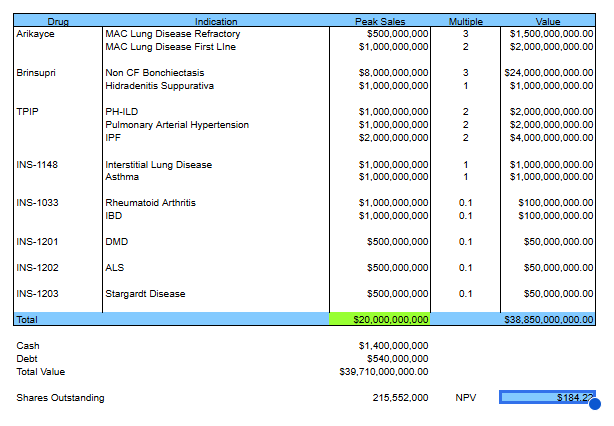

The #SynBio Report

I am going to build this thread as I go. There are not a lot of companies in the Synthetic Biology space yet. It is good to get up to date with them before new ones come into the space.

I am going to build this thread as I go. There are not a lot of companies in the Synthetic Biology space yet. It is good to get up to date with them before new ones come into the space.

1/ Gingko Bioworks $DNA

I think this is the top Synthetic Biology company working on 2 platforms. The first is #Biosercurity. This was born form the Covid pandemic and is one of the most important issues of our time.

I think this is the top Synthetic Biology company working on 2 platforms. The first is #Biosercurity. This was born form the Covid pandemic and is one of the most important issues of our time.

2/ The Covid pandemic has shown us how woefully unprepared we are for the next pandemic. We live in the age where anyone can create a bioweapon that could wipe out half the world. Biosecurity is the biggest new area of national defense.

3/ This space will be one of the biggest areas of the next decade. The other platform they have is #SynBio. They have a codebase which is all the genomic and chemistry data they have developed on engineering organisms.

4/ The other part of #SynBio is the Foundry. This is where they actually engineer the organisms. They are focused on horizontal development. They only design the organisms and pass them on to the customer. They are paid for a service when designing these organisms.

5/ They will get downstream value from the programs they develop. Some will give them equity stakes while other partners will give them milestones and royalties. This will slowly build long term value as each of these many programs goes commercial.

6/ They have sales run rate of about $400 million as growing foundry revenues will be offset by shrinking biosecurity revenues. The big benefit of Covid is expected to fade out as they work on building long term biosecurity products.

7/ The company trades at $5 billion market cap. They have $400 million sales and $1.4 billion in cash as of Q2. They trade at a reasonable valuation for their level of growth. They have one of the largest potential markets for any company in biotech.

8/ The applications are using organisms to solve some of the worlds most complex issues like carbon dioxide, pollution, food and manufacturing. That makes this one of the most promising companies for the future.

9/ Twist Biosciences $TWST

This is the second company in the #SynBio space. They actually have 4 different platforms which covers many of the super cool buzzwords for futuristic tech. They have a commercial program for synthesizing DNA. They are partnered with $DNA.

This is the second company in the #SynBio space. They actually have 4 different platforms which covers many of the super cool buzzwords for futuristic tech. They have a commercial program for synthesizing DNA. They are partnered with $DNA.

10/ They have a very successful commercial platform around selling DNA. This is not a huge money maker running about $100 million a year in sales. This is their #Synbio platform. The next platform they have is for building test kits for #Sequencing.

11/ They have a very successful test kit business where they make kits that are very efficient. They have multiple partnerships here with $NVTA and $PACB. Their 3rd platform is still in early stages. They are developing a system of DNA as data storage.

12/ This is where they turn 0's and 1's into A's, T's, G's and C's. This allows them to store huge volumes of data into a molecule smaller than the eye can see. This falls into the #TechBio space. It is not commercial yet, but could dive large future value.

13/ The last platform is using their expertise in DNA sequencing to build a clinical development platform to help other companies design and develop antibodies. They are doing all of this through various partnerships. They will get milestones and royalties on all these therapies.

14/ This could be a huge driver of future value. The company right now trades at only $1.7 billion valuation. They do about $250 million in annual sales. They have about $525 million in cash as of Q2. That leaves them trading at only $1.2 billion minus cash.

15/ This company has a ton of potential in the future for trading at only 5x sales on an ex-cash basis. The biggest drivers will be the new areas around DNA storage and antibody development.

16/ Amyris $AMRS

I am going to prefix this company with a dire warning. This company is in very high risk of bankruptcy based on their financials. They have about $110 million cash. They still burn over $150 million a year. They have declining sales and near $700 million debt.

I am going to prefix this company with a dire warning. This company is in very high risk of bankruptcy based on their financials. They have about $110 million cash. They still burn over $150 million a year. They have declining sales and near $700 million debt.

17/ I do not think this company is buyable at any cost. They do have a end to end strategy to #SynBio. They discovery new products in their lab and develop them. Then try to develop products with what they discover.

18/ This end to end strategy has many weaknesses. First they start with discovery of a product then try to build a market for it. This is the opposite of letting demand decide what gets made.

19/ The second major challenge is it requires a management team that can master every aspect of the business from science in the lab all the way across production and into sales. No management is that good and it has shown.

20/ This company might look cheap for its valuation with over $300 million a year in sales, but their balance sheet is exhausted with high debt, low cash and high cash burn. This becomes a cautionary tale of how important business model plays in success.

21/ Codexis $CDXS

This is a small company focused on enzymes. They have a fairly cheap valuation with $396 million market cap. The company has $108 million in cash and over $135 million in annual sales. They burn about $35 million a year so they are close to profitable.

This is a small company focused on enzymes. They have a fairly cheap valuation with $396 million market cap. The company has $108 million in cash and over $135 million in annual sales. They burn about $35 million a year so they are close to profitable.

22/ This seems like a very cheap company, but a large majority of their sales comes from a single supplier with Pfizer and the enzyme for Paxlovid. These sales are expected to decline. I don't think they have enough going on to replace all those sales when they do.

23/ The CEO recently departed and the new CEO sounds like he is focused on a turn around. This is another high risk turn around story. The one thing I am sure about is there will never be a block buster enzyme out there which makes the potential of this company small.

24/ They have a Codevolver database for designing and developing high performance enzymes for all applications. That makes them an interesting play on Synthetic Biology, but their potential is not there. I have owned them for a while, but I faded some of my position.

25/ Synlogic Therapeutics $SYBX

I will prefix this is a very speculative company that trades for just $.75. They are literally a penny stock, but they are doing something that is exciting. They are creating non replicating probiotics that produce a therapeutics.

I will prefix this is a very speculative company that trades for just $.75. They are literally a penny stock, but they are doing something that is exciting. They are creating non replicating probiotics that produce a therapeutics.

26/ This is very interesting, but still very early and much could go wrong. When it comes to a risky company like this. My rule is, "If you really like it, throw in a few bucks and see what happens". Some of these companies should be treated like a lottery ticket.

27/ As long as you know the risk going in. Chances are you will probably lose that money because the science is very risky for biotech. Nothing personal toward this specific company because I find what they are trying to do very exciting.

28/ The last thing I want to cover for #SynBio is a new conference. For many years, I have been a super nerd for science conferences like AACR, ASGCT, ASCO, ASH, SITC, and EHA. Now I would like to add a new very cool conference called the #SynBioBeta conference.

29/ On their conference website @ synbiobeta.com They have a huge collection of articles and videos you can dig into and learn a ton about Synthetic Biology. I plan to spend many hours absorbing all this knowledge.

• • •

Missing some Tweet in this thread? You can try to

force a refresh