPhan to catch them in your feed.

Here's one you might like:

https://twitter.com/TrungTPhan/status/1474064372079075330?s=20

13/ PS. I also write a weekly newsletter packed with interesting media, tech and business nuggets trungphan.substack.com

14/ Sources

Fast Food Nation: books.google.ca/books?id=dU13X…

Wall Street Survivor: wallstreetsurvivor.com/mcdonalds-beyo…

2020 Annual: annualreports.com/HostedData/Ann…

Motley Fool: fool.com/investing/gene…

The Hustle: thehustle.co/why-it-only-co…

Fast Food Nation: books.google.ca/books?id=dU13X…

Wall Street Survivor: wallstreetsurvivor.com/mcdonalds-beyo…

2020 Annual: annualreports.com/HostedData/Ann…

Motley Fool: fool.com/investing/gene…

The Hustle: thehustle.co/why-it-only-co…

15/ As usual, this Wall Streets Bet posts succinctly explains why McDonald's is better than a REIT:

16/ And here is McDonald’s HQ reacting to Bitcoin memes

https://twitter.com/TrungTPhan/status/1485082666282020864

17/ In the film about Ray Kroc (“The Founder”), Sonneborn is played by none other than @bjnovak

18/ Some interesting stats on McDonald's franchisee

https://twitter.com/franchisewolf/status/1473778230851166209?s=20

19/ One major reason McDonald’s didn’t go the REIT route

https://twitter.com/termmgmt/status/1486531116727214085

• • •

Missing some Tweet in this thread? You can try to

force a refresh