About -

Over the last three decades, HFCL has

transformed into a leading innovation-led

technology enterprise from a telecom

equipment manufacturer, offers wide

range of next-gen communication

products & integrated solutions to

diverse sectors.

Over the last three decades, HFCL has

transformed into a leading innovation-led

technology enterprise from a telecom

equipment manufacturer, offers wide

range of next-gen communication

products & integrated solutions to

diverse sectors.

The Company produces Optical Fibre,

Optical Fibre Cables, passive components & other cutting-edge transmission & access equipment.

HFCL also has an established track record of providing end-to-end communication

network solutions to it's customer across the globe.

Optical Fibre Cables, passive components & other cutting-edge transmission & access equipment.

HFCL also has an established track record of providing end-to-end communication

network solutions to it's customer across the globe.

Global presence -

HFCL has an international presence in 30+ countries.

HFCL has an international presence in 30+ countries.

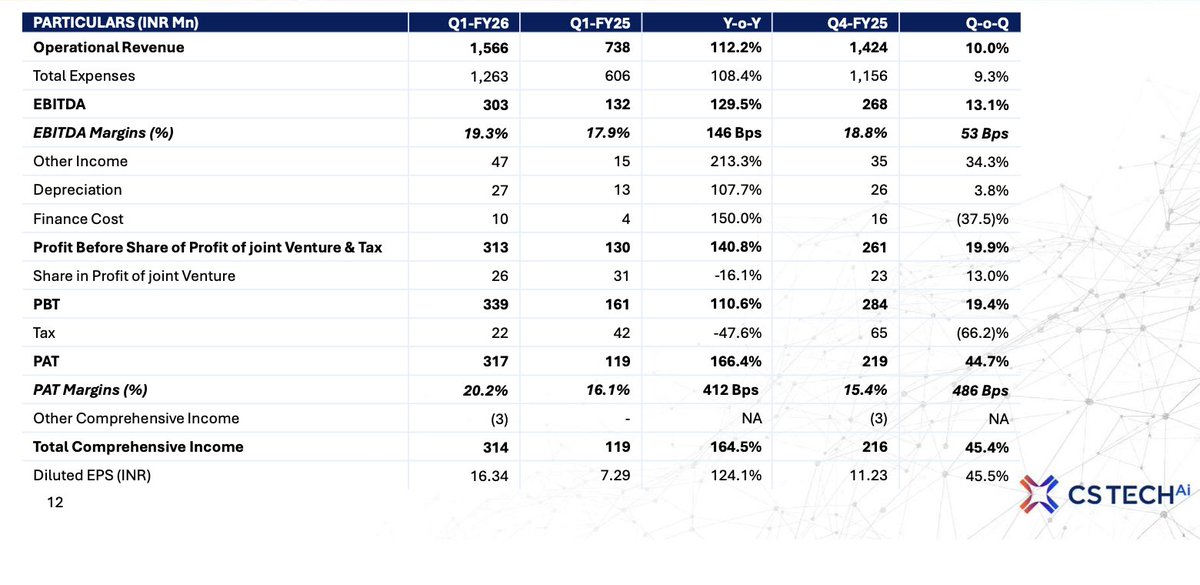

Financials -

Revenue has roughly grown at (16%) CAGR & PAT by (21.4%) CAGR over the last 5yrs.

Current EBITDA margins are at the level of 15%.

ROCE is 19.3%.

₹5,280 Cr + (~USD 649 mn) Order Book as on 30th Sep, 2022.

Revenue has roughly grown at (16%) CAGR & PAT by (21.4%) CAGR over the last 5yrs.

Current EBITDA margins are at the level of 15%.

ROCE is 19.3%.

₹5,280 Cr + (~USD 649 mn) Order Book as on 30th Sep, 2022.

Revenue Breakup -

HFCL earns (76%) of its Revenue from Public Telecommunication, (21%) from Defence Communication & Electronics, and (3%) from Railway Communication.

Current Order Book as on 30th Sep, 2022:

Public Telecom ~ Rs1,757+Cr

Defence Com ~ 2,069+Cr

Railway Com ~ 320+Cr

HFCL earns (76%) of its Revenue from Public Telecommunication, (21%) from Defence Communication & Electronics, and (3%) from Railway Communication.

Current Order Book as on 30th Sep, 2022:

Public Telecom ~ Rs1,757+Cr

Defence Com ~ 2,069+Cr

Railway Com ~ 320+Cr

Products -

▪️Optic Fibre / Optical Fibre Cables:

HFCL offers a wide range of optical fiber cable solutions for various applications, including underground, aerial, micro duct, FTTH & last mile connectivity.

▪️Optic Fibre / Optical Fibre Cables:

HFCL offers a wide range of optical fiber cable solutions for various applications, including underground, aerial, micro duct, FTTH & last mile connectivity.

It's Fiber optic solutions support long-distance data transmission, high bandwidth & speed, a high degree of flexibility, reliability & durability.

▪️Public Telecommunication:

HFCL offers comprehensive range of telecom products and solutions for all network requirement.

HFCL offers comprehensive range of telecom products and solutions for all network requirement.

▪️Defence Communication & Electronics:

Defence product portfolio caters to strategic applications required across defence forces, border security & law enforcement.

Defence product portfolio caters to strategic applications required across defence forces, border security & law enforcement.

▪️Passive Networking Components:

Offer end-to-end solutions for both data & telecom applications, with a view to enable service providers meet their customers’ demand for higher bandwidth.

Offer end-to-end solutions for both data & telecom applications, with a view to enable service providers meet their customers’ demand for higher bandwidth.

Renowned to facilitate faster and enhanced connectivity experience, there fiber and copper cabling solutions are the product of choice for leading Indian as well as global telecom service providers.

Clientele -

HFCL's client base includes Jio, Tata, airtel, vodafone, Nokia, L&T, Orange, BSNL, BBNL, TCIL, BPCL, IOL, Railtel, GAIL, Saudi Railways and others.

HFCL's client base includes Jio, Tata, airtel, vodafone, Nokia, L&T, Orange, BSNL, BBNL, TCIL, BPCL, IOL, Railtel, GAIL, Saudi Railways and others.

Manufacturing Capabilities -

Presently, the company has 5 manufacturing facilities across Telangana, Tamil Nadu, Himachal and Goa.

Capacities are:-

Optical Fibre Cable - 23.35m fkm

FTTH Cable - 630k ckm

Optic Fibre - 8mn fkm

Presently, the company has 5 manufacturing facilities across Telangana, Tamil Nadu, Himachal and Goa.

Capacities are:-

Optical Fibre Cable - 23.35m fkm

FTTH Cable - 630k ckm

Optic Fibre - 8mn fkm

R&D Capabilities -

HFCL has 2 in-house R&D located at Gurgaon & Bengaluru.

The company has also invested is external R&D Houses & collaborated with technology companies in 🇮🇳 & abroad to develop innovate futuristic range of technology products and solutions.

HFCL has 2 in-house R&D located at Gurgaon & Bengaluru.

The company has also invested is external R&D Houses & collaborated with technology companies in 🇮🇳 & abroad to develop innovate futuristic range of technology products and solutions.

Strategic Partnerships 🤝 -

The Company formed strategic partnerships with various global accredited names to drive product development, integrating its capacities & accelerating growth from industrial collaborations.

The Company formed strategic partnerships with various global accredited names to drive product development, integrating its capacities & accelerating growth from industrial collaborations.

HFCL has a strong association with Reliance Jio Infocomm Ltd & has been responsible for network planning, design and implementation of its network for the Northern region of India.

Growth Drivers -

~ Government initiatives for telecom connectivity to significantly enhance the

demand for OFCs. Indian OFC market was valued at $530 mn in FY20 & is expected to grow to reach $700 mn by FY25.

~ Government initiatives for telecom connectivity to significantly enhance the

demand for OFCs. Indian OFC market was valued at $530 mn in FY20 & is expected to grow to reach $700 mn by FY25.

~ Rising competition among OEMs, availability of cheaper 5G chipsets and declining prices of devices are expected to make brands push more 5G devices into the market.

As of March 2022, 🇮🇳’s tower fibreisation stood at 33%, leaving plenty of room for growth as the country strives to reach 70% tower fibreisation by 2025. As a result, demand for OFC networks & related solutions has risen significantly & expected to increase further in coming yrs.

~ New opportunities from Indian aerospace & defence:

🇮🇳 plans to spend US$130 bn to

modernize armed forces & strengthen combat capabilities from FY21-26. The Indian A&D Industry is very PSU & Govt organisations dependent but the avenue for Private Sector is opening rapidly.

🇮🇳 plans to spend US$130 bn to

modernize armed forces & strengthen combat capabilities from FY21-26. The Indian A&D Industry is very PSU & Govt organisations dependent but the avenue for Private Sector is opening rapidly.

~ Opportunity in Railway Communication System:

The capex outlay for FY22 was INR 2,15,000 cr, which is more than 5.0X of 2014 level & this run rate is expected to increase in the current decade.

The capex outlay for FY22 was INR 2,15,000 cr, which is more than 5.0X of 2014 level & this run rate is expected to increase in the current decade.

Railways are now adopting information technology & computerization in large-scale for its internal use & to meet passenger expectations.

Capitalising on Global Opportunities -

As one of the largest infrastructure providers in South East Asia, HFCL recognised the potential of European

markets & formed strategic alliances with local players in these regions to provide EPC services for OFC / FTTH rollout.

As one of the largest infrastructure providers in South East Asia, HFCL recognised the potential of European

markets & formed strategic alliances with local players in these regions to provide EPC services for OFC / FTTH rollout.

Key Risks -

• If telecom products business fails to scale up as per forecasts due to any micro or macro hurdles, then revenue & profitability could be affected.

• If there are disruptions in the roll out of 5G networks, growth of the company could get delayed.

• If telecom products business fails to scale up as per forecasts due to any micro or macro hurdles, then revenue & profitability could be affected.

• If there are disruptions in the roll out of 5G networks, growth of the company could get delayed.

Conclusion -

HFCL is marching ahead with determination and commitment on the path of sustainable & profitable growth fuelled by continued expansion of capacities, creation of new capacities, innovative product offerings, backward and forward integration, increased

HFCL is marching ahead with determination and commitment on the path of sustainable & profitable growth fuelled by continued expansion of capacities, creation of new capacities, innovative product offerings, backward and forward integration, increased

customer base and expanding global footprint. Other factors backing the Company’s growth include increasing need for high speed & secure communication network worldwide.

Please 🙏 like 👍,comment, retweet ♻️ if you find this 🧵 useful.

And follow us on @LnprCapital for more information like this.

@nid_rockz @VVVStockAnalyst @harrie007

And follow us on @LnprCapital for more information like this.

@nid_rockz @VVVStockAnalyst @harrie007

https://twitter.com/LnprCapital/status/1587278551031500800?t=KZJr746TFPlTqQhDtCjNiQ&s=19

• • •

Missing some Tweet in this thread? You can try to

force a refresh