Climate disasters like Hurricanes Ian are making insurance unaffordable for communities exposed to climate risks. 🌪️ @chiaraarena2030 and I just proposed a way how insurers can make carbon polluters rather than their customers pay for such disasters. 🧵 context.news/climate-risks/…

As climate change spirals out of control, (un)natural disasters are becoming more frequent and expensive. 📈 Munich Re reports that they caused losses of $280 bn last year, up from $166 bn in 2019 and $210 bn in 2020. Insurers’ business models are now stretching at the seams.

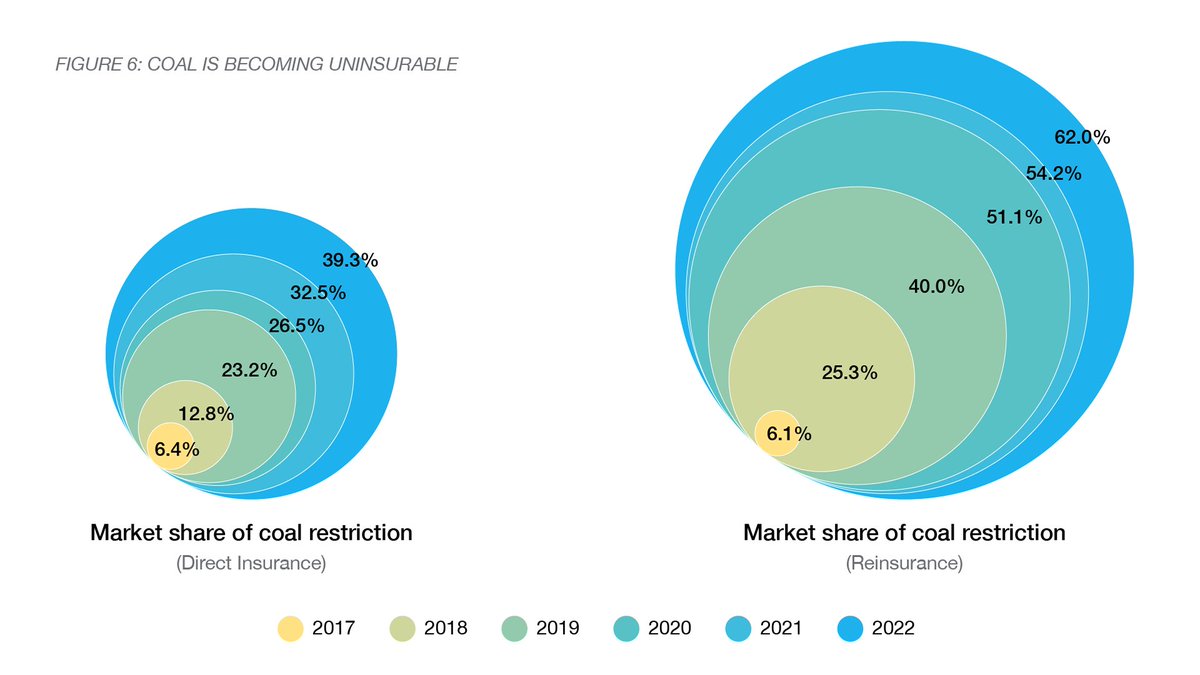

AXA’s former CEO warned in 2015: “We know that if average temperatures increase by 2°C the world may still be insurable. But it’s very clear that at +4°C it would not.” 🌡️ Even at today’s +1.2°C, insurance is becoming unaffordable for growing areas from Florida to California.

🌊 The costs of Hurricane Ian are currently estimated at >$60 bn. CoreLogic warns that as a consequence, “insurers will go into bankruptcy, homeowners will be forced into delinquency and insurance will become less accessible in regions like Florida”. 🌊

But there is another way. Climate disasters are not true ‘natural’ disasters but are caused by humans, particularly by the burning of fossil fuels. 🛢️ The Carbon Majors Database finds that just 100 companies are responsible for 71% of all carbon emissions.

👩🔬 Attribution science, which links extreme weather events to climate change, is rapidly evolving and forms the basis of numerous lawsuits against carbon majors which are currently playing out in courts around the world. 👩⚖️

Insurers can pursue legal action to reimburse their costs against third parties who caused their damages after they have paid their clients. 💵 Car insurers eg. regularly recover part of their losses through so-called subrogation claims against parties responsible for accidents.

As the costs of climate disasters are mounting, insurance companies should explore ways how they can bring similar claims 🎯 against the companies which are driving climate-related losses through their carbon emissions.

They should explore how to make big polluters pay their fair share for the cost of hurricanes like Ian. The public nuisance and negligence claims against carbon majors which are currently being tested in courts offer a valuable basis for developing potential subrogation suits. 👀

Reinsurers like @SwissRe, which are covering major natural disasters but not a lot of carbon majors, are best placed to explore such subrogation cases. They will not face the potential conflict of interest of acting as the insurer of the carbon polluter they try to sue.

Insurers have so far shied away from taking carbon polluters to court, but their current model of covering the costs of climate disasters is becoming unworkable. 🌪️ As global warming careens towards 1.5°C, the pressure to allocate these costs fairly will rapidly increase.

🍀 Through subrogation claims insurers could make polluters pay. They could keep insurance affordable for communities exposed to climate risks and send a stark message to carbon majors that they need to reconsider their role in extracting and burning fossil fuels. 🍀

Today @SwissRe announced expected losses of $1.3 bn from Hurricane Ian. As @chiaraarena2030 and I argue in this oped and 🧵, the reinsurer should take oil companies to court to cover these losses, not pass the losses on to its customers. #MakePollutersPay

• • •

Missing some Tweet in this thread? You can try to

force a refresh