China’s property crisis is spilling over to some of its stronger builders, leaving investors with even fewer places to hide.

Analysts are warning of an “unstoppable downward spiral.” 1/5

Read my latest breakdown in Bloomberg’s China credit tracker 👇

bloomberg.com/graphics/china…

Analysts are warning of an “unstoppable downward spiral.” 1/5

Read my latest breakdown in Bloomberg’s China credit tracker 👇

bloomberg.com/graphics/china…

China’s developers have been rocked by at least 14 defaults since authorities began cracking down on the housing market in 2020.

Authorities are allowing selective policy relief but that’s had very little effect on credit markets. 2/5

Authorities are allowing selective policy relief but that’s had very little effect on credit markets. 2/5

Traders betting on better times ahead for China property are in a difficult position now that builders once shielded from the wild swings look increasingly vulnerable. (Made worse by global risk-off following the invasion of Ukraine.)

That’s keeping stress elevated offshore 3/5

That’s keeping stress elevated offshore 3/5

A painful reminder of how far and fast a Chinese developer can fall: luxury builder Shimao was once a bellwether for China’s safer builders. In a matter of months it was slashed deep into junk from investment grade. It’s now rated CCC 4/5

bloomberg.com/news/articles/…

bloomberg.com/news/articles/…

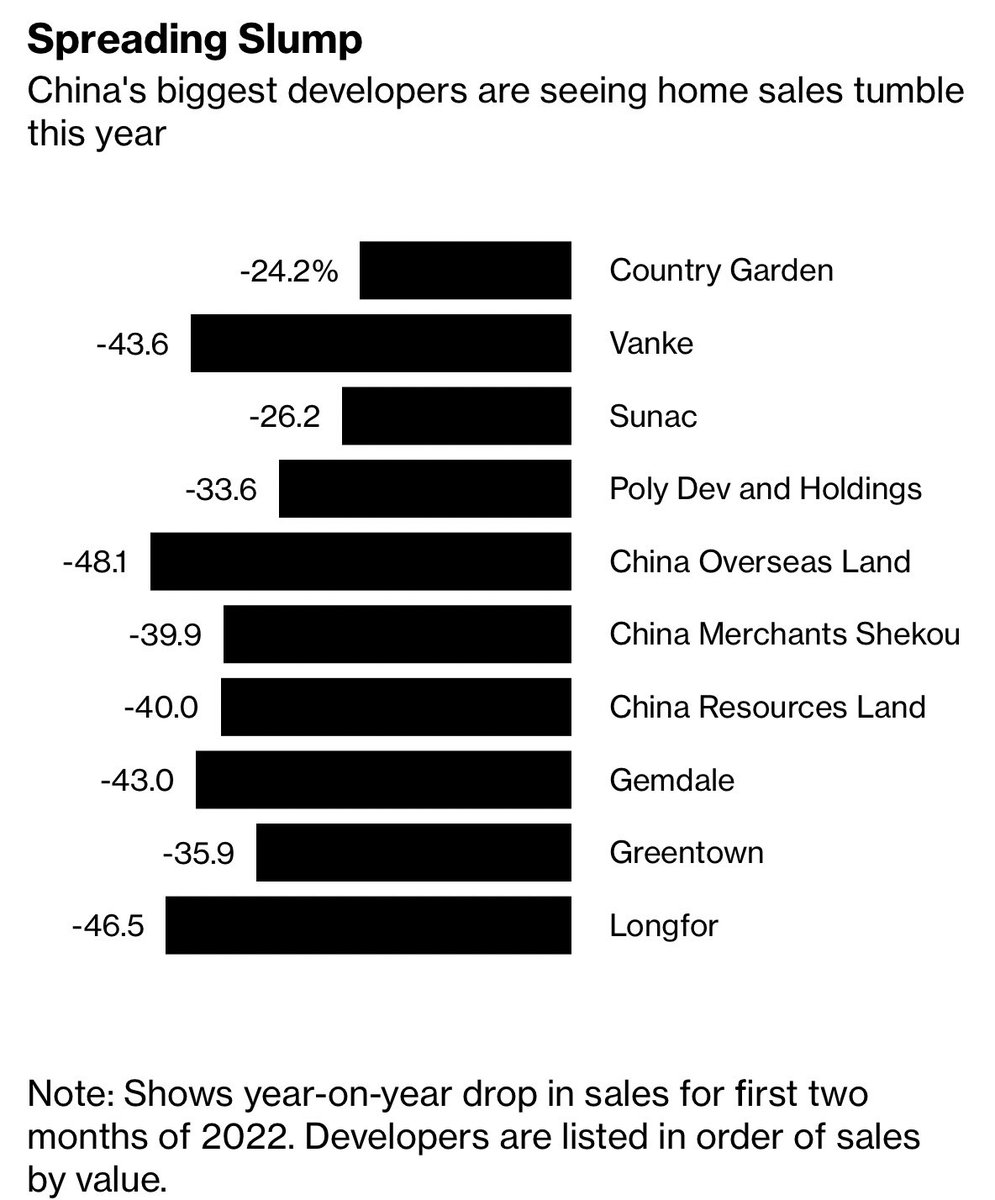

Longer-term prospects for China’s largest builders look bleak. Home sales by some of these firms tumbled during the first two months of this year. Country Garden, the nation’s largest developer, saw sales fall 24%. Vanke sales, the second-biggest, declined 44%. 5/5

Analysts are once again warning of a further correction. The next month will be key. A wave of debt obligations in March—stressed Chinese developers face a $3.7b debt bill— is likely to spur fresh pressure with fund raising options still limited for many firms. 6/5

• • •

Missing some Tweet in this thread? You can try to

force a refresh