1.OK, after a day of flights and meetings for yours truly, I have thoughts on $CNQ.

2.This Q was sort of underwhelming, not bad but also not the epic blowout like $TOU had, just a solid, expected Q. $CNQ

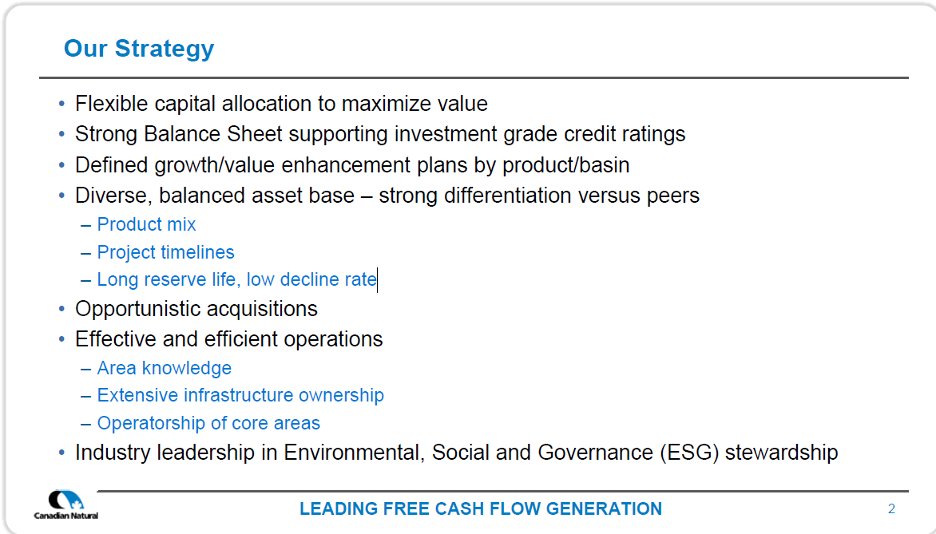

3.On to their deck, loved to see them lightly engaging with the Elliott $SU drama by explaining why they are worth a premium – it is hard to disagree – best in class reserves, a solid asset base across commodities $CNQ #LongLifeLowDecline

4.Then on to some yada yada yada about their capital discipline, which is true – but it also is kind of meaningless in this pricing environment. $CNQ #CREAM

5.It is weird that $CNQ almost seems defensive about it’s value in light of the #RestoreSuncor campaign against $SU, like ya you trade at a premium – thanks for explaining why?

6.Good to see someone talking about #RLI issues at $SU, even if it is their competitor. $CNQ

7.What a bloody flex this is - $CNQ just ticking off $BP $COP $CVX $SHEL $TTE $XOM

8.This is where things get interesting – at least for me, the Acquisition side $CNQ

9. So I am wondering if some of the reaction to the Q was the fact that debt didn’t fall more? I am having some trouble reconciling their acquisition spend with the lack of decline in net debt.

https://twitter.com/SadBillAckman/status/1512421927171751936

11.What would have been #Pike Phase 1 will be developed by pads feeding Jackfish1 CPF and Pike2 will feed Kirby South.

https://twitter.com/SadBillAckman/status/1503824842360975361(My circles worked!) $CNQ

12.I am a bit struggling to reconcile this in my head (first h/t to @_sem_yyc for getting me a copy of the $CNQ $DVN deck), how much of the Pike reserves were already booked as 2P when the deal closed in 2019?

13.I thought this deck included a breakdown of reserves by asset but no such luck, and memory fades. TLDR is that this will enable #KirbyPikeFish™ to run as full as $CNQ wants for a very long time.

14.The $CVE Wembley deal is a classic Bolt On – it does what it says on the tin. $CNQ

15. So this beings up to the fun / chose your own adventure approach to shareholder returns. First we have $CNQ establishing a lower bound for their debt reduction of 8 billion $CNQ, which is approximately their public debt outstanding.

16. We pick up on the call with a question from Greg $RY on what “incremental returns” means??

So we have confirmation that $CNQ is considering variable dividends as part of their shareholder return program.

So we have confirmation that $CNQ is considering variable dividends as part of their shareholder return program.

17.Though they don’t sound super enthused about this and I am left feeling like taking the under on them making changes to their program of higher base dividends and lots of buybacks. $CNQ

18. Which brings us to SBC and Buybacks, Christ 42% of Q1 buybacks went to offsetting dilution from SBC – I get it , the stock is at ATH’s but by the same token it really blunts the impact of your buybacks when nearly half was just issued stock. $CNQ

19. So what to make of all this? $CNQ is a monster when it comes to execution and generating FCF, that they are about to build one of the least levered majors in the world – but it feels like they need to clean up the story around what happens when debt hits 8B.

20. As @johnwhi60696884 points out there is a question of buying back your stock at ATH’s, $TOU seems to understand this better...

@johnwhi60696884 20.a , now $CNQ still has issued a net 43.3mm shares over the last 5 years so I am comfortable with continued buybacks to get the float closet to that number…

21. But there is also a question about if buybacks alone are what the market wants. $CNQ

• • •

Missing some Tweet in this thread? You can try to

force a refresh