SCALING A MULTI-MANAGER TEAM

I was going through some of my materials today in creation of Academy modules and I found a deck that I put together in summer '20 (post my 2 pod PM jobs and post quant-fund consulting gig) when I was interviewing with a large multi-manager as a PM.

I was going through some of my materials today in creation of Academy modules and I found a deck that I put together in summer '20 (post my 2 pod PM jobs and post quant-fund consulting gig) when I was interviewing with a large multi-manager as a PM.

Ultimately I was bounced by that fund after 1 round, so I feel comfortable sharing some of the content that I included in that deck, in case it is helpful to any multi-manager teams that are in scale mode.

So here we go...the team that wasn't...TEAM CAUGHRAN: SCALE PLAN.

So here we go...the team that wasn't...TEAM CAUGHRAN: SCALE PLAN.

TEAM

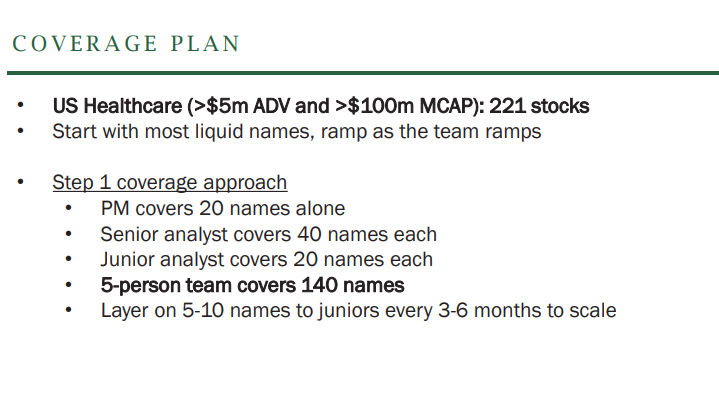

At this point, in healthcare there were 221 stocks in the US that traded over $5m ADV and over $100m MCAP.

At a multi-manager, my investment process generally capped out at ~40 stocks, so I proposed a team of 5 (including myself) to start.

At this point, in healthcare there were 221 stocks in the US that traded over $5m ADV and over $100m MCAP.

At a multi-manager, my investment process generally capped out at ~40 stocks, so I proposed a team of 5 (including myself) to start.

TEAM

I would be looking for an experienced Biopharma analyst on one side, and an experienced MedTools analyst on the other, with demonstrated subsector knowledge and ability to cover 40 names Day 1 and drive "idea velocity".

With the complexity of risk model management, I felt

I would be looking for an experienced Biopharma analyst on one side, and an experienced MedTools analyst on the other, with demonstrated subsector knowledge and ability to cover 40 names Day 1 and drive "idea velocity".

With the complexity of risk model management, I felt

like 3 idea generators (myself included) is about minimum viable team to manage a $1bn+ portfolio where 75%+ of the risk is from idiosyncratic factors.

Below those senior analysts, I would have been looking for young "best mental athlete" junior analysts to plug into the

Below those senior analysts, I would have been looking for young "best mental athlete" junior analysts to plug into the

Senior Analyst process, and I was willing to train these juniors (young, cheaper, hungry).

As the team scaled, my plan was to promote the 2 senior analysts to Associate or Junior PM, each with a carve-out, and promote the best junior analyst to senior. This chart shows one of

As the team scaled, my plan was to promote the 2 senior analysts to Associate or Junior PM, each with a carve-out, and promote the best junior analyst to senior. This chart shows one of

juniors gone, but that wasn't intentional. With positive P&L, the plan would have been to take the team from ~5 up to 6-8, with three PMs on the team taking risk.

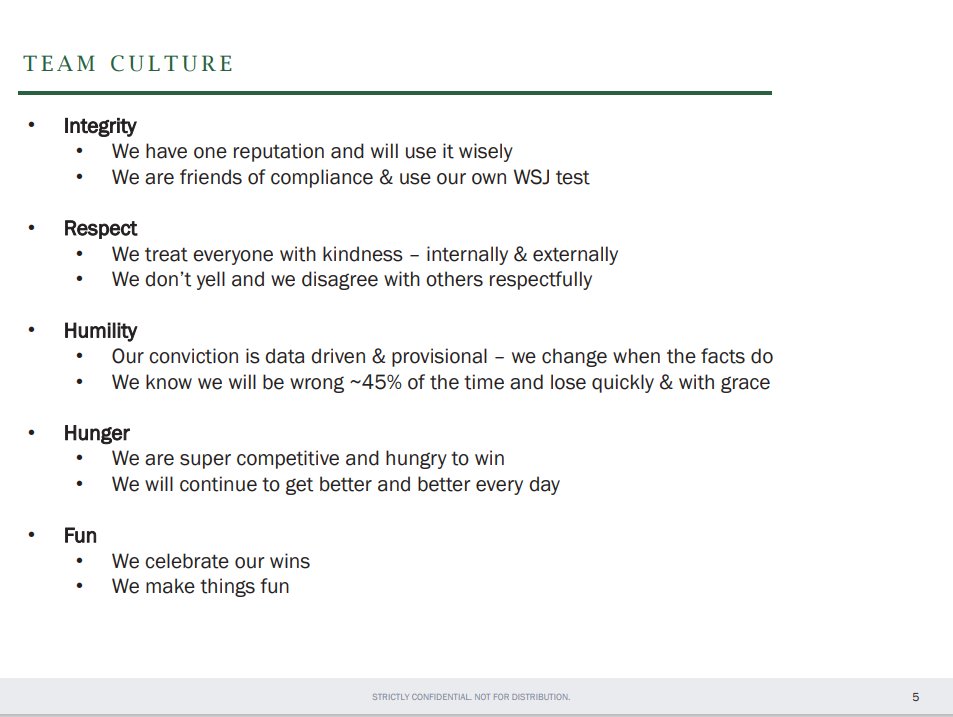

This is the team culture that I was dedicated to establishing.

This is the team culture that I was dedicated to establishing.

COVERAGE

I have found (as have most pod PMs) that a coverage model is the best approach at market neutral, factor-constrained models.

The idea velocity necessary to manage risk well & generate consistent P&L makes it really difficult to be a generalist, taking 6 weeks to go

I have found (as have most pod PMs) that a coverage model is the best approach at market neutral, factor-constrained models.

The idea velocity necessary to manage risk well & generate consistent P&L makes it really difficult to be a generalist, taking 6 weeks to go

from start to finish on a name. Better to have dedicated killers covering 40 stocks who can pounce at any sign of mispricing. Each of these analysts has a model and a dedicated coverage plan for each name.

As a PM, that means at any time we are prepared to trade all 140 stocks

As a PM, that means at any time we are prepared to trade all 140 stocks

under coverage.

I planned to cover 20 names (vs. a senior covering 40) to lead from the front on coverage process and stay in the flow of the "central nervous system" stocks in healthcare. Using the rest of my time to manage the portfolio.

I planned to cover 20 names (vs. a senior covering 40) to lead from the front on coverage process and stay in the flow of the "central nervous system" stocks in healthcare. Using the rest of my time to manage the portfolio.

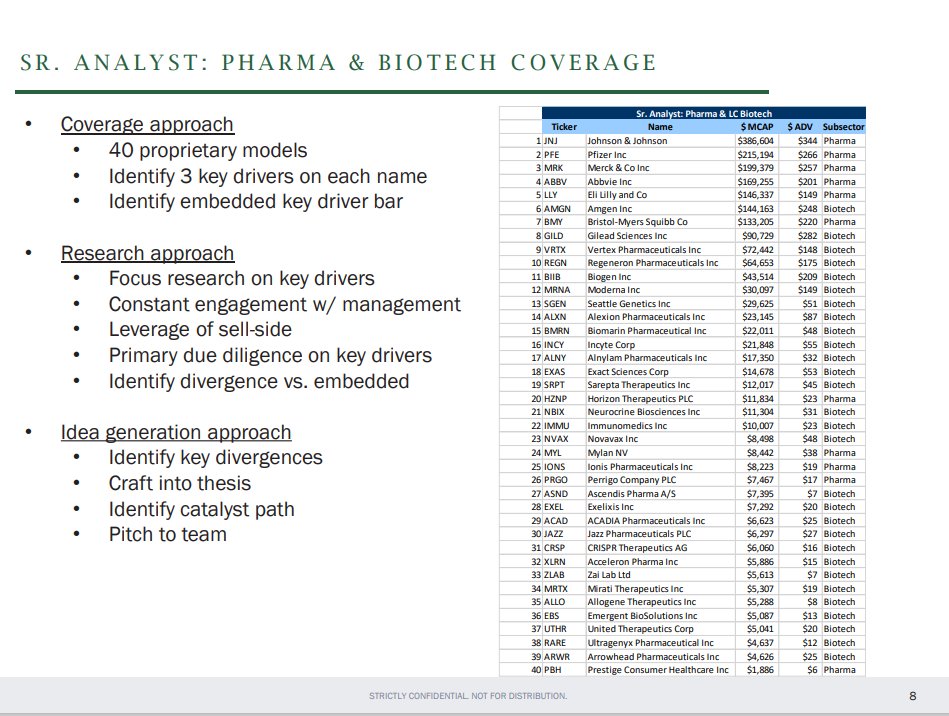

Whereas a senior analyst would be 100% dedicated to covering 40 stocks. Identifying the 3 key drivers and price-embedded expectations then focusing research on driving differentiation and, consequently, tradable ideas.

Junior analysts would start as Senior Analyst support (modeling, research assistance) then grow into Coverage as they were ready, generally with smaller names or less covered sectors (Senior Analysts taking the more liquid and more scalable names)

IDEA VELOCITY

The goal was to bring one new idea per week from coverage. Sound like a lot? It is. But if you are closely covering 40 names, after a bit of time it becomes a natural process.

An example might be: "SYK talked down the Q at Morgan Stanley last week...

The goal was to bring one new idea per week from coverage. Sound like a lot? It is. But if you are closely covering 40 names, after a bit of time it becomes a natural process.

An example might be: "SYK talked down the Q at Morgan Stanley last week...

...but it's underperformed BSX by 9% over the last 2 weeks so it's probably overshot and the talk-down was non-operating". A juicy mean reversion pair like that could go into the book the next morning.

A chunkier, naked, alpha long we might be more considerate about in

A chunkier, naked, alpha long we might be more considerate about in

finishing full due diligence before it goes into the book.

RESEARCH CADENCE

A reasonable part of the PM job is just keeping the team on track. I tried to keep a master calendar to sharpen focus.

For example, we tried to take 3 weeks in December to focus on our big bets for

RESEARCH CADENCE

A reasonable part of the PM job is just keeping the team on track. I tried to keep a master calendar to sharpen focus.

For example, we tried to take 3 weeks in December to focus on our big bets for

the year ahead and for pre-JPM trades. But we had to be responsive to the calendar. Into October, we would work to identify pre-Q3 earnings trades (where hockey stick guidance goes to die).

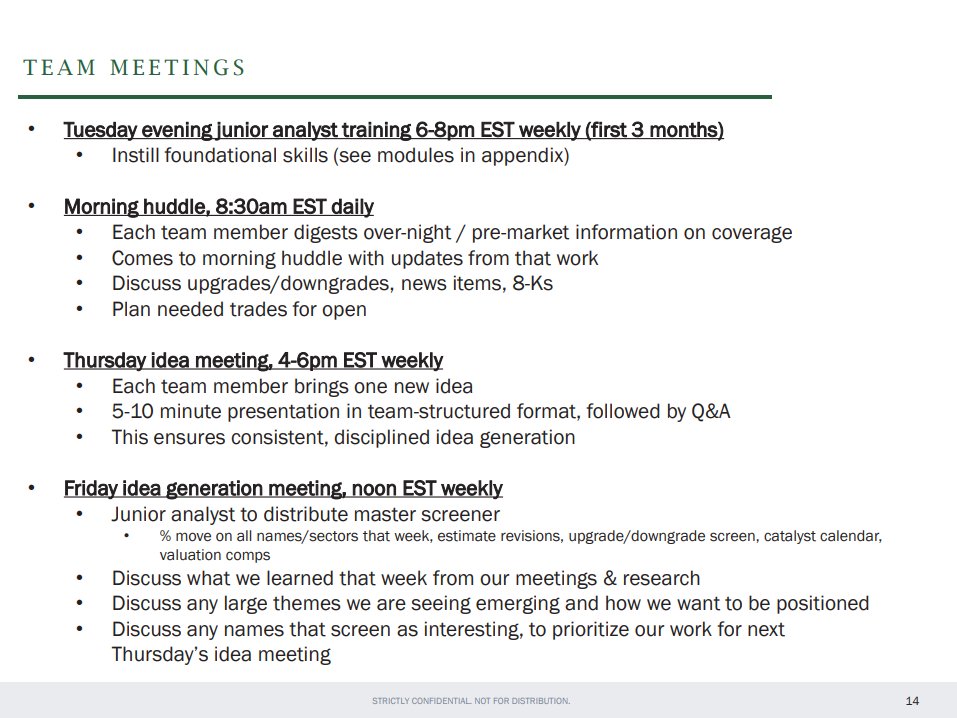

TEAM MEETINGS

Communication is huge, and I've learned (the hard way) that more is better

TEAM MEETINGS

Communication is huge, and I've learned (the hard way) that more is better

In pod land, I've done 8:30am morning huddle, a longer post-close Thursday idea meeting (with a team dinner or drinks often following), then a Friday idea generation meeting for week ahead trades (usually entered before Friday close).

PORTFOLIO CONSTRUCTION

I feel like this is it's own lengthy tweet thread, though I'll show you here my approach to portfolio construction & risk management.

In summary, my approach is to first fill in portfolio with highest conviction alpha trades, then highest conviction pairs

I feel like this is it's own lengthy tweet thread, though I'll show you here my approach to portfolio construction & risk management.

In summary, my approach is to first fill in portfolio with highest conviction alpha trades, then highest conviction pairs

then focus on the fillers and tightening of factor exposures.

In a VaR model, orthogonal P&L is critical as P&L is a simple sum but risk is the sum of squares. Massively simplified, four uncorrelated 1-Sharpe P&L streams can add up to a 2-Sharpe book. And a 2-sharp is GOOD.

In a VaR model, orthogonal P&L is critical as P&L is a simple sum but risk is the sum of squares. Massively simplified, four uncorrelated 1-Sharpe P&L streams can add up to a 2-Sharpe book. And a 2-sharp is GOOD.

RISK MANAGEMENT

Again, this slide is probably it's own tweet thread. But I've learned the hard way, "when you're in a hole, stop digging". Pod P&L management is very much, in my experience, about minimizing losses during rough periods so the book can stay scaled and produce

Again, this slide is probably it's own tweet thread. But I've learned the hard way, "when you're in a hole, stop digging". Pod P&L management is very much, in my experience, about minimizing losses during rough periods so the book can stay scaled and produce

P&L during better periods. Finding the balance of defense vs. offense, I believe, is one of the hardest things for a pod PM.

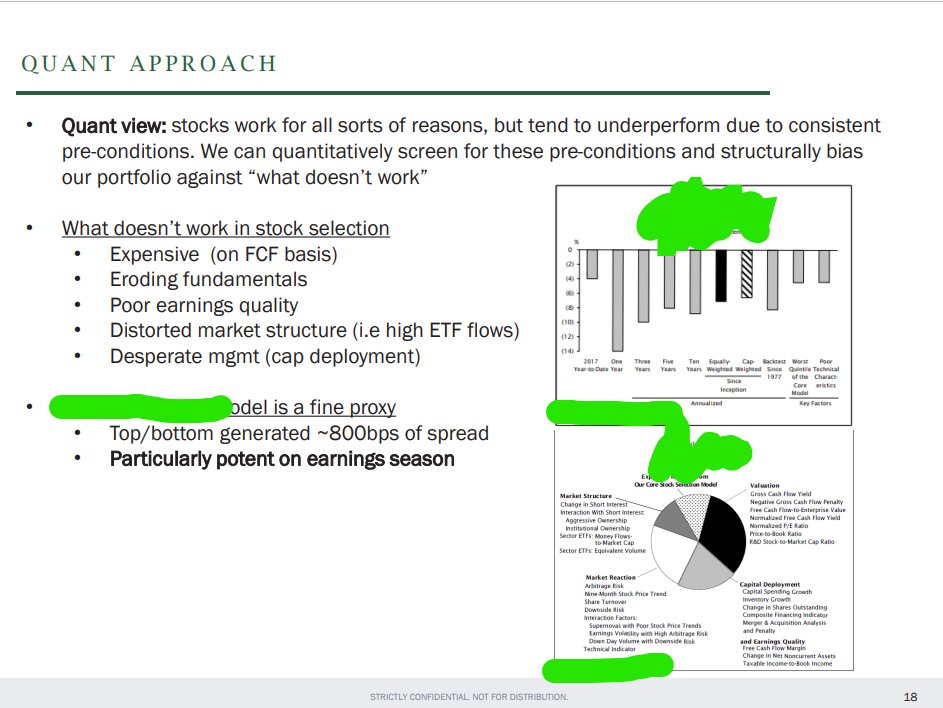

QUANT OVERLAY

I would overlay my book with a quant fundamental model, which was really effective for me over my career (we will be discussing this

QUANT OVERLAY

I would overlay my book with a quant fundamental model, which was really effective for me over my career (we will be discussing this

approach at Academy for those interested)

EDGE

And, of course, hiring managers & LPs love to ask PMs about their "edge". Which is kind of funny, since NO PMs EVER sit and talk to each other about their "edge". We all know this is a very hard, highly competitive business with

EDGE

And, of course, hiring managers & LPs love to ask PMs about their "edge". Which is kind of funny, since NO PMs EVER sit and talk to each other about their "edge". We all know this is a very hard, highly competitive business with

no short-cuts. But, hey, i was trying to get hired!! I had to come up with something. This was our 3-pronged edge.

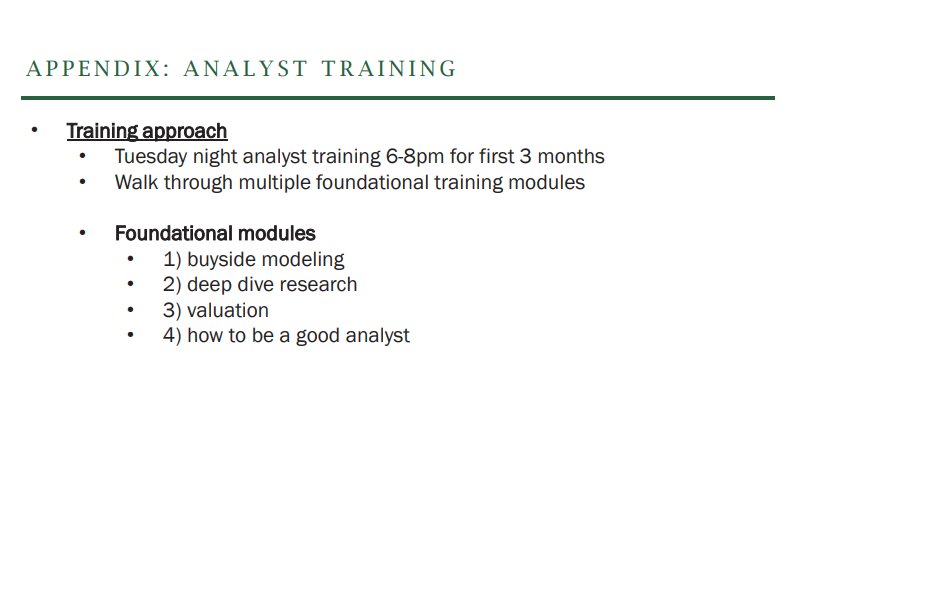

TRAINING

And, OF COURSE, we had to have an analyst training approach. Many of the Fundamental Edge training modules were things I WAS TAUGHT in '08, and have been

TRAINING

And, OF COURSE, we had to have an analyst training approach. Many of the Fundamental Edge training modules were things I WAS TAUGHT in '08, and have been

refined and honed over my various stops on the buy-side over 13 years. Effectively, Academy isn't that different than the training content I gave to my junior analysts back in 2018 (though much better as it has grown & been refined a lot, and includes some amazing guest speakers)

So there we go. Team Caughran. It didn't come to fruition. And I'm FAR from the best pod PM to ever live (evidence: I didn't get the job).

But I hope there are some frameworks in here that can help you if you are at a pod team scaling right now, or in the future!!!

But I hope there are some frameworks in here that can help you if you are at a pod team scaling right now, or in the future!!!

• • •

Missing some Tweet in this thread? You can try to

force a refresh