Many people refer to Terry Smith as the "English Warren Buffett".

He spoke at Fundsmith's latest Annual Shareholder Meeting about:

•His stake in $AMZN, $FB & $GOOGL

•Why he continues to hold $PYPL

•Inflation & interest rates

• Ukraine-Russia war

Here are my notes:

He spoke at Fundsmith's latest Annual Shareholder Meeting about:

•His stake in $AMZN, $FB & $GOOGL

•Why he continues to hold $PYPL

•Inflation & interest rates

• Ukraine-Russia war

Here are my notes:

1. Pandemic has caused quite a bit of distortions

To overcome the distortions, evaluate businesses (and the fund results) based on two-year stacks.

I.e. How has the company/fund done compared to 2019?

Rather than looking at the YoY performance.

To overcome the distortions, evaluate businesses (and the fund results) based on two-year stacks.

I.e. How has the company/fund done compared to 2019?

Rather than looking at the YoY performance.

2. Winners keep winning

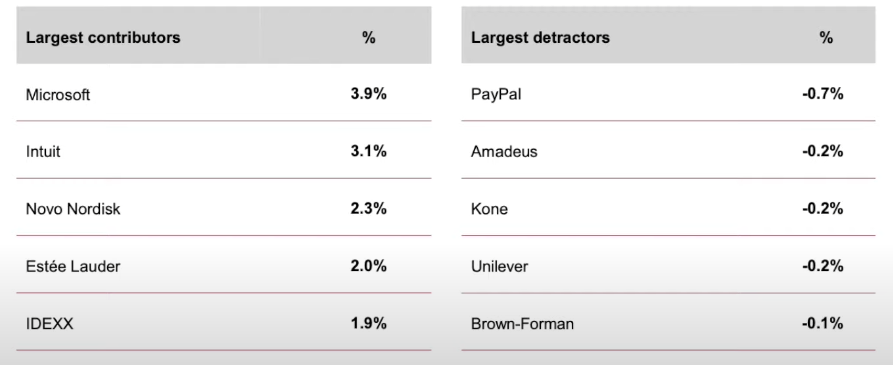

$MSFT has made its 7th appearance to be the top contributor to the fund's performance.

Run your winners.

Water your flowers and pull out your weeds.

Not the opposite (which many do).

$MSFT has made its 7th appearance to be the top contributor to the fund's performance.

Run your winners.

Water your flowers and pull out your weeds.

Not the opposite (which many do).

4. On $PYPL

Multiple years of success except for recent months.

Still a strong business with a great market position.

But management lost their way with acquisitions.

Should have focused on getting its users to use PayPal more frequently instead.

Multiple years of success except for recent months.

Still a strong business with a great market position.

But management lost their way with acquisitions.

Should have focused on getting its users to use PayPal more frequently instead.

5. On Amadeus

Airline reservations continue to be problematic which led to underperformance.

Continue holding as it will survive and emerge stronger with a more powerful market position.

Largely because they are better financed than its competitors.

Airline reservations continue to be problematic which led to underperformance.

Continue holding as it will survive and emerge stronger with a more powerful market position.

Largely because they are better financed than its competitors.

6. On Valuation

A Ford doesn't price the same as a Ferrari

The fact that one is priced lower than the other doesn't in itself tell you anything about the bargain you are getting.

We need to examine other factors such as growth & quality as well.

A Ford doesn't price the same as a Ferrari

The fact that one is priced lower than the other doesn't in itself tell you anything about the bargain you are getting.

We need to examine other factors such as growth & quality as well.

7. New Position in $GOOGL

On top of $FB, another route for them to get into the digital advertising market.

Continues to take share away from traditional advertising.

Third largest player in the cloud computing infrastructure market.

On top of $FB, another route for them to get into the digital advertising market.

Continues to take share away from traditional advertising.

Third largest player in the cloud computing infrastructure market.

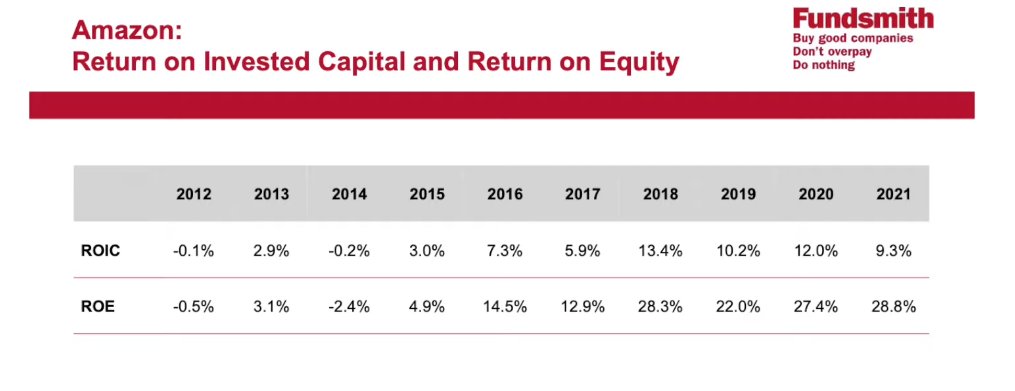

8. New Position in $AMZN

AWS is highly profitable and has decades of growth.

Profitable 3P transactions have increased significantly (56% of sales).

Prime members has 200m members and is a powerful profit driver.

Advertising segment benefits strongly from ATT.

AWS is highly profitable and has decades of growth.

Profitable 3P transactions have increased significantly (56% of sales).

Prime members has 200m members and is a powerful profit driver.

Advertising segment benefits strongly from ATT.

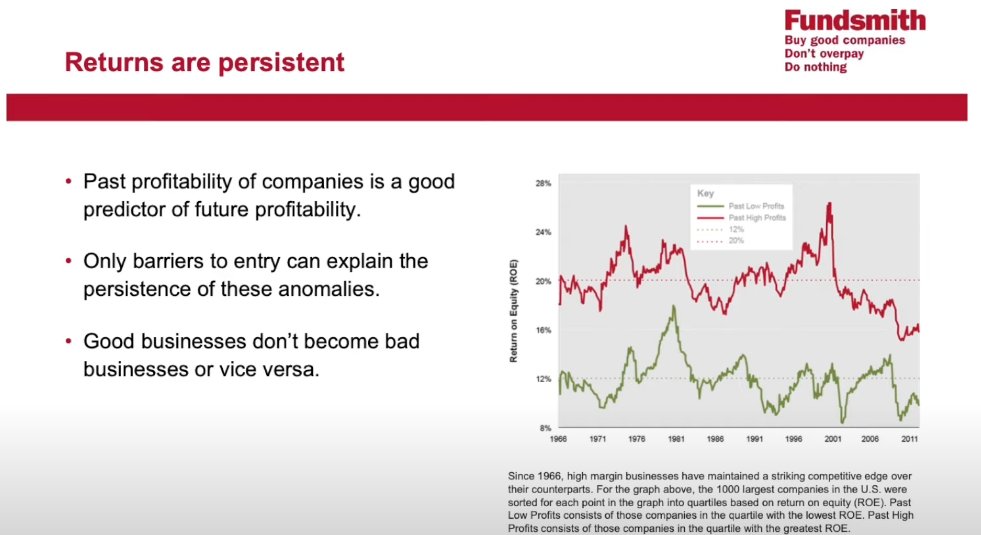

9. Returns are Persistent

Good businesses tend to stay good.

And Fundsmith focuses on good businesses because they are investing for the long-term.

Energy and banks are generally bad businesses.

This "rotation" is temporary and it doesn't make them become good.

Good businesses tend to stay good.

And Fundsmith focuses on good businesses because they are investing for the long-term.

Energy and banks are generally bad businesses.

This "rotation" is temporary and it doesn't make them become good.

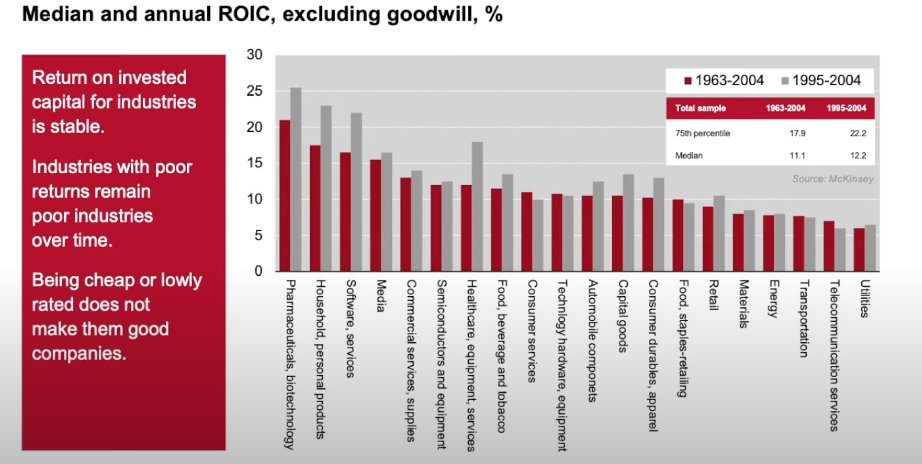

10. ROC is Persistent for Industries

This chart compares the ROC between:

1963-2004 VS 1995-2004

Industry with poor returns remains poor and vice versa.

"Over the long term, it's hard for a stock to earn a much better return than the business which underlies it earns."

This chart compares the ROC between:

1963-2004 VS 1995-2004

Industry with poor returns remains poor and vice versa.

"Over the long term, it's hard for a stock to earn a much better return than the business which underlies it earns."

11. Main Determinant of Investment Outcomes...

Isn't what's happening in the short-term: inflation, interest rates, Ukraine

The most important thing is to in good businesses that can reinvest at high ROC.

And whether they have the fortitude & patience to stay invested.

Isn't what's happening in the short-term: inflation, interest rates, Ukraine

The most important thing is to in good businesses that can reinvest at high ROC.

And whether they have the fortitude & patience to stay invested.

12. On ESG

Big marketing tool, Terry remains cynical.

If sole focus is on ESG, it'll not drive Alpha.

It always goes back to ROC, cash conversion, margins, and reinvestment to build its moat.

Big marketing tool, Terry remains cynical.

If sole focus is on ESG, it'll not drive Alpha.

It always goes back to ROC, cash conversion, margins, and reinvestment to build its moat.

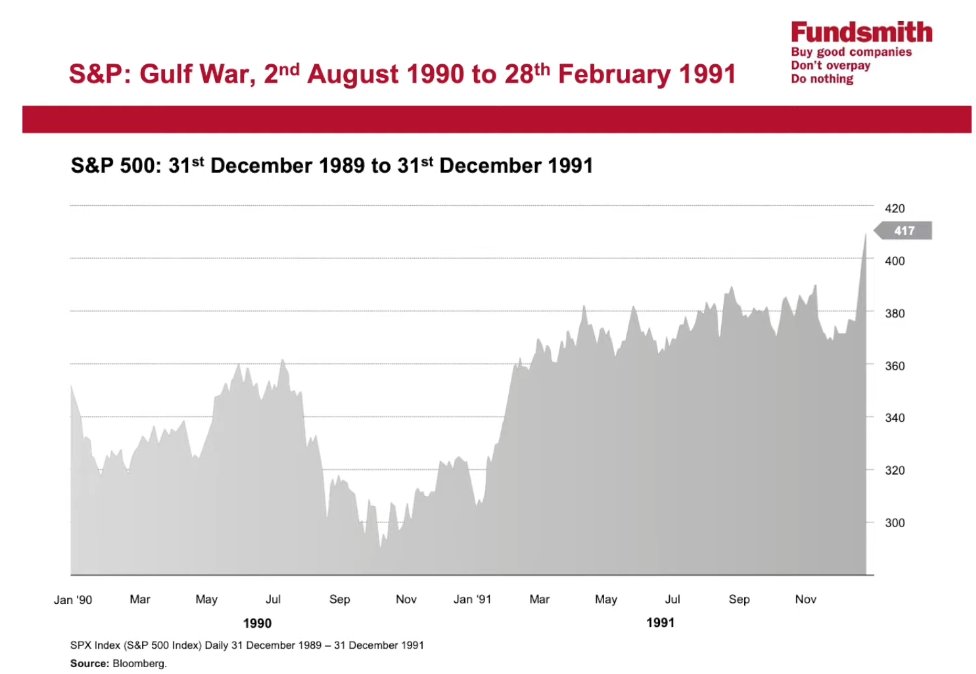

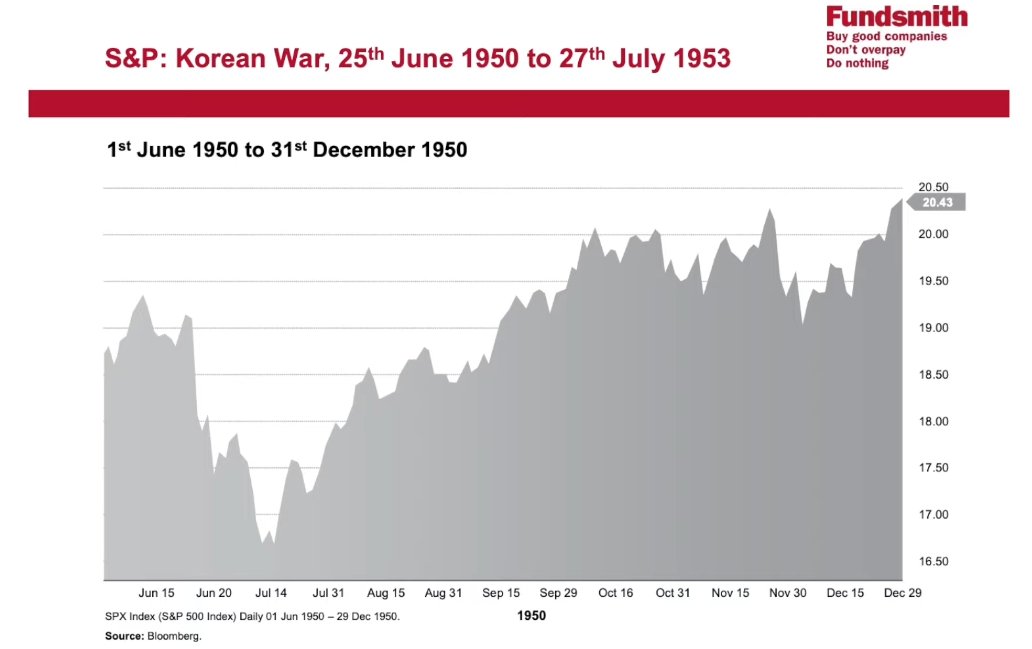

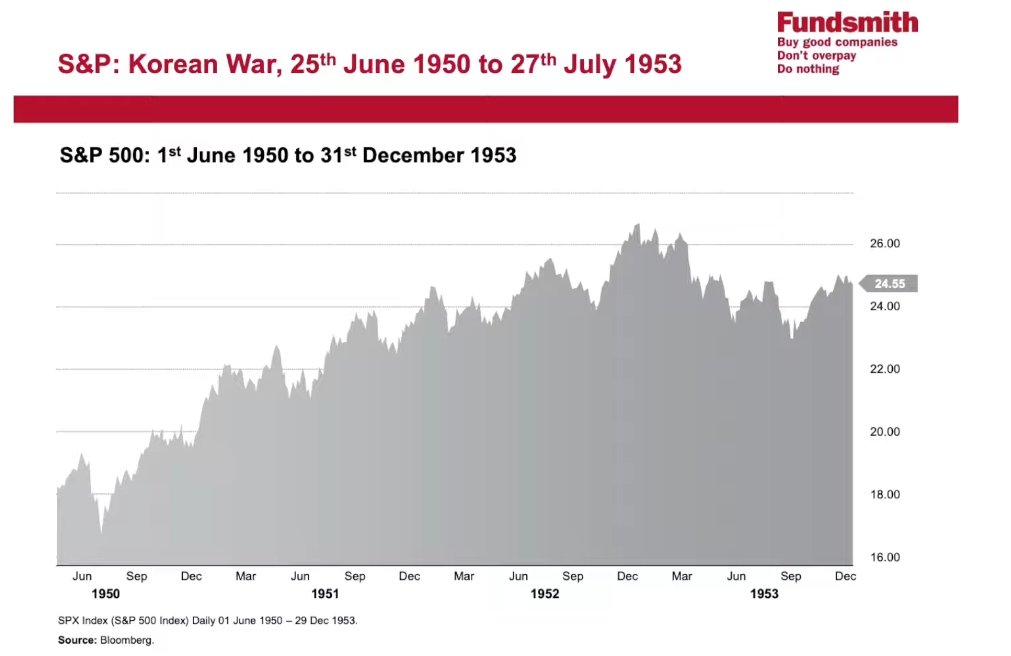

13. The War in Ukraine

If history is any guide:

"Buy on the sound of canons" — Nathan Mayer Rothschild

Most of their companies have no significant exposure to Russia.

Russia is a resource economy, not a consumer goods nor tech economy.

Fundsmith isn't affected much.

If history is any guide:

"Buy on the sound of canons" — Nathan Mayer Rothschild

Most of their companies have no significant exposure to Russia.

Russia is a resource economy, not a consumer goods nor tech economy.

Fundsmith isn't affected much.

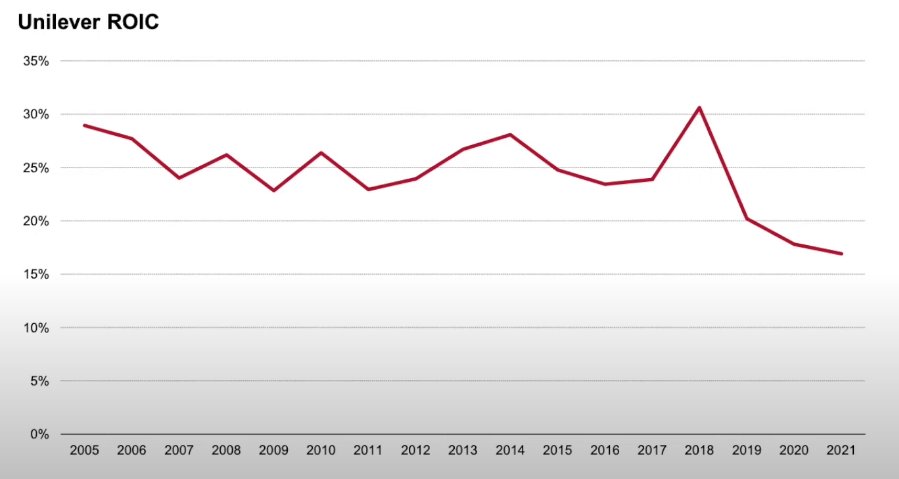

14. Why hasn't he sold Unilever?

Terry has frequently criticized Unilever's management.

But continues to hold them because they're fundamentally a good business.

Holds plenty of great brands.

It's easier to change the management than to change the quality of the business.

Terry has frequently criticized Unilever's management.

But continues to hold them because they're fundamentally a good business.

Holds plenty of great brands.

It's easier to change the management than to change the quality of the business.

15. $FB investment in the metaverse

The company is spending heavily on data centers to prepare for the metaverse.

But it isn't speculative spending.

Tim Cook from $APPL echoed similar sentiments about the metaverse.

Valuing it based on $FB ad business alone, it's very cheap.

The company is spending heavily on data centers to prepare for the metaverse.

But it isn't speculative spending.

Tim Cook from $APPL echoed similar sentiments about the metaverse.

Valuing it based on $FB ad business alone, it's very cheap.

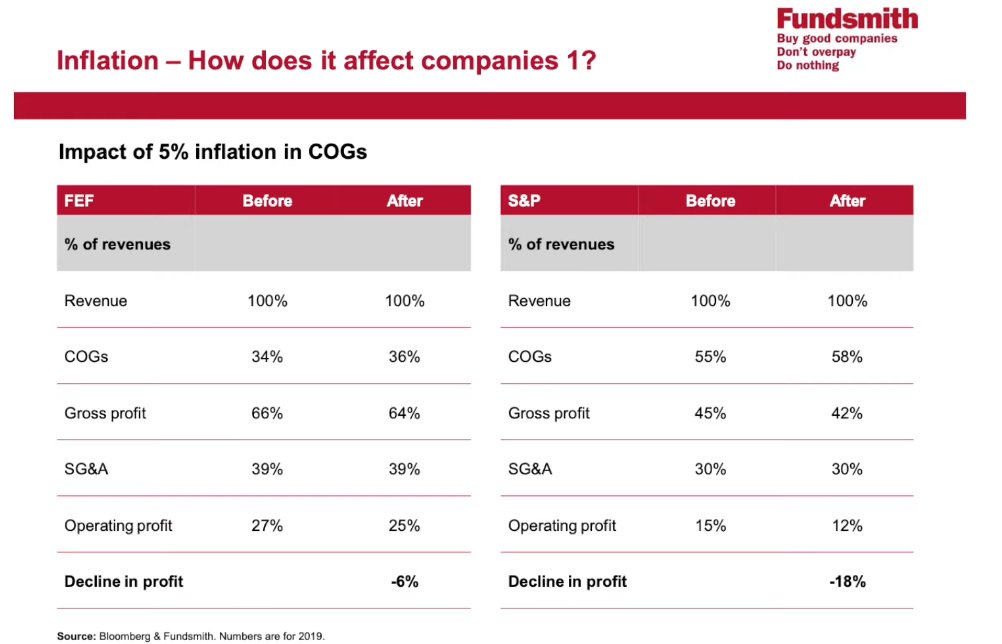

16. On inflation

Not all companies are impacted equally.

The biggest frontline of protection is not having COGS a big % of expenses.

Companies with high GPM will defend themselves better in times of inflation.

Not all companies are impacted equally.

The biggest frontline of protection is not having COGS a big % of expenses.

Companies with high GPM will defend themselves better in times of inflation.

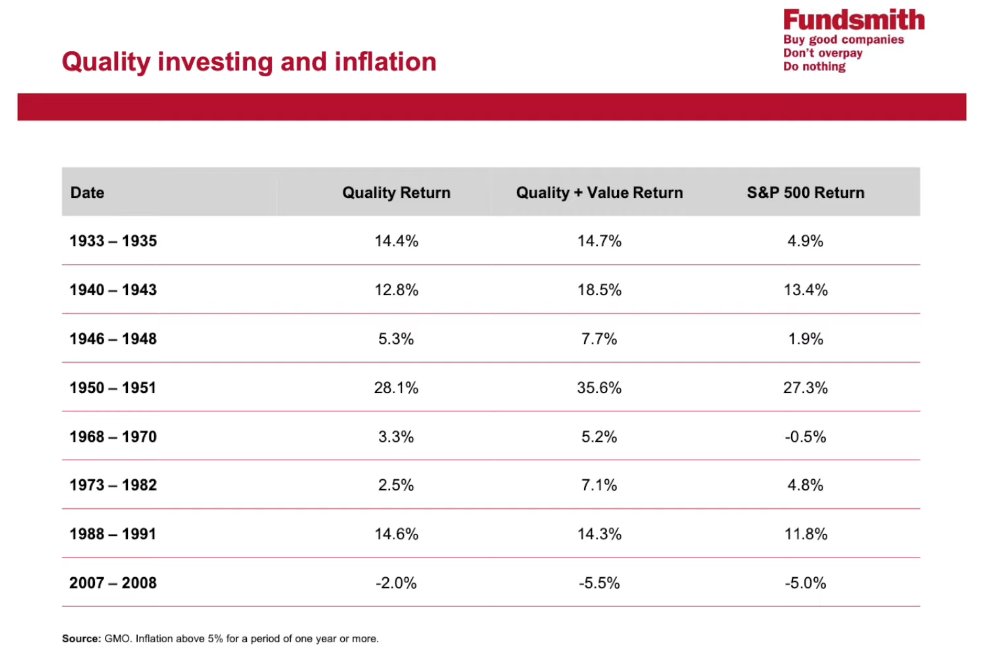

During periods of high inflation (>5%), quality companies will outperform the index.

Historically, it only underperformed during one of the high inflationary period.

Historically, it only underperformed during one of the high inflationary period.

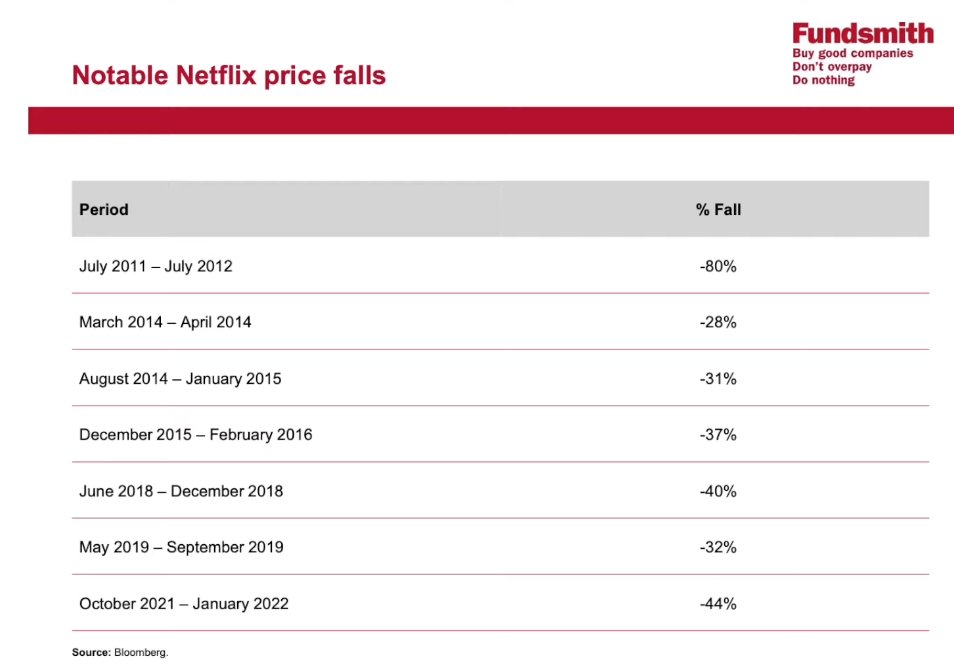

17. On Volatility

If volatility makes you uneasy then the stock market may not be for you.

$NFLX has multiple drawdowns (as shown in the chart).

But if you held it from 2010-2022, it's a return of 5,992%!

In the end, share prices follow fundamentals, not the other way around.

If volatility makes you uneasy then the stock market may not be for you.

$NFLX has multiple drawdowns (as shown in the chart).

But if you held it from 2010-2022, it's a return of 5,992%!

In the end, share prices follow fundamentals, not the other way around.

That's a wrap!

I hope you enjoyed it.

If you like this, follow me here @steadycompound

I write about investment concepts, business breakdowns and growth philosophies.

I hope you enjoyed it.

If you like this, follow me here @steadycompound

I write about investment concepts, business breakdowns and growth philosophies.

If you like tweets like these, you might enjoy my weekly newsletter: Steady Compounding.

I write about business breakdowns, investing concepts and timeless lessons from super investors.

Join here: steadycompounding.com

I write about business breakdowns, investing concepts and timeless lessons from super investors.

Join here: steadycompounding.com

Found this helpful?

Retweet the first tweet to help others find it!

Retweet the first tweet to help others find it!

https://twitter.com/SteadyCompound/status/1506219189849272320

If you like to watch the meeting, check it out here:

If you want more Terry Smith, check out my key takeaways from his book:

Investing for Growth

Investing for Growth

https://twitter.com/SteadyCompound/status/1469791173069975555

• • •

Missing some Tweet in this thread? You can try to

force a refresh