Warren Buffett 2021 letter has dropped!

Buffett's letters since his partnership years are jammed with insights.

And he taught me more than any business school ever could.

This year is no different.

Here are my key insights:

Buffett's letters since his partnership years are jammed with insights.

And he taught me more than any business school ever could.

This year is no different.

Here are my key insights:

1. Buffett and Munger's investing philosophy

Their goal is to look for businesses with both durable economic advantages and a first-class CEO.

Their goal is to look for businesses with both durable economic advantages and a first-class CEO.

2. Pick the right businesses and the stock price will take care of itself.

"...we own stocks based upon our expectations about their long-term business performance and not because we view them as vehicles for timely market moves."

"...we own stocks based upon our expectations about their long-term business performance and not because we view them as vehicles for timely market moves."

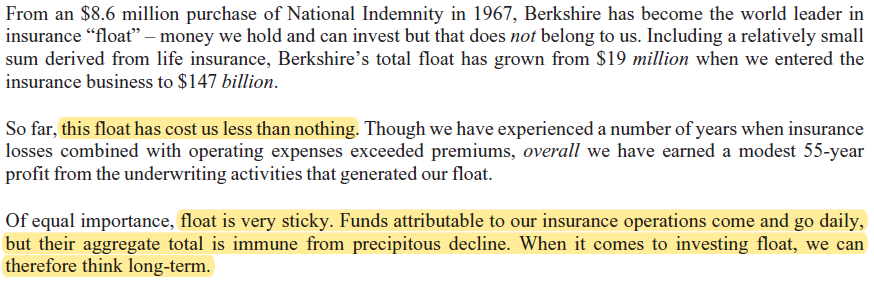

3. Warren uses leverage...

With his insurance businesses!

So far this leverage (aka float) has:

•Cost him nothing

•Gave him a sticky source of capital

The latter is important.

A sticky source of capital allows Buffett to make long-term investments.

With his insurance businesses!

So far this leverage (aka float) has:

•Cost him nothing

•Gave him a sticky source of capital

The latter is important.

A sticky source of capital allows Buffett to make long-term investments.

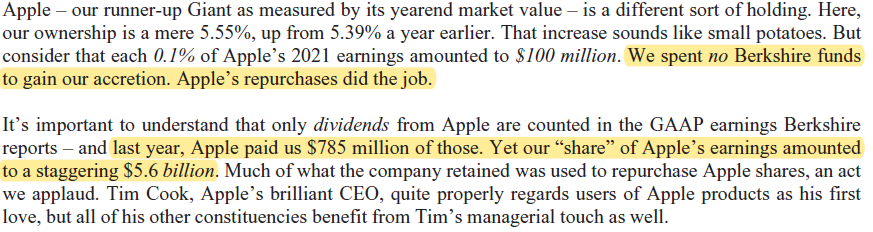

4. Look-through earnings

$BRK owns 5.39% of $APPL

But its share of earnings isn't fully captured on its income statement.

Only the dividends is received.

But don't forget...

There's the retained earnings which is ploughed into share buybacks & reinvestment.

$BRK owns 5.39% of $APPL

But its share of earnings isn't fully captured on its income statement.

Only the dividends is received.

But don't forget...

There's the retained earnings which is ploughed into share buybacks & reinvestment.

5. Why Buffett loves the insurance business

Because it fits Buffett's rule for investing...

A company that can generate durable growth and it's tough for competitors to catch up with them!

Because it fits Buffett's rule for investing...

A company that can generate durable growth and it's tough for competitors to catch up with them!

6. How Buffett likes his earnings

TLDR; After ALL expenses have been accounted for.

TLDR; After ALL expenses have been accounted for.

7. THREE ways to increase $BRK value

1) Increase earnings power of wholly owned businesses or make more acquisitions

2) Buy shares of publicly listed businesses

3) Repurchase $BRK shares

More on repurchasing $BRK shares...

1) Increase earnings power of wholly owned businesses or make more acquisitions

2) Buy shares of publicly listed businesses

3) Repurchase $BRK shares

More on repurchasing $BRK shares...

In Buffett's 1999 letter, he outlines the conditions required for share repurchases to be value accretive:

1) The company has available funds—cash plus sensible borrowing capacity, AND

2) Its stock is selling in the market below its intrinsic value, conservatively-calculated.

1) The company has available funds—cash plus sensible borrowing capacity, AND

2) Its stock is selling in the market below its intrinsic value, conservatively-calculated.

8. Why Buffett loves teaching

Buffett started teaching investing 70 years ago.

"Teaching, like writing, has helped me develop and clarify my own thoughts."

@heymaxkoh and I will be teaming up to teach investing.

If you are interested, let us know by dropping a 🚀 below!

Buffett started teaching investing 70 years ago.

"Teaching, like writing, has helped me develop and clarify my own thoughts."

@heymaxkoh and I will be teaming up to teach investing.

If you are interested, let us know by dropping a 🚀 below!

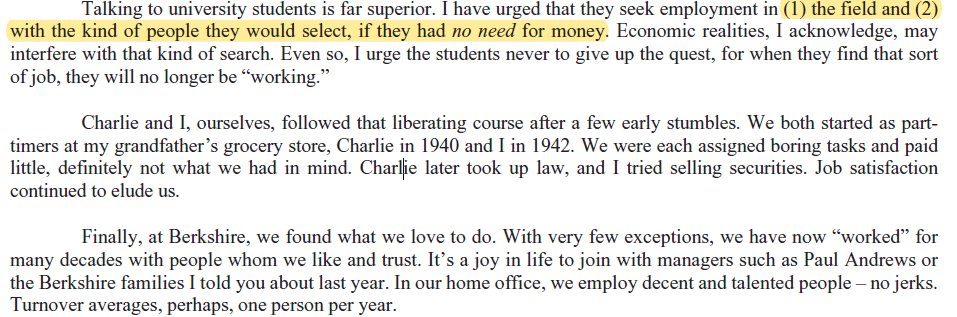

@heymaxkoh 9. Career advice for university students

Seek employment in:

1) the field and

2) with the kind of people they would select....

If they had no need for money.

It's not easy. But don't give up on the quest to hunt for a job where they will no longer be "working".

Seek employment in:

1) the field and

2) with the kind of people they would select....

If they had no need for money.

It's not easy. But don't give up on the quest to hunt for a job where they will no longer be "working".

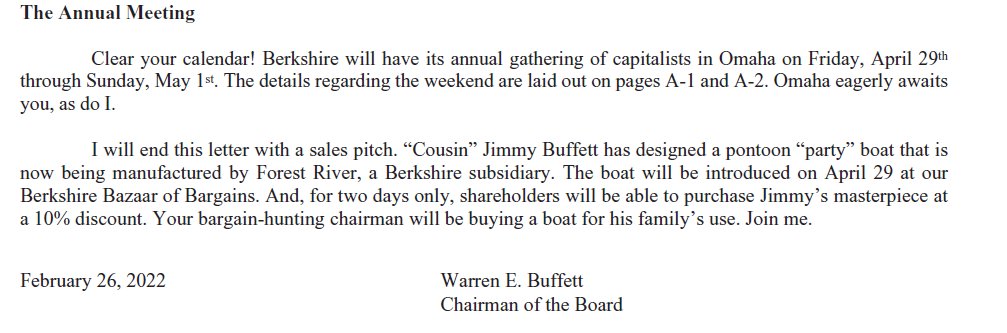

@heymaxkoh 10. The upcoming $BRK meeting...

Will be a PHYSICAL one!

In Omaha on Friday, Apr 29 through Sunday, May 1.

Will be a PHYSICAL one!

In Omaha on Friday, Apr 29 through Sunday, May 1.

@heymaxkoh Not enough of Buffett's wisdom?

Then check out my mega thread on ALL of Buffett's $BRK letters.

I distill his insights from 1977 to 2020 here:

Then check out my mega thread on ALL of Buffett's $BRK letters.

I distill his insights from 1977 to 2020 here:

https://twitter.com/SteadyCompound/status/1477401315877822476

@heymaxkoh This is the end of my key takeaways from Buffett's letters!

I hope you enjoyed it.

If you like this, follow me here @steadycompound

I write about investment concepts, business breakdowns and growth philosophies.

I hope you enjoyed it.

If you like this, follow me here @steadycompound

I write about investment concepts, business breakdowns and growth philosophies.

@heymaxkoh If you have enjoyed this thread, you're gonna love my newsletter where I curate 3 ideas on investing and growth philosophies.

Every week.

steadycompounding.com

Every week.

steadycompounding.com

• • •

Missing some Tweet in this thread? You can try to

force a refresh