Alright alright, we got the eucalyptus tea brewed, we have one of the Koala's go to modeling playlists cranking...it's time for a Whitehaven Coal $WHC.AX valuation thread

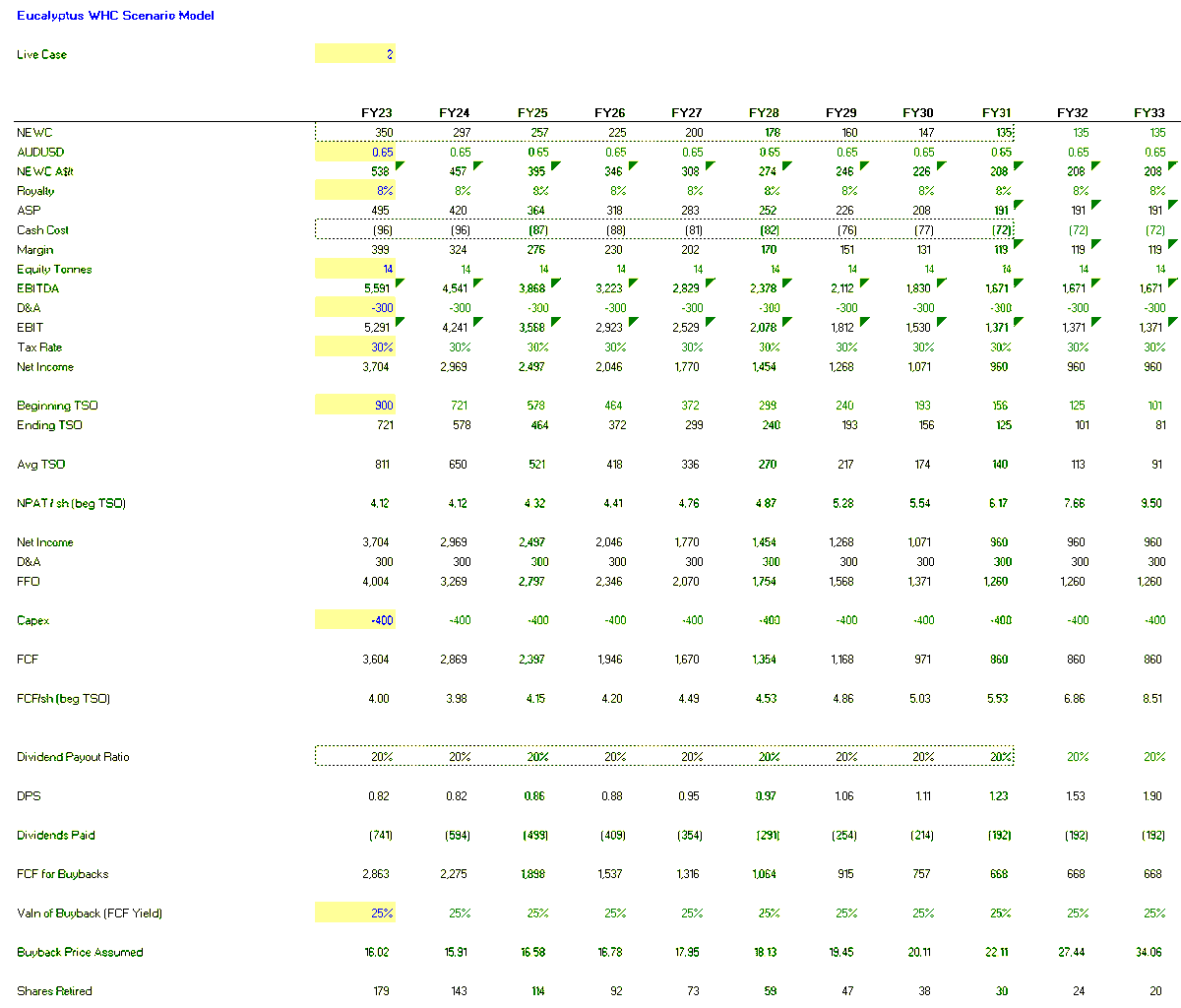

First let's start with our 6 scenarios...1/n

First let's start with our 6 scenarios...1/n

https://twitter.com/thebiglong9/status/1587729257370984448

Also let's highlight a couple assumptions here:

Have cash costs sliding as energy crisis "resolves" through the decade

30% cash tax rate

14MM equity tonnes per year through FY2050 (yea Gunnedah open cuts, etc.)

2/n

Have cash costs sliding as energy crisis "resolves" through the decade

30% cash tax rate

14MM equity tonnes per year through FY2050 (yea Gunnedah open cuts, etc.)

2/n

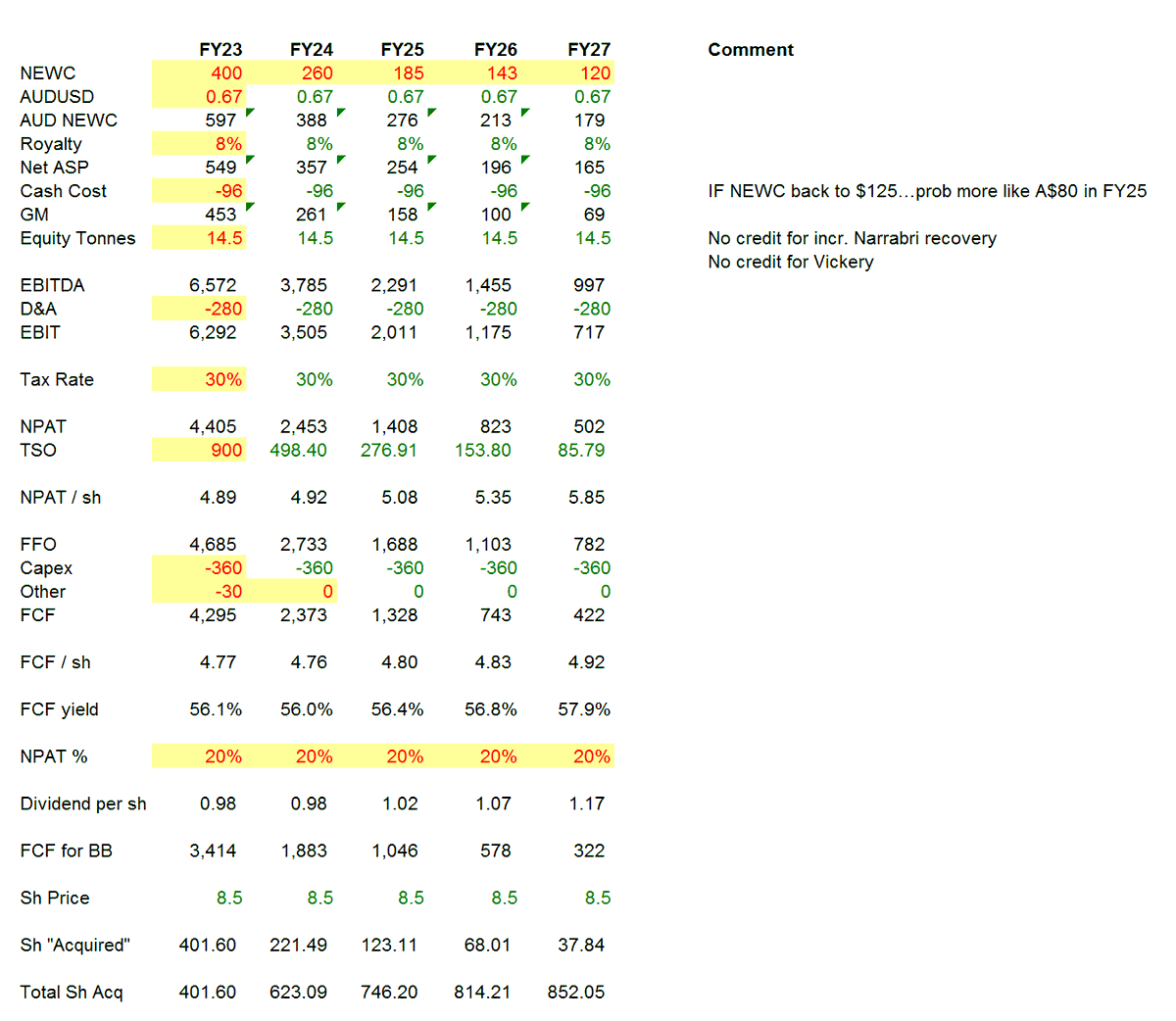

Figure

a) small guide cut this yr

b) Maules 30+, Narrabri '44 (close enough)

So yea no Vickery or Winchester but w/e

Capex 400/yr

3/n

a) small guide cut this yr

b) Maules 30+, Narrabri '44 (close enough)

So yea no Vickery or Winchester but w/e

Capex 400/yr

3/n

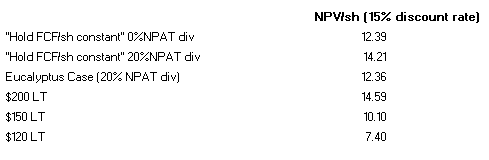

Used a 15% discount rate, these are the NPV/sh for each case:

Remember NPV is a point in time today. Does not reflect if buybacks will be accretive or not (using June 30th balance sheet which was pf net debt zero share balance)

4/n

Remember NPV is a point in time today. Does not reflect if buybacks will be accretive or not (using June 30th balance sheet which was pf net debt zero share balance)

4/n

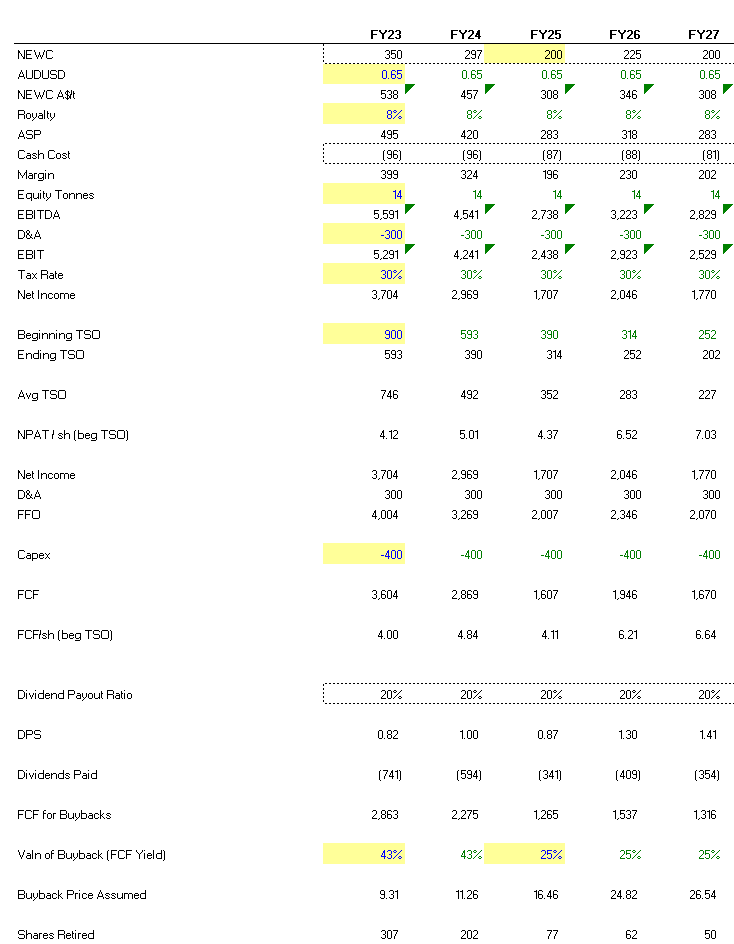

So now that we are past the NPV today question, the buyback value creation question comes into play

Let's look at if you buyback at a 25% FCF yield in FY23...well FCF/sh is A$4 so let's say we have a 20% NPAT div and rest of FCF goes to buybacks (case 2)

5/n

Let's look at if you buyback at a 25% FCF yield in FY23...well FCF/sh is A$4 so let's say we have a 20% NPAT div and rest of FCF goes to buybacks (case 2)

5/n

Assuming a constant multiple (25% spot FCF yield) we need to see $297/t NEWC average in FY24 for the share price to stay at ~A$16...that's a bold one

Minor detail though, and very important with buyback value creation...we are not at 25% right now...we are at...43% yield

6/n

Minor detail though, and very important with buyback value creation...we are not at 25% right now...we are at...43% yield

6/n

Guess what NEWC price the koala needs in FY24 to hold the same FCF/sh & share price at 43% FCF yield...$260/t...that's almost $30/t on NEWC

That was a big deal in coal price before things got weird at this party!

Except, multiples SHOULD re-rate as we move towards LT price 7/n

That was a big deal in coal price before things got weird at this party!

Except, multiples SHOULD re-rate as we move towards LT price 7/n

So the q of the buyback becomes what is your LT coal price and the right FCF yield (or put another what is your discount rate for owning a high quality thermal coal stock)

It's a circular debate we could have until Net Zero actually happens for the koala's grandchildren 8/n

It's a circular debate we could have until Net Zero actually happens for the koala's grandchildren 8/n

At least where the koala has settled out, think the buyback is accretive and the right number for this company is somewhere between A$15-20/sh and will explain it this way...

9/n

9/n

No one is investing in thermal coal

Do not think this spike is either the last one or imminently over (see all decks above assume no spike at all in the future)

So Vickery has some optionality value

Esp since LT NEWC prob $150+ 10/n

Do not think this spike is either the last one or imminently over (see all decks above assume no spike at all in the future)

So Vickery has some optionality value

Esp since LT NEWC prob $150+ 10/n

But as someone else pointed out, this is a personal journey for everyone in the market

The dream would be WHC can buyback 50% of the company this FY and next, coal is still over $200/t and the world wakes up and goes "oh fuck" 11/n

The dream would be WHC can buyback 50% of the company this FY and next, coal is still over $200/t and the world wakes up and goes "oh fuck" 11/n

So for fun let's look at that 43% FCF yield situation

Instead of 25% FCF yield bb price & then in FY25 NEWC avg "only" $200 but mkt decides WHC finally merits a 25% FCF yield

A$16.50 sh px & A$1.80 divs, there is some value uplift v 100% FCF div payout even before taxes

12/n

Instead of 25% FCF yield bb price & then in FY25 NEWC avg "only" $200 but mkt decides WHC finally merits a 25% FCF yield

A$16.50 sh px & A$1.80 divs, there is some value uplift v 100% FCF div payout even before taxes

12/n

But the buyback is really a call on two things:

NEWC will be higher for longer with 2020s avg price being much higher than most expect (koala agrees)

At some point the market recognizes high quality thermal has a longer runway and re-rates the sector even a little 13/n

NEWC will be higher for longer with 2020s avg price being much higher than most expect (koala agrees)

At some point the market recognizes high quality thermal has a longer runway and re-rates the sector even a little 13/n

Which the koala also agrees on

If you agree with both of those, you want the buyback done aggressively up to say a 20-25% FCF yield level

Fwiw, if NEWC avg $150/t in FY24, need a 15% FCF yield for WHC to be ~A$9.30

14/n

If you agree with both of those, you want the buyback done aggressively up to say a 20-25% FCF yield level

Fwiw, if NEWC avg $150/t in FY24, need a 15% FCF yield for WHC to be ~A$9.30

14/n

Having fun noodling away here with the eucalyptus tea on the buyback circularity and various scenarios but we can distill this to one thing:

Think WHC should be A$15-20/sh and company should be buying back stock in size below those levels

15/n

Think WHC should be A$15-20/sh and company should be buying back stock in size below those levels

15/n

And the simple math there is using a brutal 15% discount rate (for an UNLEVERED company) the koala gets A$12-15/sh of intrinsic value with no value assigned to Vickery or Winchester South

Drop discount rate lower and things would get really wild...16/n

Drop discount rate lower and things would get really wild...16/n

Think it's important for us to disaggregate two dicussions we tend to co-mingle.

What is the value of the stock TODAY?

What is the capital allocation framework and will that CREATE or DESTROY incremental value?

17/n

What is the value of the stock TODAY?

What is the capital allocation framework and will that CREATE or DESTROY incremental value?

17/n

Anyways, this is not the koala's best or most concise thread, even the marsupial gets stuck in the circular fun of buyback value creation / destruction

Hope you've enjoyed it

One last thought 18/n

Hope you've enjoyed it

One last thought 18/n

If you think Whitehaven should NOT be buying back stock here and just harvesting cash hard (and leave franking credits out this, ~1/2 register offshore), then you think coal is about to crater and this is the best it'll ever be, a question: why do you even own the stock?

19/19

19/19

• • •

Missing some Tweet in this thread? You can try to

force a refresh