1/ Co-ownership ≠ automatic protection

1/ Co-ownership ≠ automatic protection

A level 2 explanation:

A level 2 explanation:

Home Buying

Home Buying

Among individuals, direct is more favored by HNIs.

Among individuals, direct is more favored by HNIs.

Phase II: 1997 to 2017 was a golden age of low tax rates

Phase II: 1997 to 2017 was a golden age of low tax rates

6 reasons to go:

6 reasons to go: 2. The Strand (near Radio Club). Large rooms and a nice rooftop restaurant (Harbour view). Breakfast is generally included in your room fare.

2. The Strand (near Radio Club). Large rooms and a nice rooftop restaurant (Harbour view). Breakfast is generally included in your room fare.

There are however reasons to buy a higher cover today.

There are however reasons to buy a higher cover today. Middle class habits do not change overnight. Bengaluru based Rohan Chandrashekhar still drives a hatchback worth Rs 7 lakh and shops online from mid-segment clothes brands. Ghaziabad based Shubham Garg said he upgraded to a bigger home, but his lifestyle hasn't changed much.

Middle class habits do not change overnight. Bengaluru based Rohan Chandrashekhar still drives a hatchback worth Rs 7 lakh and shops online from mid-segment clothes brands. Ghaziabad based Shubham Garg said he upgraded to a bigger home, but his lifestyle hasn't changed much.

There isn't much of an argument for investing in Portfolio Management Services. They have largely grown over the past few years on the back of hefty fees and expenses. This is slowly changing. #Sebi banned upfront commissions in PMS and introduced direct plans only in 2020.

There isn't much of an argument for investing in Portfolio Management Services. They have largely grown over the past few years on the back of hefty fees and expenses. This is slowly changing. #Sebi banned upfront commissions in PMS and introduced direct plans only in 2020.

Says Sebi not looking to disintermediate brokers with regulations such as upstreaming money to clearing corporations. Huge client funds lying with brokers is a risk.

Says Sebi not looking to disintermediate brokers with regulations such as upstreaming money to clearing corporations. Huge client funds lying with brokers is a risk.

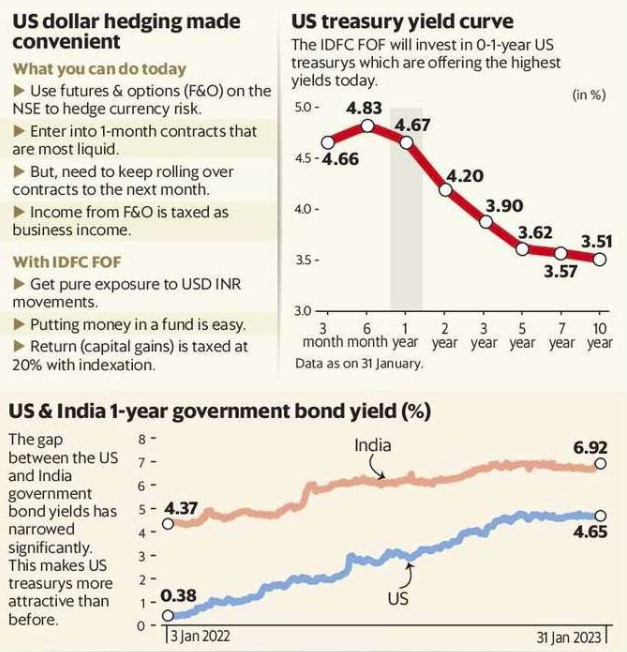

First, when the US Fed hikes rates, everything (stocks, bonds, gold) goes down. Only the yields on US treasuries go up. But for Indians there was no straightforward way to benefit from rising treasury yields. From next month, there will be.

First, when the US Fed hikes rates, everything (stocks, bonds, gold) goes down. Only the yields on US treasuries go up. But for Indians there was no straightforward way to benefit from rising treasury yields. From next month, there will be.

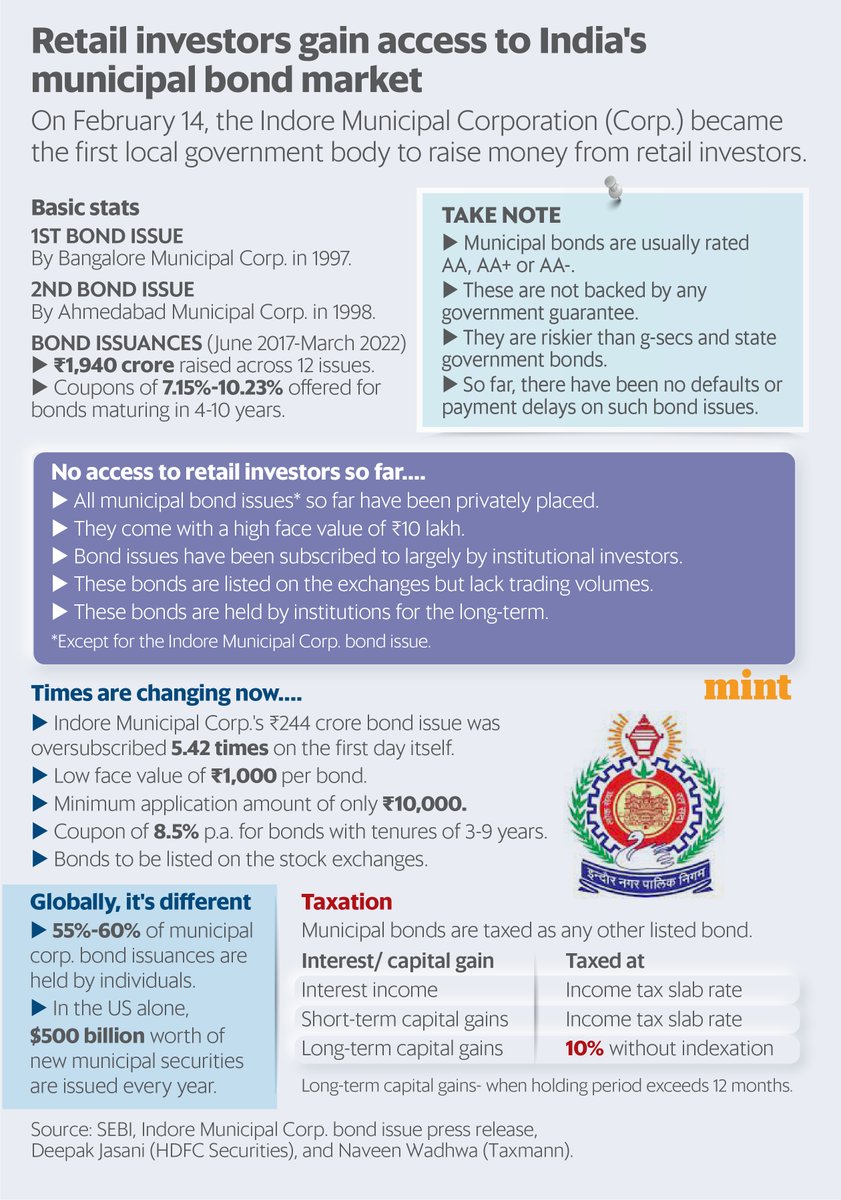

Quite simply, until Indore Municipality came out with a public issue on Feb 14th 2023, municipal bond issues were few and far between. They were also 'privately placed' - offered to select investors. The minimum face value (until Oct 2022) for private placement was Rs 10 lakh.

Quite simply, until Indore Municipality came out with a public issue on Feb 14th 2023, municipal bond issues were few and far between. They were also 'privately placed' - offered to select investors. The minimum face value (until Oct 2022) for private placement was Rs 10 lakh.