#Diamines & Chemicals

Market Cap : 414 Cr

How I Identified ?

1. Diamines and chemicals is into manufacturing of #piperzaine and #ethylenediamines

They have > 40% market of piperazine which goes into ciprofloxacin (API)

#aartiindustries & #neulandlabs manufacture ciprofloxacin

Market Cap : 414 Cr

How I Identified ?

1. Diamines and chemicals is into manufacturing of #piperzaine and #ethylenediamines

They have > 40% market of piperazine which goes into ciprofloxacin (API)

#aartiindustries & #neulandlabs manufacture ciprofloxacin

2. R&D Expenses increasing year on year

3. Investing 14.5 Cr for Pilot plant for newer downstream Products

4. Details of new products

5. Price trend of ethylenediamines

6. Debt free company with cash of 40 cr and investments in stocks of 12 cr

7. Cost of new capex

8. Potential of new plant

9. New Land acquisition at Dahej

10. Excellent Cash flow generation

11. ROCE & Reduction in Inventory Days

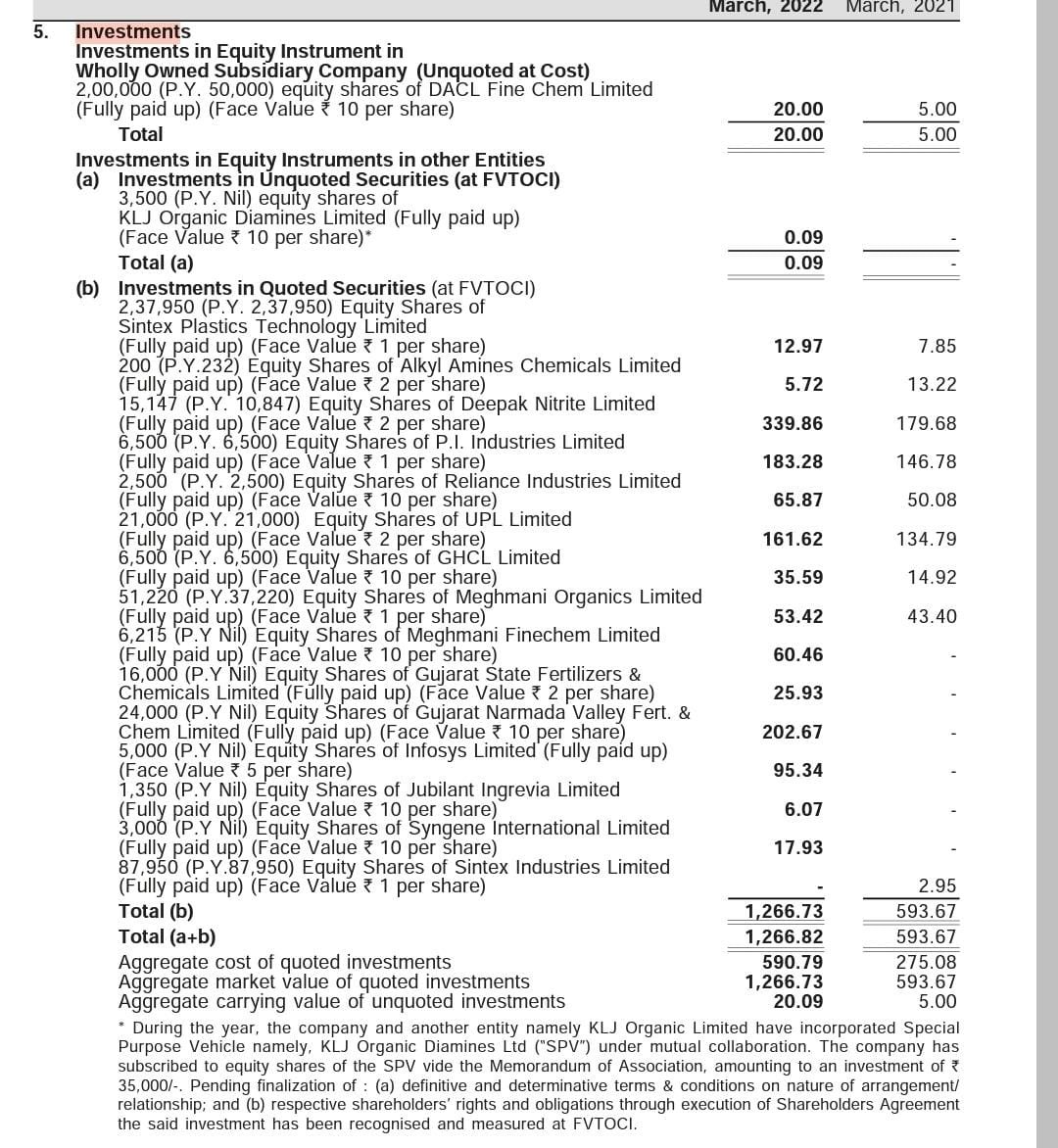

12. JV with KLJ Organics

Soon I will be starting Micro cap focused Model Portfolio (<1000 cr Market cap Opportunities ) which are unidentified and less discussed on social media

Register : forms.gle/W1yM4eURZAcYGT…

Register : forms.gle/W1yM4eURZAcYGT…

• • •

Missing some Tweet in this thread? You can try to

force a refresh