How do you trace assets of a deceased family member? Say your aunt names you as heir in a Will but you don't know about her investments. What to do? Or your dad leaves you stocks, but you don't know the demat number. @maulik_madhu has a roadmap. Read here: livemint.com/money/personal…

First things first. A Will is ideally supposed to contain all this info. But often there is no Will. Or the Will doesn't have enough details. Or the Will is outdated. It may be made 5 or 10 yrs ago when the person's investments were quite different. What do you do?

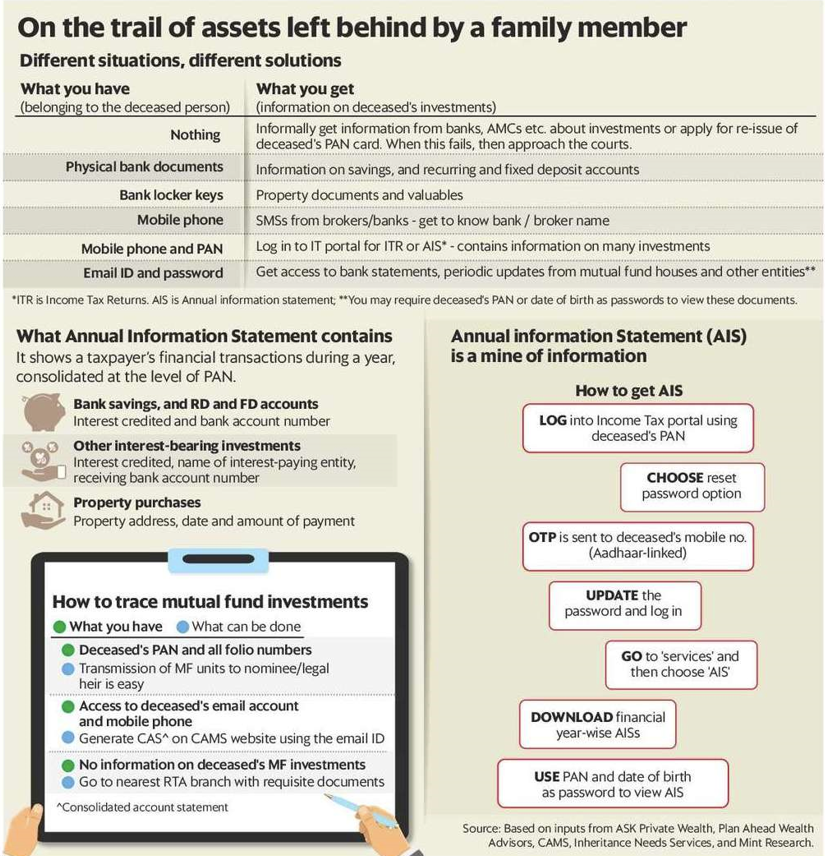

1) Look for a doc that would have most of the person's assets. For example, the Annual Information Statement (AIS) which can be accessed through the Income Tax Portal. However for that you need to know the deceased's PAN and have access to their Aadhar-linked mobile phone

2) Look for ancillary documents like the Consolidated Account Statement (CAS) for #mutualfunds. You can request a consolidated CAS from the CAMS/Kfintech website which will be sent to the deceased person's email. You will need access to this email.

3) In the worst case scenario, you can get a court order directing MF (RTAs) and depositories to tell you account details. But this means lawyer's fees and it can be extremely time consuming. To avoid this, just have a frank conversation with your family - awkward but important

Also valuable inputs from @NamrataPatel06

• • •

Missing some Tweet in this thread? You can try to

force a refresh