Also let's highlight a couple assumptions here:

Also let's highlight a couple assumptions here:

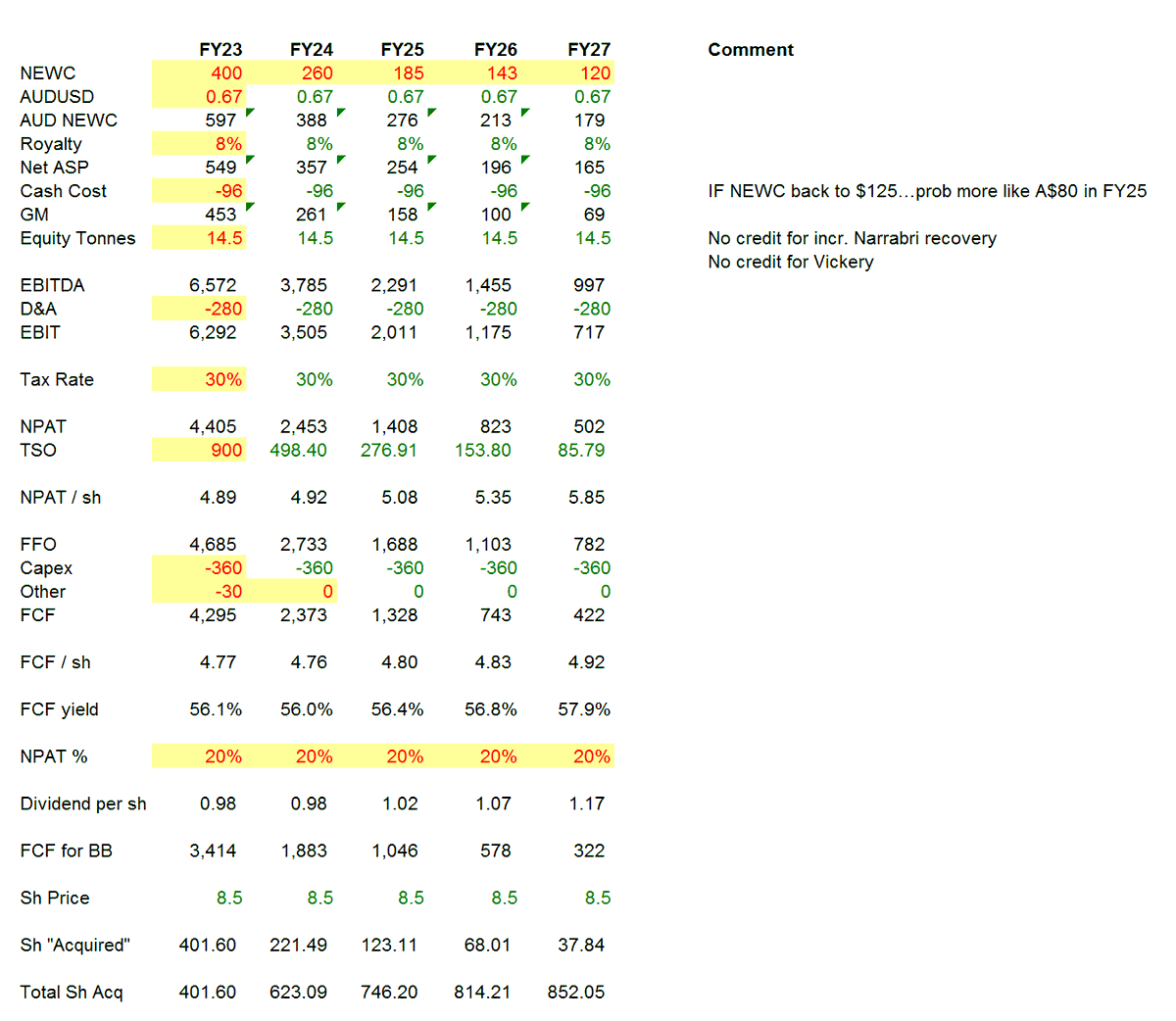

Using those same parameters, extrapolate out FY24-27 with the established capital alloc policy (20% NPAT in divvy, rest in buyback up to 50%, and koala has allocated last 50% to buyback as well) & pretended stock didn't move, what's implied NEWC to get same FCF yield each yr 2/n

Using those same parameters, extrapolate out FY24-27 with the established capital alloc policy (20% NPAT in divvy, rest in buyback up to 50%, and koala has allocated last 50% to buyback as well) & pretended stock didn't move, what's implied NEWC to get same FCF yield each yr 2/n

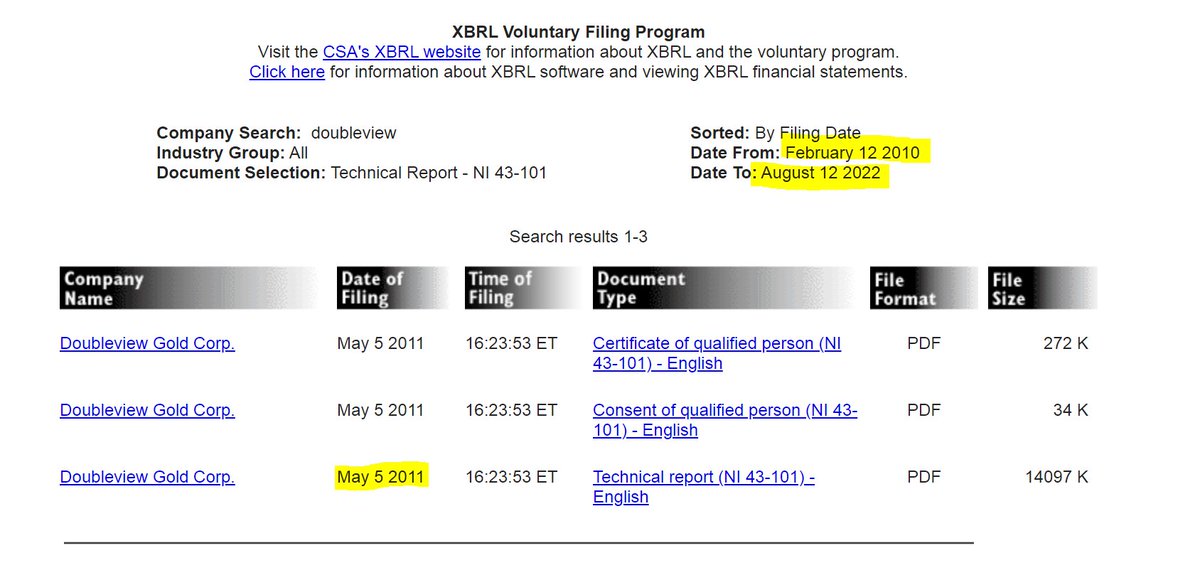

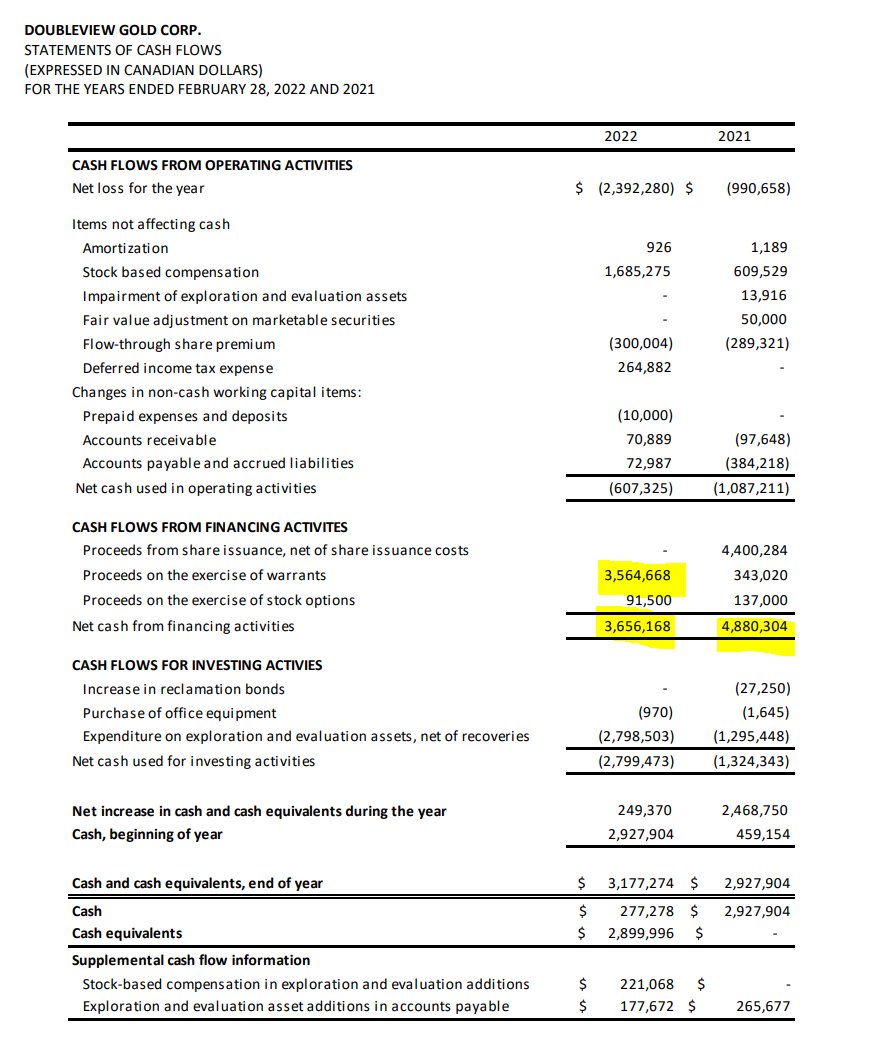

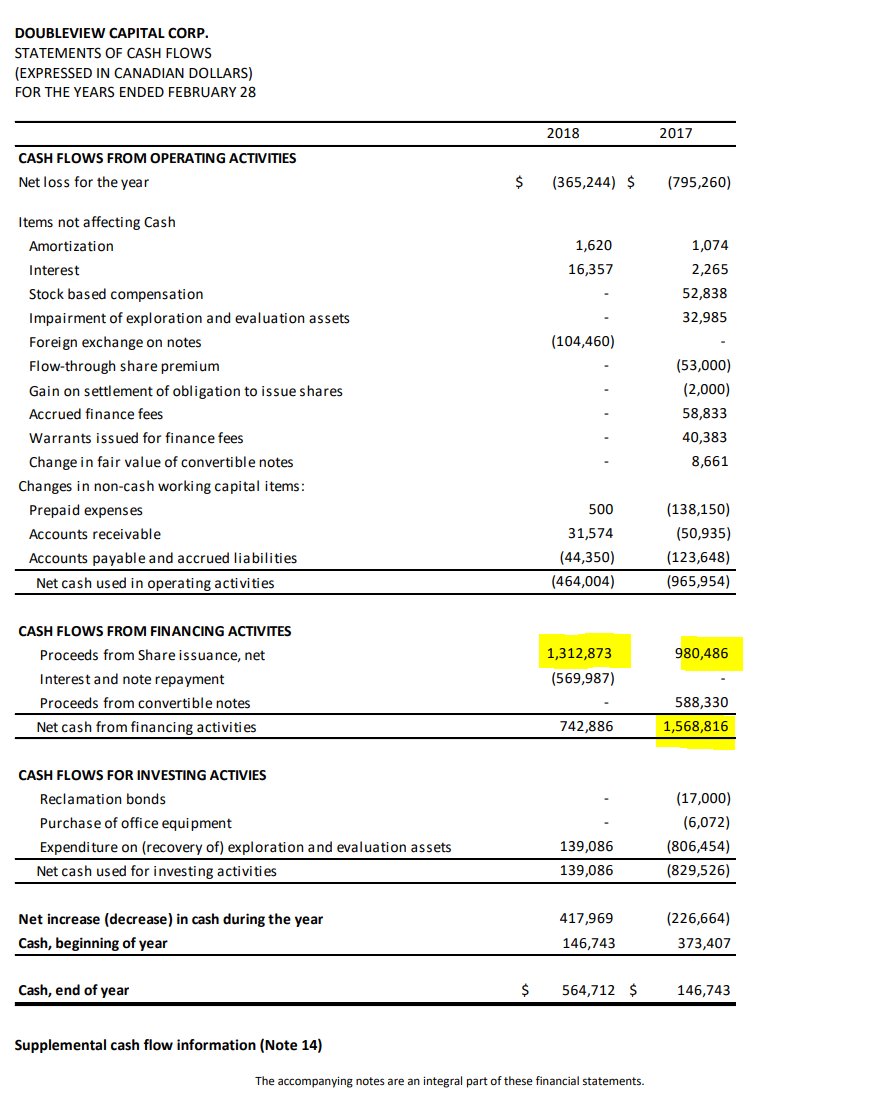

2015-22 screenshots (Feb YE)

2015-22 screenshots (Feb YE)

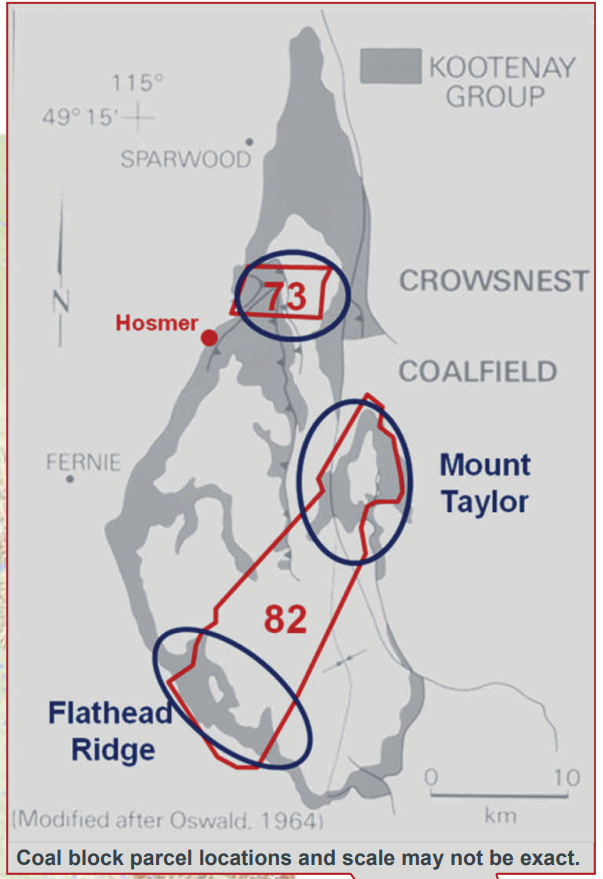

Two parcels of land the government kept while giving everything else to CP as incentive to build the railroad...and that the Canadian federal govt still hold today...Parcel 73 and 82 right in the heart of the Elk Valley 2/n

Two parcels of land the government kept while giving everything else to CP as incentive to build the railroad...and that the Canadian federal govt still hold today...Parcel 73 and 82 right in the heart of the Elk Valley 2/n