$FB (now $META) Q4 results:

Revenue: 33.7B vs 33.4B (beat)

EBIT: 12.6B vs 13.1B (miss)

Net Income: 10.3B vs 11B (miss)

EPS: $3.72 vs $3.83 (miss)

DAP: 2.82B, up 8% yoy

MAP: 3.59B, up 9% yoy

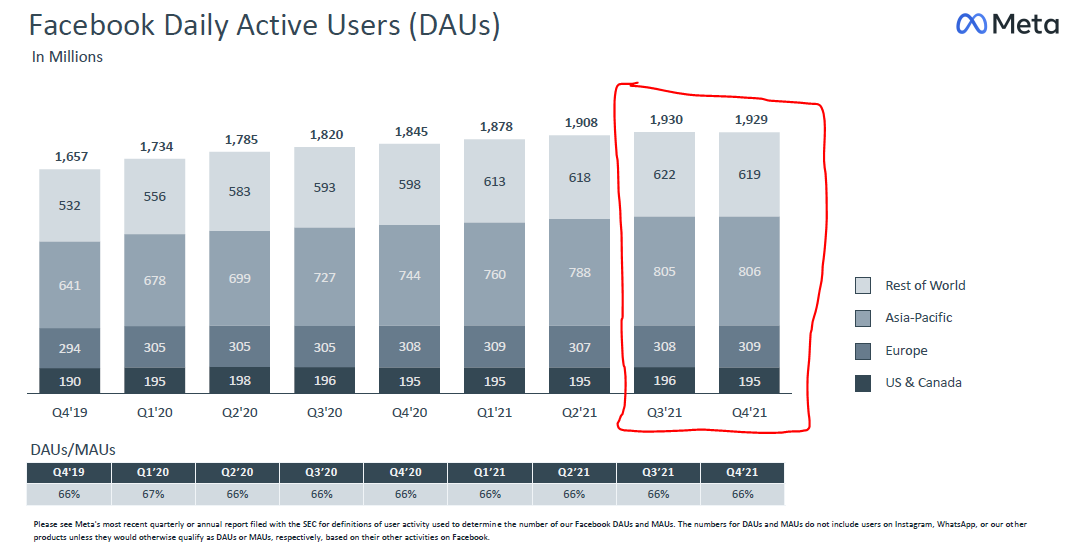

DAUs: 1.93B, up 5% yoy

MAUs: 2.91B, up 4% yoy

Revenue: 33.7B vs 33.4B (beat)

EBIT: 12.6B vs 13.1B (miss)

Net Income: 10.3B vs 11B (miss)

EPS: $3.72 vs $3.83 (miss)

DAP: 2.82B, up 8% yoy

MAP: 3.59B, up 9% yoy

DAUs: 1.93B, up 5% yoy

MAUs: 2.91B, up 4% yoy

Ad impressions: Up 13% yoy

Price per ad: Up 6% yoy

Headcount: 71,970 up 23%

Share repurchases: $19.18B in Q4 21

Total shares repurchased for full year 2021: $44.81B

$38.79B left in the tank for more share repurchases.

Price per ad: Up 6% yoy

Headcount: 71,970 up 23%

Share repurchases: $19.18B in Q4 21

Total shares repurchased for full year 2021: $44.81B

$38.79B left in the tank for more share repurchases.

Similar to the shift from desktop feed to mobile feed and to stories, Mark is leading the next pivot into Reels.

It will further cannibalize its ad revenue from feed in the short-term but this move is key to capturing younger adults.

It will further cannibalize its ad revenue from feed in the short-term but this move is key to capturing younger adults.

Users are increasingly sharing content via DMs rather than posting on public feeds.

Important for Mark to strengthen WhatsApp's and DMs infrastructure and figure out a way how to better monetize this segment as users spend more time in community groups.

Important for Mark to strengthen WhatsApp's and DMs infrastructure and figure out a way how to better monetize this segment as users spend more time in community groups.

Headwinds highlighted:

•Competition (Tiktok)

•Apple iOS changes

•Slowdown in ecommerce growth

•Supply chain disruptions, tight labor market & inflation

•Competition (Tiktok)

•Apple iOS changes

•Slowdown in ecommerce growth

•Supply chain disruptions, tight labor market & inflation

iOS changes caused two problems:

•Less targeted ad

•Tougher to track conversions for advertisers

The former results in less ROI for advertisers.

The latter results in underestimating the ROI.

•Less targeted ad

•Tougher to track conversions for advertisers

The former results in less ROI for advertisers.

The latter results in underestimating the ROI.

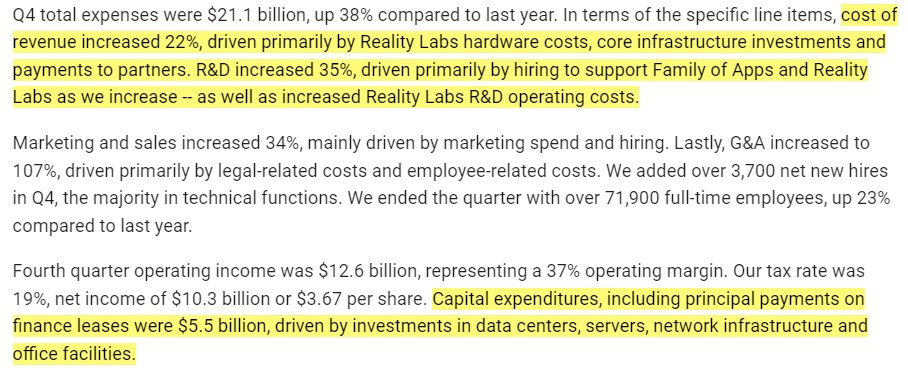

Beat on revenue but missed on EBIT and EPS estimates largely due to heavy investment into the Metaverse.

Imo, missing the estimates not a real concern here.

More important to focus on how they navigate competition (Tiktok) and iOS changes.

Imo, missing the estimates not a real concern here.

More important to focus on how they navigate competition (Tiktok) and iOS changes.

First drop off in DAUs?!

Growth in Asia, particularly in India, seems to be strongly affected by Tiktok and to lesser extent, increase in data package pricing as the telco war in India ease off.

Growth in Asia, particularly in India, seems to be strongly affected by Tiktok and to lesser extent, increase in data package pricing as the telco war in India ease off.

Management retracting from their earlier statement on the iOS changes.

Earlier they highlighted that iOS changes would make FB platform stronger vis-à-vis other platforms.

Now they estimate iOS to cost them $10B.

Earlier they highlighted that iOS changes would make FB platform stronger vis-à-vis other platforms.

Now they estimate iOS to cost them $10B.

Why Google is unscathed from iOS changes:

They pay >$10B to Apple each year to remain the default search engine on iPhones.

May FB should've just paid a "tax" to Apple too, considering the cost from iOS changes is around $10B.

They pay >$10B to Apple each year to remain the default search engine on iPhones.

May FB should've just paid a "tax" to Apple too, considering the cost from iOS changes is around $10B.

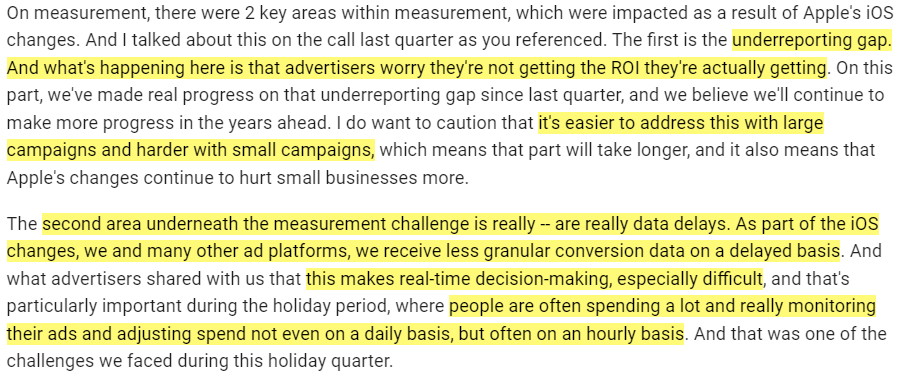

With the iOS changes, advertisers are finding it a lot tougher to measure their ROI on marketing spend.

This becomes critical during sales season as advertisers are monitoring their ROI and deciding whether to increase spend on an hourly basis.

This becomes critical during sales season as advertisers are monitoring their ROI and deciding whether to increase spend on an hourly basis.

My reflections on $META earnings

https://twitter.com/SteadyCompound/status/1489229729869799432?t=8LC4WM35GXzup5rTBF2V6Q&s=19

• • •

Missing some Tweet in this thread? You can try to

force a refresh