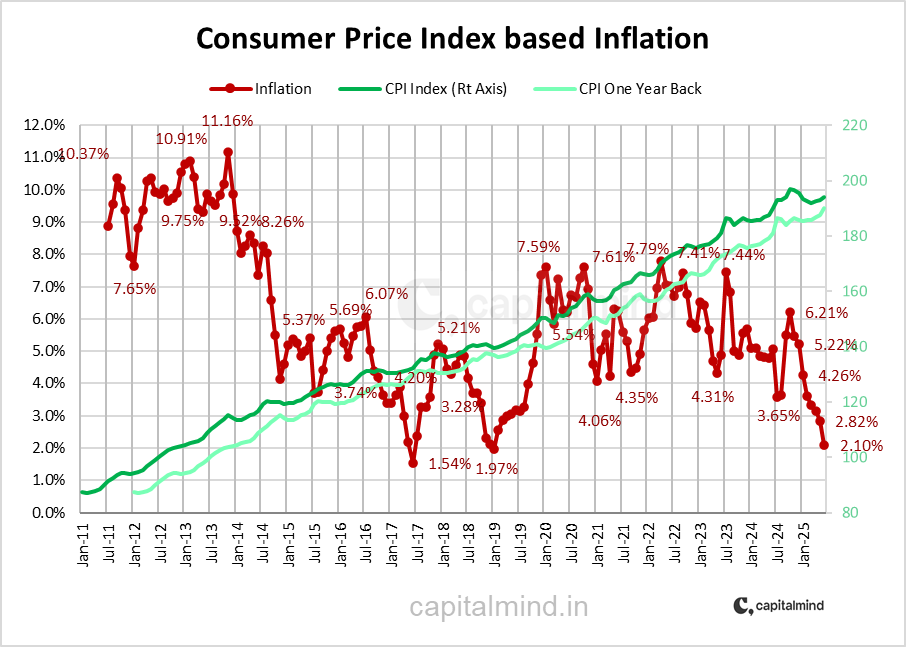

A thread 🧵on how much retail investors (individuals) dominate daily investing in the markets in India, from the NSE Pulse: static.nseindia.com//s3fs-public/i…

They're 41% of the stock market transactions - down from 45% in 2020-21. Still, massive.

They're 41% of the stock market transactions - down from 45% in 2020-21. Still, massive.

Individuals are 29% of index futures - a big drop from 39% in FY 21 and give way to brokers (PRO).

They give way to FIIs and PRO in the stock futures segment, down to just 19% in FY22 (which is April 2021 to March 2022)

Clearly, those straddle and strangle videos are working - individuals are more than 1/3rd the index option market. FIIs said goodbye, and brokers also love this market. This is a source of worry - it's also the most leveraged segment (indexes have low IVs, so leverage is high)

Individuals love them stock options too, and together with brokers prop accounts, are over 80% of the market.

But none of this means they hold stocks.

🕴️♂️Promoters own 51% of stocks.

🤵 FIIs own 21%!

💼Mutual funds/Insurers 15%

🥷Retail investors 9.3%

(Rest is others)

🕴️♂️Promoters own 51% of stocks.

🤵 FIIs own 21%!

💼Mutual funds/Insurers 15%

🥷Retail investors 9.3%

(Rest is others)

FIIs own more than Mutual funds+Retail investors added up. Very different from the trading data where Retail investors is more than double of FIIs+Mutual Funds.

But might be changing. Here's mutual fund SIPs every month:

But might be changing. Here's mutual fund SIPs every month:

That's the end. Oh, do check out get.capitalmind.in/premium for Premium and get.capitalmind.in/wealth for our PMS.

• • •

Missing some Tweet in this thread? You can try to

force a refresh