Quick thread on inflation

1. What the Fed can deal with

2. What the Fed cannot deal with

3. Size of each

Here we go.

🧵/1

1. What the Fed can deal with

2. What the Fed cannot deal with

3. Size of each

Here we go.

🧵/1

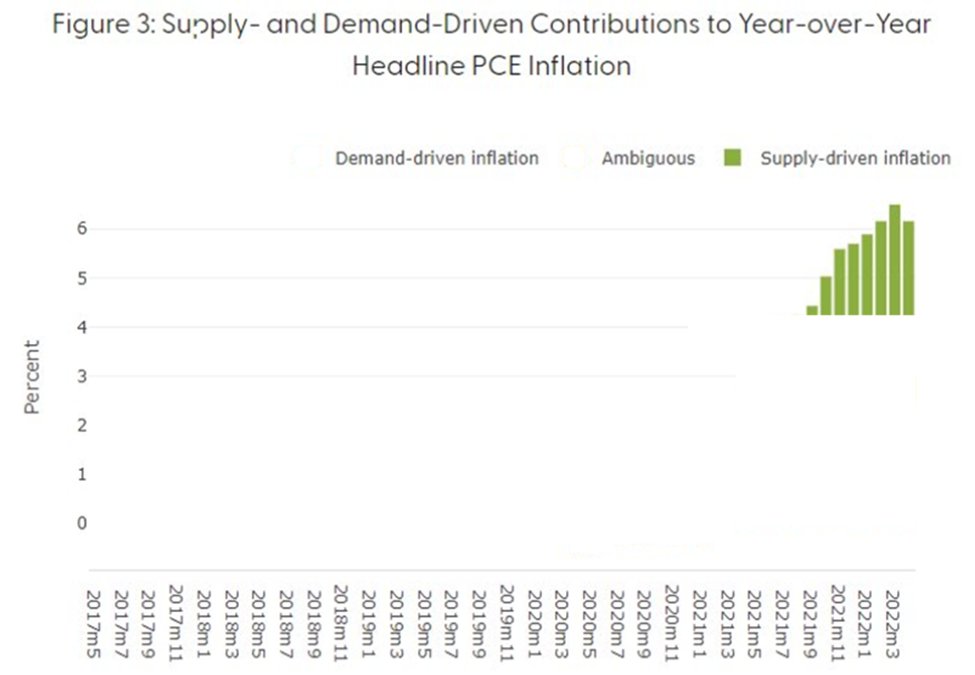

The excess demand side inflation from that chart

/3

/3

The part is 'normal' demand side inflation (outlined in green).

The 'excessive of normal' demand-side inflation (the part above the green)

/4

The 'excessive of normal' demand-side inflation (the part above the green)

/4

Just the 'excessive of normal' demand-side inflation (the part above the green)

/5

/5

Same exercise from the excess inflation from supply side

/6

/6

Comparing the duration and size of excess inflation from demand (blue) and supply (green)

/7

/7

My conclusion:

Excess demand side inflation been more persistent; Excess supply side inflation has been larger.

The Fed can't do much about the excess supply-side inflation which is larger part, but there is still plenty of excess demand-side inflation for the Fed to tame

/8

Excess demand side inflation been more persistent; Excess supply side inflation has been larger.

The Fed can't do much about the excess supply-side inflation which is larger part, but there is still plenty of excess demand-side inflation for the Fed to tame

/8

Onto oil, which the Fed has little control over, but still worth looking at bc it has been the number one contributor to headline CPI.

Start with a simple chart of Oil Prices (a bit dated)

/9

Start with a simple chart of Oil Prices (a bit dated)

/9

Two portions of inflation here.

One before the war, which was substantial, and the part after, which is also substantial.

Focusing on the increases:

/10

One before the war, which was substantial, and the part after, which is also substantial.

Focusing on the increases:

/10

Side-by-side comparison of pre-war inflation and post-war inflation.

/11

/11

And now both together with a conclusion:

* There is a lot of excess demand-side inflation that the Fed can address. So, good, do that.

* Most of the inflation the Fed cannot address (supply-side and energy) and that's bad.

/12

* There is a lot of excess demand-side inflation that the Fed can address. So, good, do that.

* Most of the inflation the Fed cannot address (supply-side and energy) and that's bad.

/12

* I don’t see a reason to be excessively bullish in the immediate-term

* I do see a reason to be quite bullish with a longer-term view

13/13

* I do see a reason to be quite bullish with a longer-term view

13/13

This is how we look at the market and what CML Pro does with stocks.

* Facts A, B, C

* Analysis A, B, C

* Conclusions A, B, C

If done correctly, whether one agrees with analysis and conclusion, value is had just going through the exercise.

Plug

bit.ly/CMLPro

/14

* Facts A, B, C

* Analysis A, B, C

* Conclusions A, B, C

If done correctly, whether one agrees with analysis and conclusion, value is had just going through the exercise.

Plug

bit.ly/CMLPro

/14

• • •

Missing some Tweet in this thread? You can try to

force a refresh