1/ Bad Habits and Good Practices (Goyal, Ilmanen, Kabiller)

Bad habits:

* Chasing (selling) multi-year winners (laggards) in stocks, asset classes, strategies

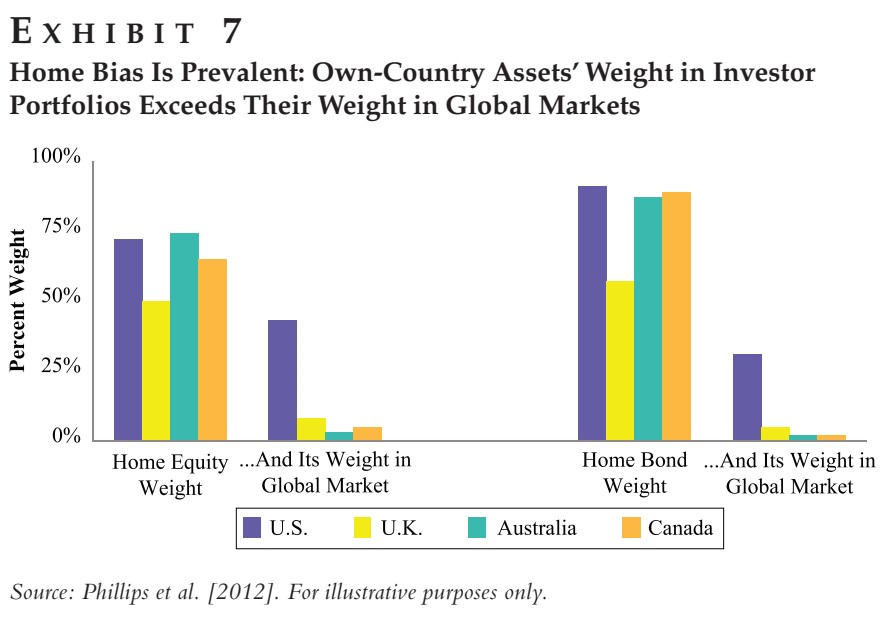

* Home bias; too much equity risk

* "Comfortable" investments (over-priced & under-diversified)

aqr.com/Insights/Resea…

Bad habits:

* Chasing (selling) multi-year winners (laggards) in stocks, asset classes, strategies

* Home bias; too much equity risk

* "Comfortable" investments (over-priced & under-diversified)

aqr.com/Insights/Resea…

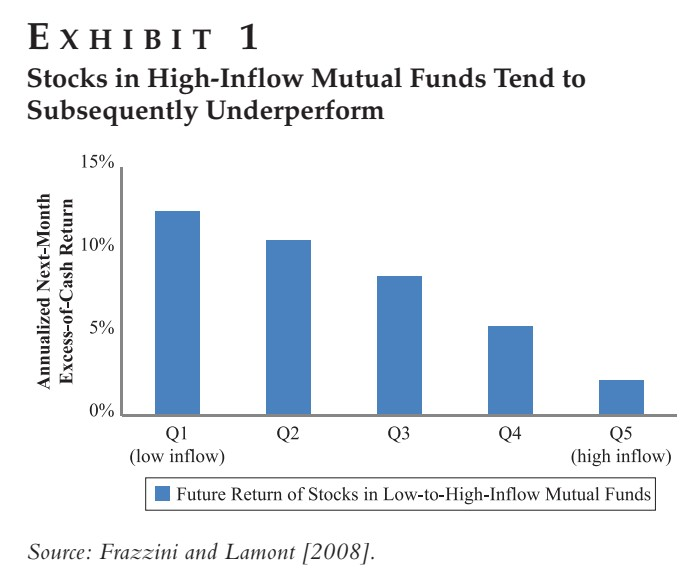

2/ "The main underperformance occurs six to thirty months after mutual fund inflows. This evidence is related to the value effect and retail investors chasing past performance."

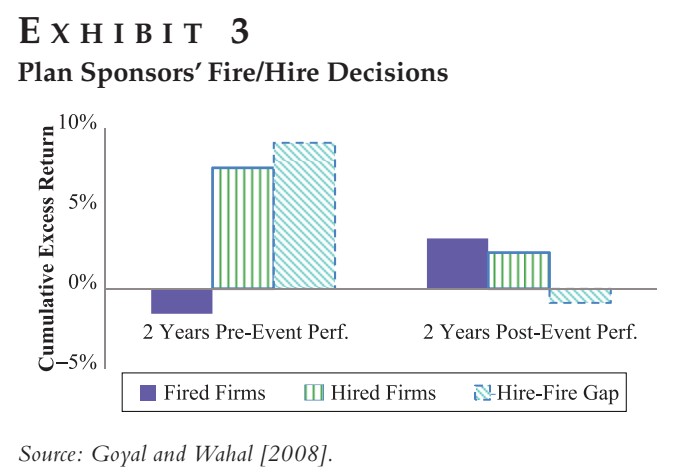

3/ "For institutional plan sponsor allocation activity, products receiving contributions subsequently underperform products experiencing withdrawals.

"The bar chart contrasts past-year flows and next-year returns, but similar patterns hold for the next three to five years."

"The bar chart contrasts past-year flows and next-year returns, but similar patterns hold for the next three to five years."

4/ "For pension plan sponsors from 1996 to 2003 (an admittedly limited sample), replacing managers has been procyclic, but fired managers later tended to mildly underperform their hired replacements. The patterns are similar with one- to three-year windows."

5/ "Pension funds in aggregate have not captured the shift from momentum to reversal tendencies in asset returns but instead keep chasing returns over multi-year horizons.

"This evidence is at the asset-class level; the patterns may be even stronger within the stock market."

"This evidence is at the asset-class level; the patterns may be even stronger within the stock market."

6/ "Humans tend to apply our desire to extrapolate even instances when no pattern exists to be successfully extraplated.

"Procyclic actions are reinforced by various social effects (herding, conventionality, peer risk) and even by certain risk management rules."

"Procyclic actions are reinforced by various social effects (herding, conventionality, peer risk) and even by certain risk management rules."

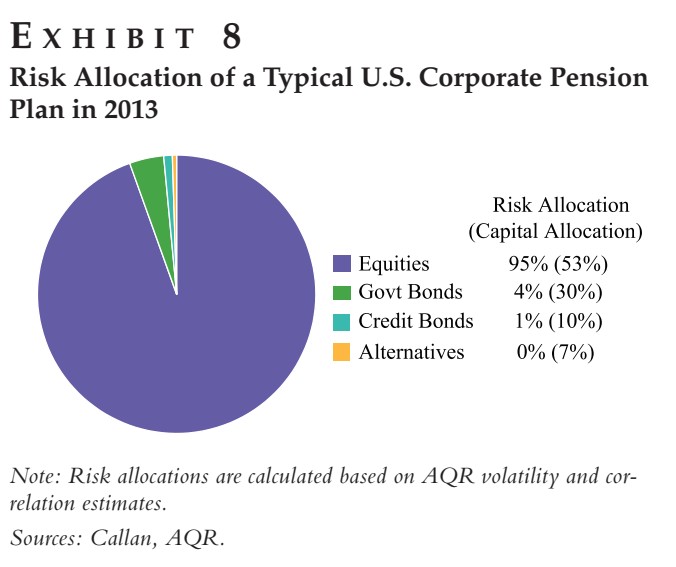

7/ "The risk allocation for a typical U.S. corporate pension plan is similar to that of public pension plans, endowments, and foundations.

"Investors in aggregate cannot avoid equity concentration, but any particular investor can certainly choose to be better diversified."

"Investors in aggregate cannot avoid equity concentration, but any particular investor can certainly choose to be better diversified."

8/ "Investors underutilize comfort-challenging tools (leverage, shorting, derivatives) that could be used to improve diversification. Staying in the comfort zone can imply leaving Sharpe ratio on the table."

This problem is solvable:

This problem is solvable:

https://twitter.com/ReformedTrader/status/1457797335430225922

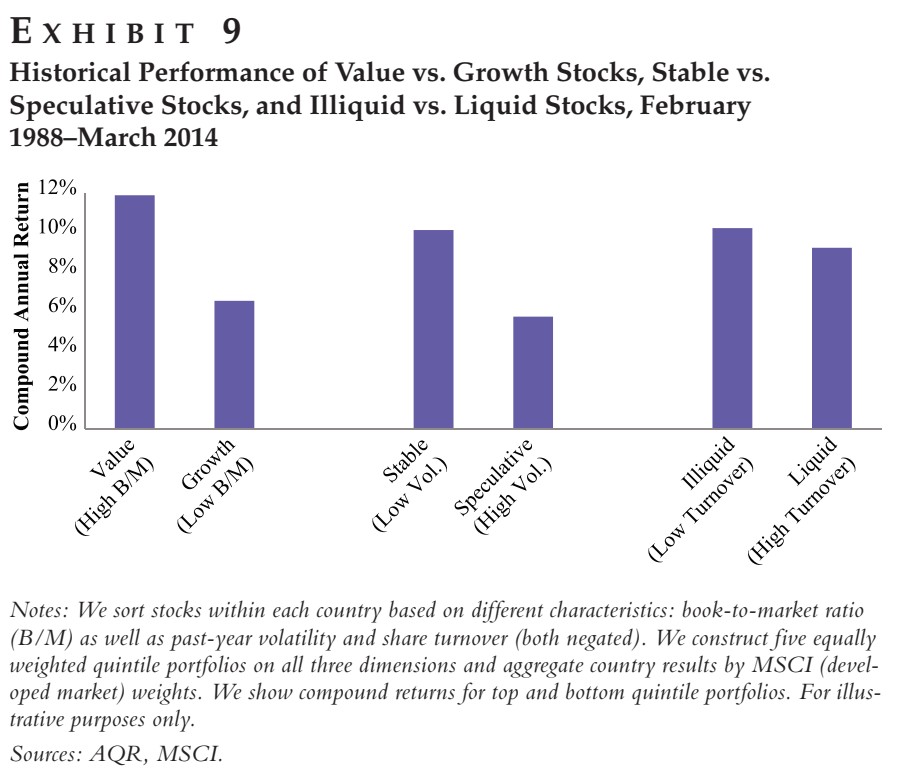

9/ "We believe the main reason for value's outperformance includes investors' excessive multi-year extrapolation of recent growth and the greater ease of holding popular story stocks than persistent losers."

More on the value factor:

More on the value factor:

https://twitter.com/ReformedTrader/status/1117084235318190087

10/ "Habits tend to occur unconsciously and often become institutionalized over time."

"Investors should embrace intelligent risks, including tools (leverage, shorting, and derivatives) that let them fully diversify, though mixing these with illiquid assets can be dangerous."

"Investors should embrace intelligent risks, including tools (leverage, shorting, and derivatives) that let them fully diversify, though mixing these with illiquid assets can be dangerous."

• • •

Missing some Tweet in this thread? You can try to

force a refresh