My Favorite #Lithium Stocks 🔋 🚗 With +10x Potential 🚀 💥

Lithium South Development Corp (TSX.V: $LIS, OTC: $LISMF) is one of my favorites. In this thread I'll tell you why!

*Thread*

Lithium South Development Corp (TSX.V: $LIS, OTC: $LISMF) is one of my favorites. In this thread I'll tell you why!

*Thread*

Location 📍 🗺️

$LIS Hombre Muerto North (HMN) project is located in the famous Hombre Muerto salar in the #Lithium Triangle. About 40% of the world's lithium is produced in Atacama and Hombre Muerto. Hombre Muerto salar has a +25 year history of large scale #lithium production

$LIS Hombre Muerto North (HMN) project is located in the famous Hombre Muerto salar in the #Lithium Triangle. About 40% of the world's lithium is produced in Atacama and Hombre Muerto. Hombre Muerto salar has a +25 year history of large scale #lithium production

Resource Quality ⛏️ ✅

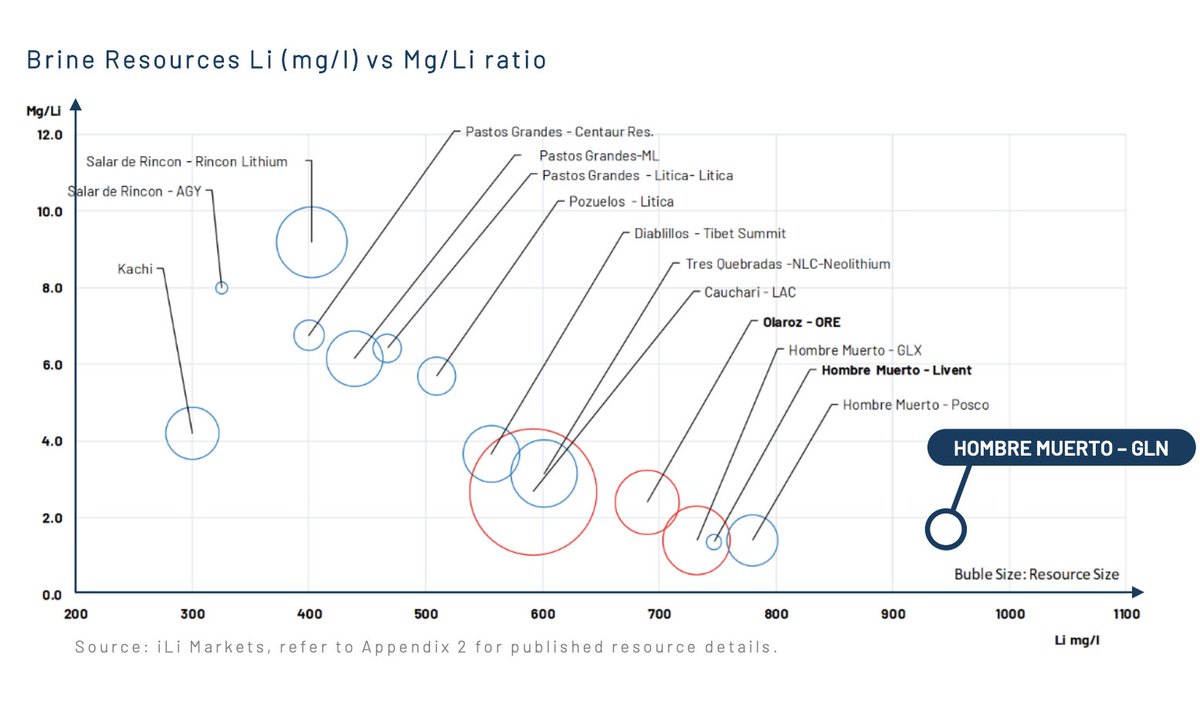

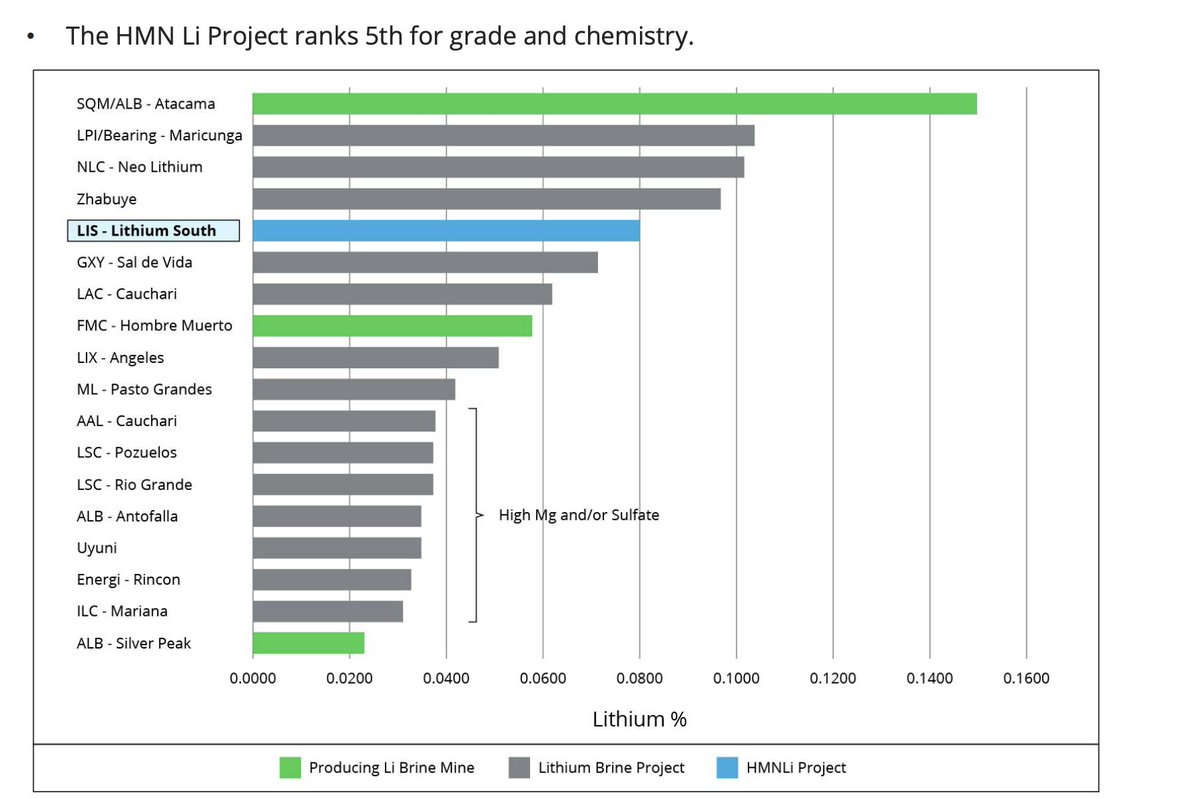

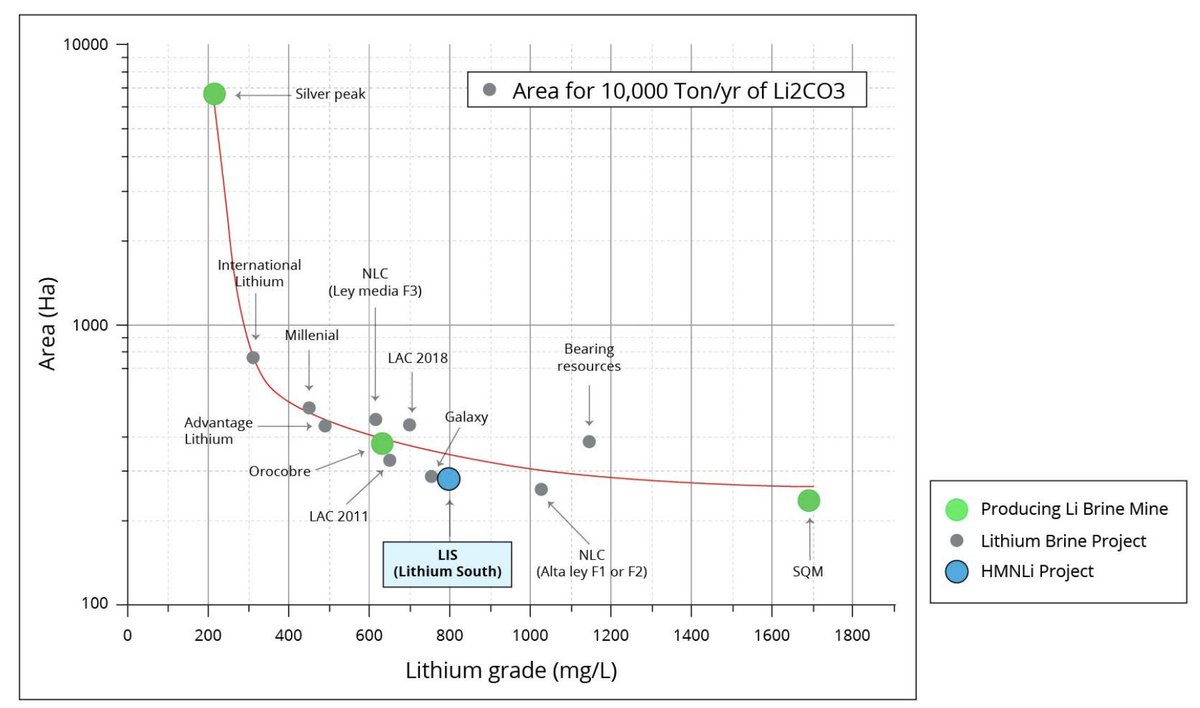

$LIS brine shares the world-class characteristics of other brines in Hombre Muerto. Low impurities coupled with a high #lithium grade makes it one of the purest brines in the world, suitable for low cost production of battery grade lithium carbonate

$LIS brine shares the world-class characteristics of other brines in Hombre Muerto. Low impurities coupled with a high #lithium grade makes it one of the purest brines in the world, suitable for low cost production of battery grade lithium carbonate

Resource Size ⛏️ ⛰️

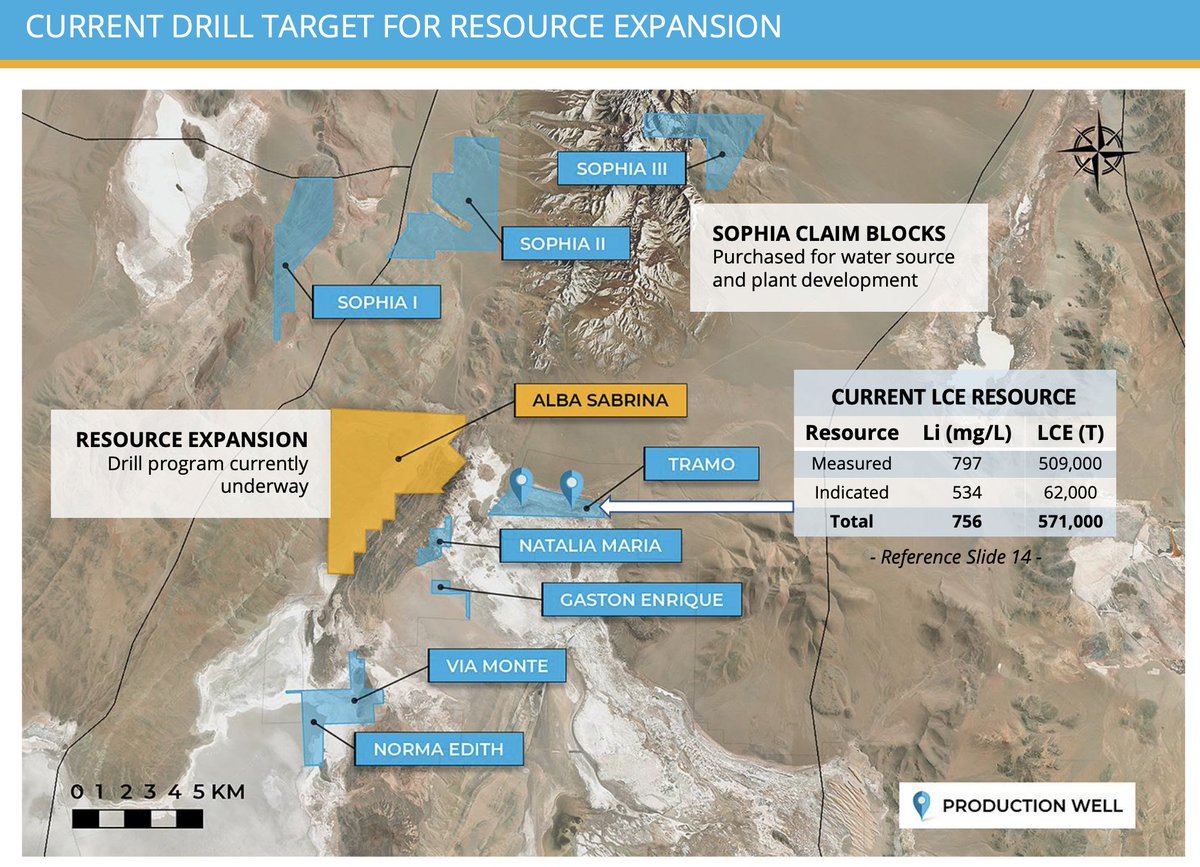

$LIS PEA from 2019 presented a 571,000 tonne LCE resource (Measured and Indicated). The resource estimate and historic drilling focused only on 1 of the 6 claim blocks the company held at that time. A new expansion drill program is currently underway

$LIS PEA from 2019 presented a 571,000 tonne LCE resource (Measured and Indicated). The resource estimate and historic drilling focused only on 1 of the 6 claim blocks the company held at that time. A new expansion drill program is currently underway

Ongoing Expansion Drilling 📶

The ongoing expansion drill program is focused on Alba Sabrina, $LIS largest claim block, aiming to expand the resource to +2Mt LCE

$LIS is taking a fast-tracked approach towards a full feasibility study where the updated resource will be included

The ongoing expansion drill program is focused on Alba Sabrina, $LIS largest claim block, aiming to expand the resource to +2Mt LCE

$LIS is taking a fast-tracked approach towards a full feasibility study where the updated resource will be included

Technology 💡

$LIS in partnership with Eon Minerals is evaluating which technology can optimize the use of the resource. Work is being conducted at the Eon Laboratory in Argentina. Conventional and proven evap. tech is being evaluated in conjunction with #lithium DLE Technology

$LIS in partnership with Eon Minerals is evaluating which technology can optimize the use of the resource. Work is being conducted at the Eon Laboratory in Argentina. Conventional and proven evap. tech is being evaluated in conjunction with #lithium DLE Technology

Impressive team 👷 👷♂️ 💥

https://twitter.com/avanzalg/status/1459916244119924750?s=20&t=JxlhP9TDosybSeLUlq2Vpg

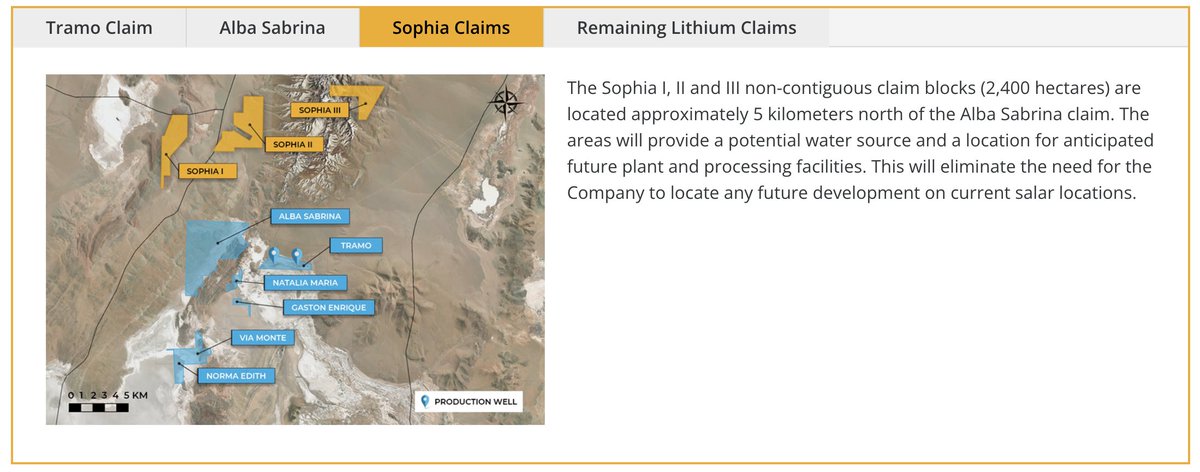

Water source 💧🚰

$LIS recently acquired three new claim blocks aimed to provide the project with a water source as well as a location for future processing facilities

$LIS recently acquired three new claim blocks aimed to provide the project with a water source as well as a location for future processing facilities

Salar Activity

The activity around the Hombre Muerto Salar has increased significantly with large commitments from majors like Posco, Livent and Allkem

$LIS neighbor Posco recently announced it will invest $4bn into its Hombre Muerto salar project

nsenergybusiness.com/news/posco-4bn…

The activity around the Hombre Muerto Salar has increased significantly with large commitments from majors like Posco, Livent and Allkem

$LIS neighbor Posco recently announced it will invest $4bn into its Hombre Muerto salar project

nsenergybusiness.com/news/posco-4bn…

M&A Activity 💰

The area has seen multiple buyouts the recent years, showcasing the demand for high-quality brine resources.

*Update 2022 LSC: USD 962 M

The area has seen multiple buyouts the recent years, showcasing the demand for high-quality brine resources.

*Update 2022 LSC: USD 962 M

Production Tonnage ⛏️

With a +2Mt LCE resource, $LIS hopes to be able to increase the production tonnage in the upcoming feasibility study to 20,000 tonnes LCE per year

An increase to 20ktpa would make HMN the same size as LSC's LitheA project recently sold for US $962 million

With a +2Mt LCE resource, $LIS hopes to be able to increase the production tonnage in the upcoming feasibility study to 20,000 tonnes LCE per year

An increase to 20ktpa would make HMN the same size as LSC's LitheA project recently sold for US $962 million

Summary

✅ Advanced project in a top-tier salar w/ very pure brine

✅ High activity in the area (M&A & investments)

✅ Experienced team

✅ Evaluating both conventional evap & DLE

✅ Ongoing expansion → higher future production tonnage

✅ Low valuation C$41M mcap ~C$11M cash

✅ Advanced project in a top-tier salar w/ very pure brine

✅ High activity in the area (M&A & investments)

✅ Experienced team

✅ Evaluating both conventional evap & DLE

✅ Ongoing expansion → higher future production tonnage

✅ Low valuation C$41M mcap ~C$11M cash

* Cash figure is from end of March. Burnrate: ~$0.5 million / month (not including share-based payments which is another $0.5 million/month). So an updated figure would be ~C$9.5M.

• • •

Missing some Tweet in this thread? You can try to

force a refresh