0/ Now that the FOMC chopfest is out the way.

Here is our FX & Rates Roundup 🧵👇

Here is our FX & Rates Roundup 🧵👇

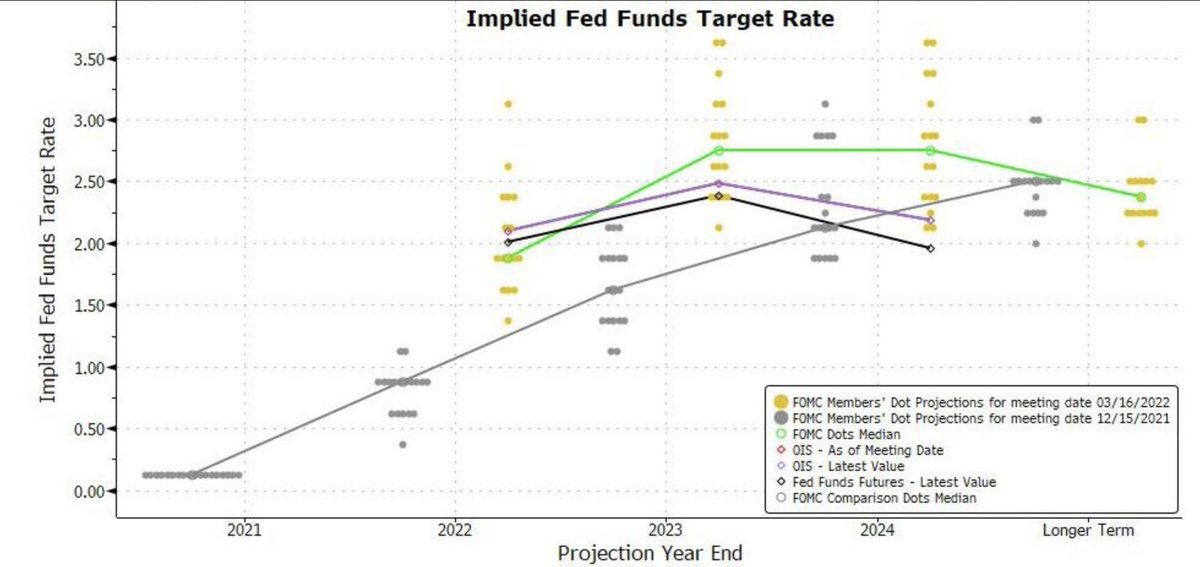

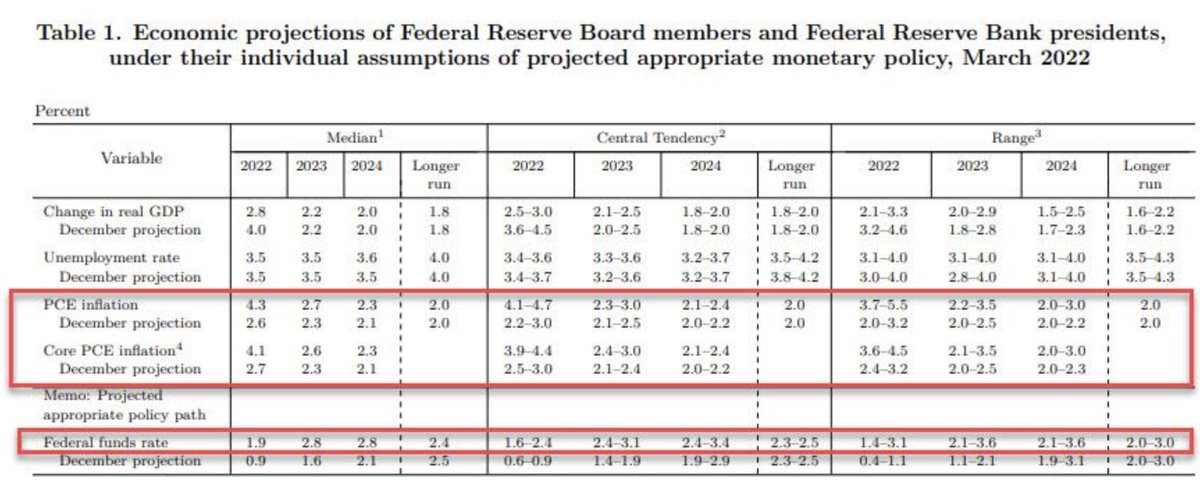

1/ Markets were expecting 25bps hike, likely some hawkish guidance to get back some credibility (good luck!), higher dot plot to meet the market pricing and QT guidance. Well we got the higher dots...

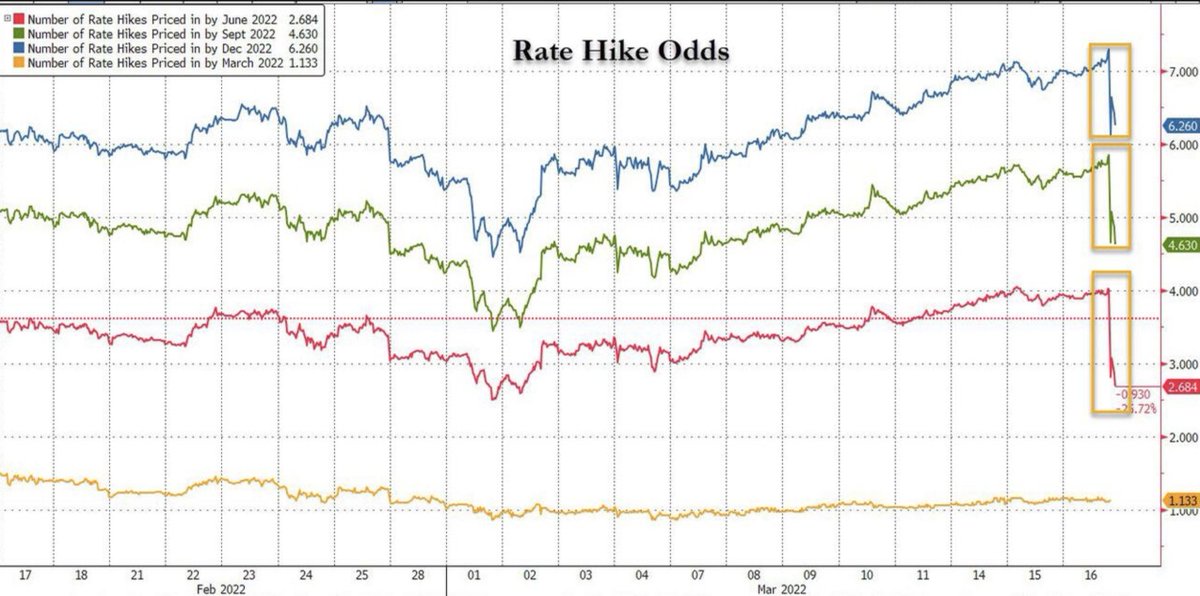

2/ Markets however decided that confirmation of hiking at every meeting this year was reason to be concerned, given just how bad the FED have been at predicting inflation dynamics. Hike probabilities for this year actually came down. Sell the news!

3/ This dovish move in short rates after the presser along with 5s10s inverting triggered "risk on" across asset classes with DXY lower, stocks, gold and crypto higher.

4/ USDJPY recent breakout on Kuroda ruling out hikes this week. This could have some legs as CB policies diverge so dramatically.

5/ The unstoppable trend of yield curve flattening continued with 2s10s flatter by 5bps to 25 bps. Not much wiggle room before we see an inversion which many will call a recession signal.

6/ These type of whipsaw moves on FOMC day are quite normal and often it's more about positioning than the actual fundamentals. Overall, Powell confirmed stagflation risk is high, market decided to rally. Lower growth, higher inflation, not a great combination.

7/ If you like this thread pls RT and be sure to try out our community by joining our FREE Discord group chat (discord.com/invite/dsnhDWS…) to join the conversation and get info like this & more in real-time.

• • •

Missing some Tweet in this thread? You can try to

force a refresh