Michael Mauboussin's 2014 paper "What Does a P/E Multiple Mean" is a great guide to understanding the link between valuation, multiples and business economics (ROIC).

Here are some of my notes from reading it:

Here are some of my notes from reading it:

Multiples are a shorthand for valuation, not the valuation itself. Valuation should be driven by earnings and CFs

The value of a firm can be thought of in two parts:

- steady state value where NOPAT is held constant into perpetuity

- future value creation (growth opportunities)

The value of a firm can be thought of in two parts:

- steady state value where NOPAT is held constant into perpetuity

- future value creation (growth opportunities)

The steady state component simply assumes that there's a core base of a business, the NOPAT of which can be maintained forever, and ROIC=cost of equity, so the steady-state PE multiple can be expressed as 1/CoE. eg. if the CoE is 8%, then the steady state PE mult should be 12.5x

Of course as rates and risk premiums move around, the CoE and thus the steady state PE multiple can change over time, rising during bull markets and low rates and falling during bear markets and rising rates

The second part of the value, the future growth, as per the formula depends on

1) the spread between ROIIC and WACC

2) the size of the investment

3) the duration of the positive spread

Investments that don't exceed the WACC are not value accretive and don't drive up the P/E

1) the spread between ROIIC and WACC

2) the size of the investment

3) the duration of the positive spread

Investments that don't exceed the WACC are not value accretive and don't drive up the P/E

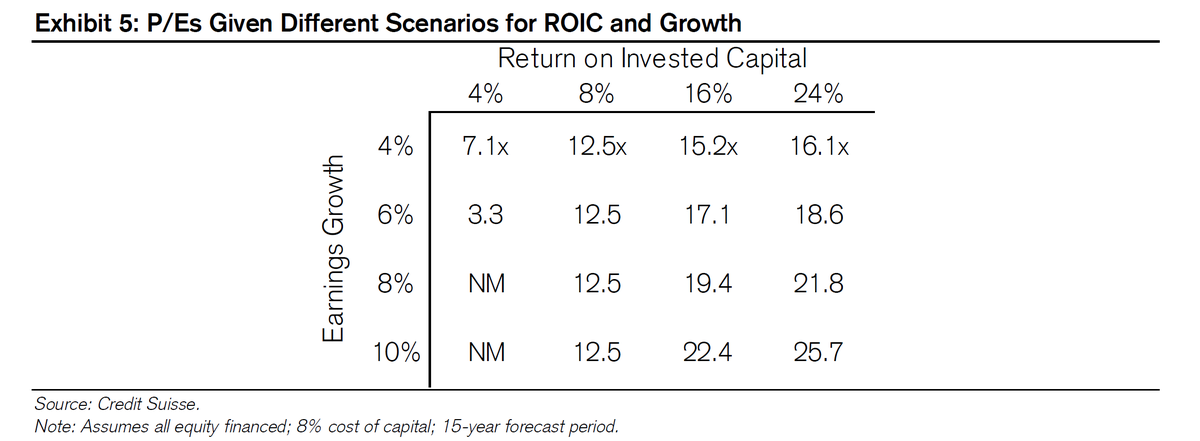

This is best seen in the below example, where only in the case where ROIIC exceeds the cost of capital (8%), is earnings growth accretive to value and thus deriving a higher multiple (at ROIIC of 8%, the business should be worth its steady state PE of 12.5x at any growth rate)

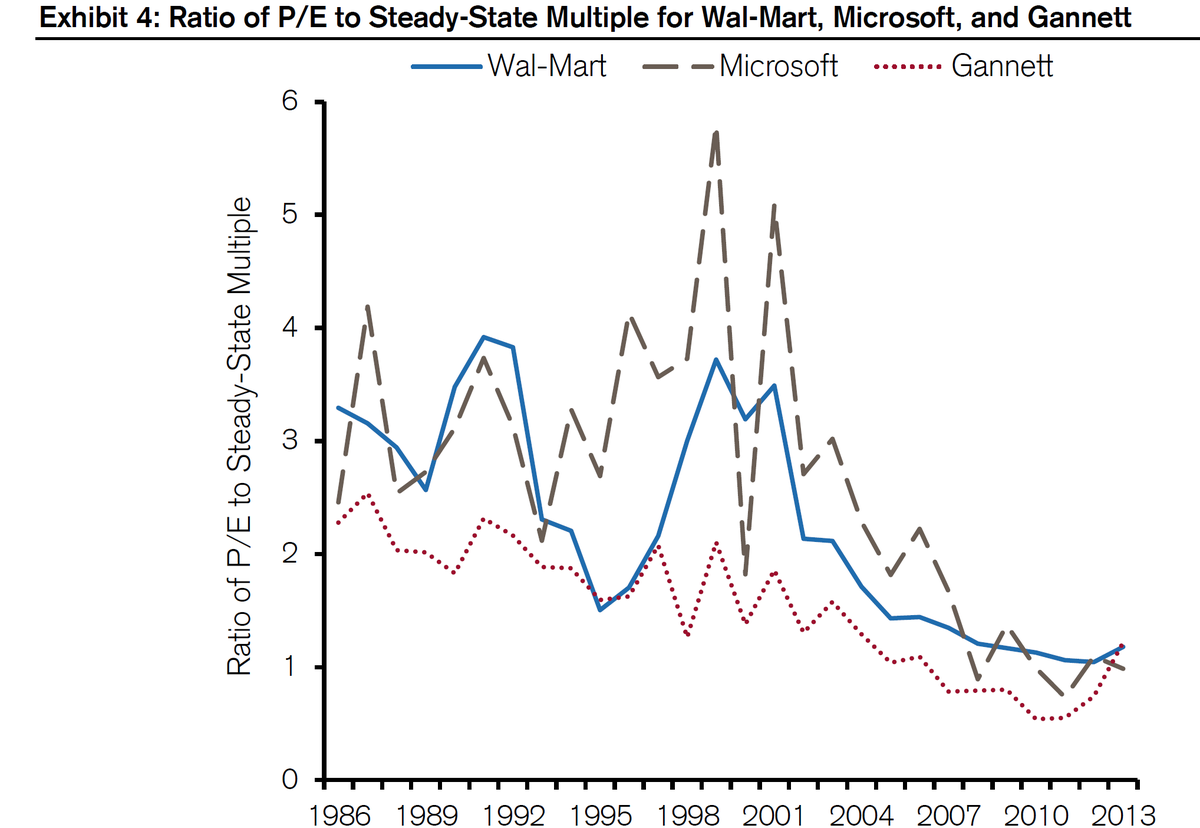

Competition will generally drive down ROIC to the CoE, meaning that a premium multiple is likely to move to the steady state multiple over time, as seen below in the P/Es for MSFT WMT GCI. The pace of the fade depends on a few factors incl. moat, investment runway, sector etc

There is a lot more interesting detail in the full paper, which I highly recommend reading

research-doc.credit-suisse.com/docView?langua…

research-doc.credit-suisse.com/docView?langua…

• • •

Missing some Tweet in this thread? You can try to

force a refresh