A 🧵 on a co i added recently where imo risk is high but risk reward is quite favorable. Lets see how it turns out 🤞.

The co we are talking about is building TCAS :

Train collision avoidance system. Let us first understand what a TCAS is.

rdso.indianrailways.gov.in/uploads/files/…

Train collision avoidance system. Let us first understand what a TCAS is.

rdso.indianrailways.gov.in/uploads/files/…

The Indian Railways has a plan:

1. Higher capacity utilization =>

2. Higher Asset turnover =>

3. Higher profitability =>

4. A better Railways

What happens when largest railway in world gets serious about improving its ROCE?

1. Higher capacity utilization =>

2. Higher Asset turnover =>

3. Higher profitability =>

4. A better Railways

What happens when largest railway in world gets serious about improving its ROCE?

How will it accomplish this though?

1. Higher speed Trains (Remember Rando Vande Bharat videos I was watching? lol. Scuttlebutt

2. Higher speeds mean Higher chances of collisions; needs safety

3. Enter, Train Collision Avoidance System (TCAS)

1. Higher speed Trains (Remember Rando Vande Bharat videos I was watching? lol. Scuttlebutt

https://twitter.com/sahil_vi/status/1580917369114763264?s=20&t=keAdXCy3z9pW0t9CTPpPeg)

2. Higher speeds mean Higher chances of collisions; needs safety

3. Enter, Train Collision Avoidance System (TCAS)

TCAS is an indigenous Bhartiya system for detecting collisions, excessive speeding, signal passing at danger (SPAD; imagine it as Jaywalking of trains, lol. When trains SKIP a STOP sign)

During unsafe situations when brake application is necessitated, and the Crew has

either failed to do so, or is not in position to do so, automatic brake application shall take

place.

either failed to do so, or is not in position to do so, automatic brake application shall take

place.

Now how is this accomplished?

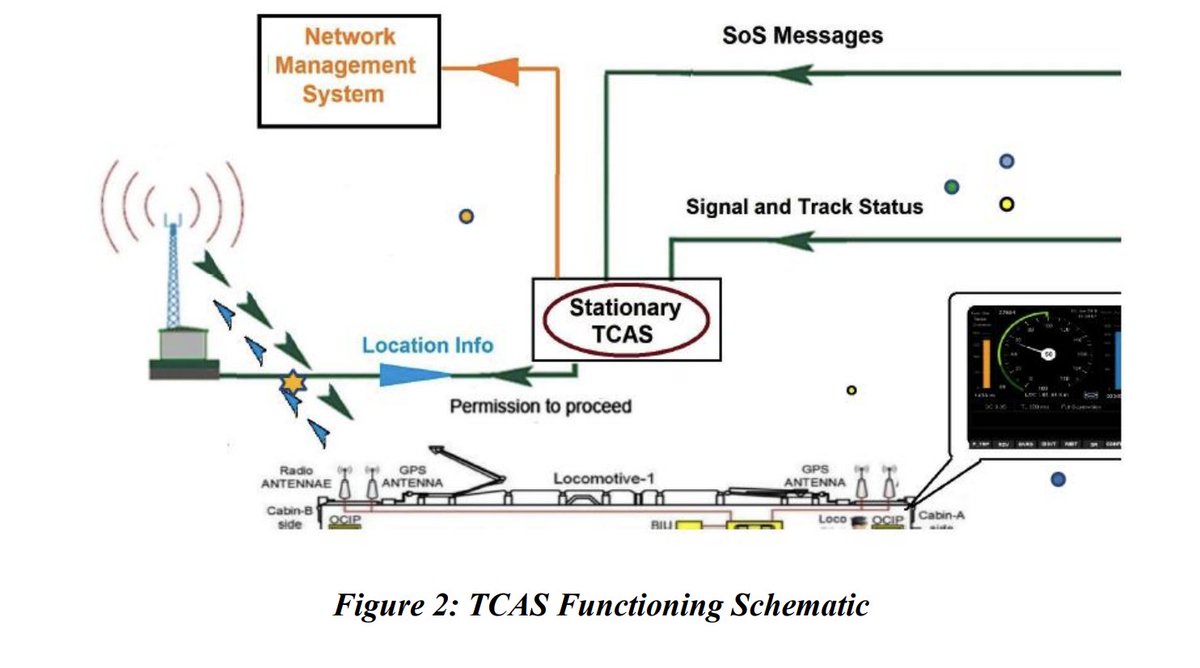

Through a system of RFID tags. The train has an RFID tag. The station gets an TFID tag and a tower. Each KM along the track, we again place RFID tags. What does this ensure?

Through a system of RFID tags. The train has an RFID tag. The station gets an TFID tag and a tower. Each KM along the track, we again place RFID tags. What does this ensure?

Each part of the system

1. The train

2. Any other train

3. The train Station

4. The train track

Talks to each other and knows about each others info. THis is literally the IoT (internet of things) dream being realized IRL (in real life).

1. The train

2. Any other train

3. The train Station

4. The train track

Talks to each other and knows about each others info. THis is literally the IoT (internet of things) dream being realized IRL (in real life).

Stationary TCAS unit (say at a point on the track) gets real-time information regarding Locations, Speed, acceleration of

various trains in its jurisdiction through UHF Radio Communication.

various trains in its jurisdiction through UHF Radio Communication.

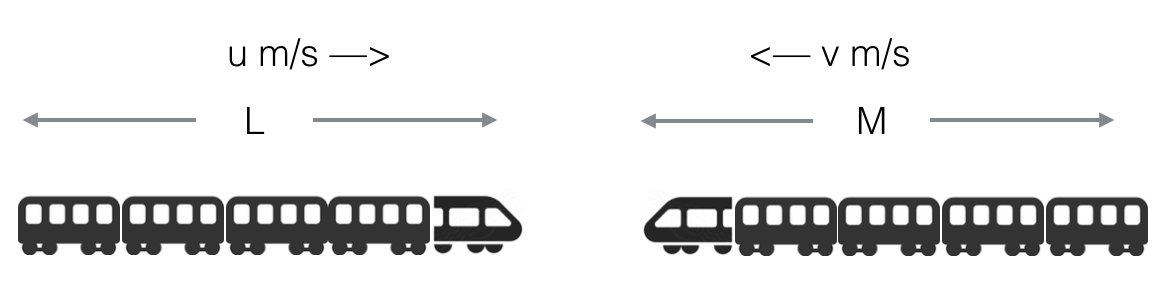

So imagine that 2 trains are approaching each other on TCAS system.

As soon as each of them crosses the respective RFID tags on their their side, the "Movement authority" (How far ahead to let it go) is set to 0 by the RFID tag since both of the RFID tags are talking to each other.

This results in automatic breaking of the trains.

This results in automatic breaking of the trains.

Communication technique used for transfer of information between Stationary and Locomotive units in station area is Full Duplex UHF Radio Communication through Multiple Access TDMA/FDMA scheme.

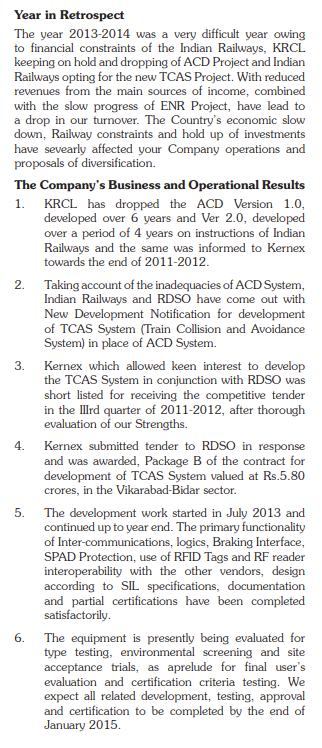

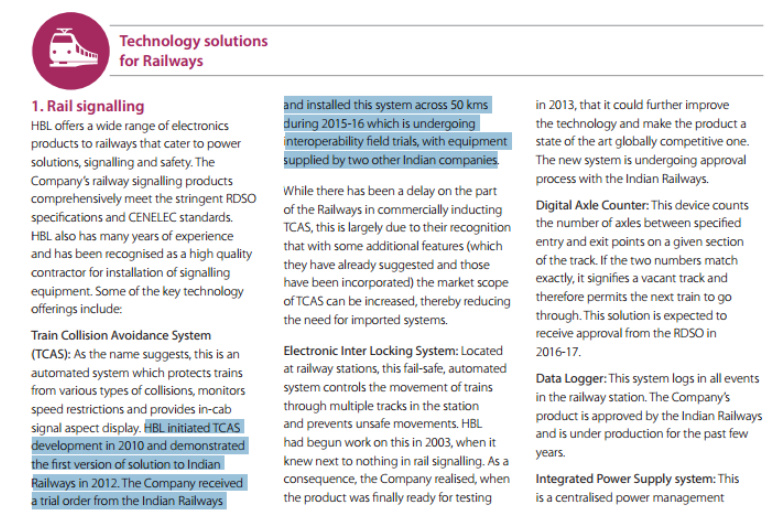

Co has been working closely with RDSO on developing these Anti Collision Device System for a decade now.

You can see from FY14 annual report that its been working since FY12.

You can see from FY14 annual report that its been working since FY12.

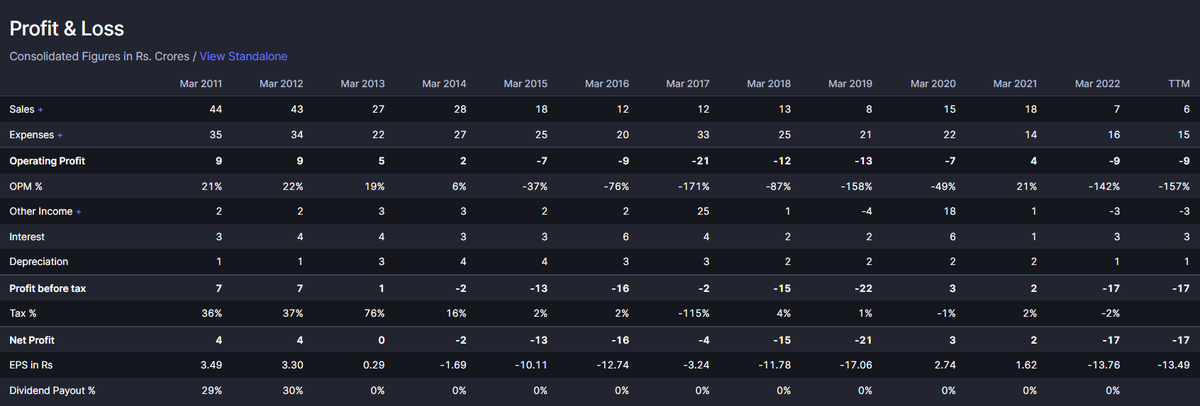

A decade of R&D, trials, working on this one thing. It can really destroy your P&L. And it has, for our co as well.

In a way we can visualize our co as a CDMO partner for RDSO (Research Design and Standards Organisation, part of Indian Railways).

In a way we can visualize our co as a CDMO partner for RDSO (Research Design and Standards Organisation, part of Indian Railways).

Naturally, the railways is cognizant of that. In order to limit competition and support healthy supplier eco-system, only 3 companies are right now allowed to productionize TCAS.

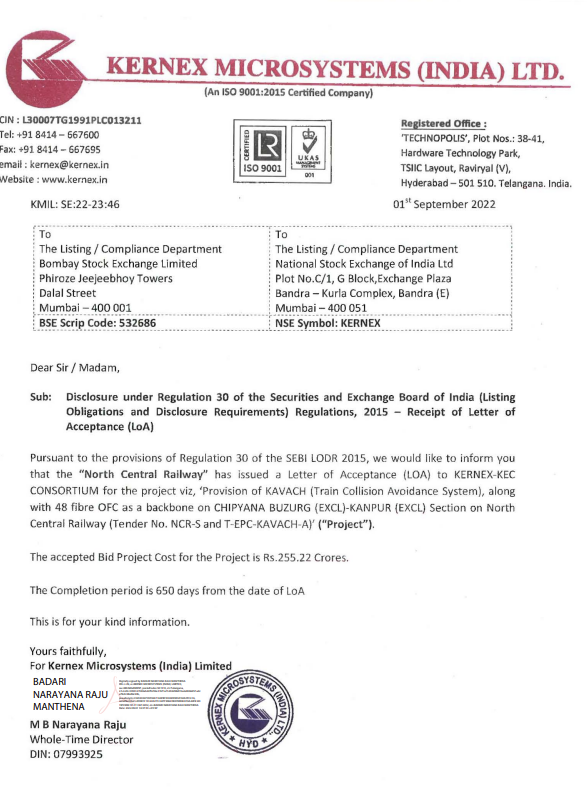

Okay, why now though? Whats happening now?

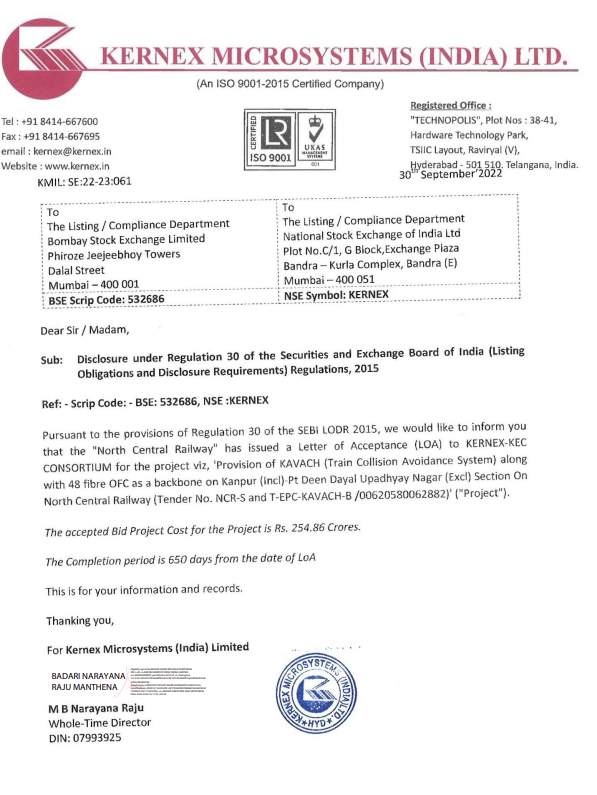

Well, in the latest AGM, it seems like finally TCAS is being rolled out. Kernex has given good details in latest AGM.

Well, in the latest AGM, it seems like finally TCAS is being rolled out. Kernex has given good details in latest AGM.

1. Total confirmed orders received by Kernex for the productionization (commercial rollout) of TCAS is 540 cr.

2. the TCAS revenue potential is roughly 2000 cr / year with 1000 cr potential from Indian railways and 1000 cr / year from export opportunities (Europe, Africa, Asia)

2. the TCAS revenue potential is roughly 2000 cr / year with 1000 cr potential from Indian railways and 1000 cr / year from export opportunities (Europe, Africa, Asia)

3. Right now only 3 competitors. 2 more are developing their systems (Quadrant Future tek, GG Tronics). So for next 2-3 years, 3 competitors (kernex is one of them) and after 2-3 years 5 competitors (potentially)

4. Management expects this to be a 25-30% EBITDA, 15% Net profit margin business

5. For 600cr of orders (Current order book), 80cr of WC. 30cr of debt, and 50cr of preferential issue of equity (~10% dilution).

Payment terms with Railways are great. Gets paid within a week of raising an invoice. Bonus for early completion of contract.

Payment terms with Railways are great. Gets paid within a week of raising an invoice. Bonus for early completion of contract.

6. With existing fixed assets, co can easily manage for next 3-4 years and up to 500-1000 cr topline.

7. Of current order book of 540 cr: Co expects 60cr revenue in Q4FY23, and 280 cr in FY24, rest in FY25.

7. Of current order book of 540 cr: Co expects 60cr revenue in Q4FY23, and 280 cr in FY24, rest in FY25.

Just valuing kernex on FY24 profits of 42 cr (280*0.15) its at a P/E multiple of around 11. With some dilution, maybe around 12-13 P/E multiple. This is why i think risk reward is in favor. Revenue potential from India alone is 330cr a year (given there are 3 competitors).

TCAS costs are around 30-50 lakh per KM. India has 1 lakh KM of railway. This works out to 30-50k cr total opportunity. If over a decade or more kernex captures 20% of it, it would have executed 6k - 10k cr worth of TCAS.

The Maintenance & support revenue at 5% of total execution could lead to 300-500cr of annuity revenue in perpetuity.

Lets also discuss the risks:

1. The largest customer is Sarkar-e-hind : Bharat Sarkar : Government of India. We all know how it goes with Govt. Delays are the least thing to expect. On top of it, potential for revenue disputes.

1. The largest customer is Sarkar-e-hind : Bharat Sarkar : Government of India. We all know how it goes with Govt. Delays are the least thing to expect. On top of it, potential for revenue disputes.

2. All earnings are in the future. We are paying for future execution so must discount the risk of that execution never happening. This is why i called this a high risk investment

3. There could be a political risk as well. If the central government changes, focus on railway could entirely go away (Customer's capital & Opex allocation decisions are not consistent).

Please do remember that I am not a sebi registered advisor, and this is in no way a buy or sell recommendation. I am sharing my research with the hope it might motivate you to study as well and maybe share some insights with me.

Please do your own due diligence before putting your capital at risk. Your profits, your losses, your capital.

Some other company threads you might like:

Thats the end of the thread. Happy Diwali everyone. Stay safe.

https://twitter.com/sahil_vi/status/1406848206181335046?s=20&t=rv_E9Ah-riF630b7vEm7fA

Thats the end of the thread. Happy Diwali everyone. Stay safe.

• • •

Missing some Tweet in this thread? You can try to

force a refresh