Combining investing experience, data driven strategy and AI to invest. All opinions are my own. I post my reseach and ideas. Please do your own research.

May 11 • 6 tweets • 6 min read

My Strategy:

I spent the weekend going over companies with one question in mind. "Is this s wonderful business at a wonderful price I want to hold for 10 years?" Here are my results.

Biotech:

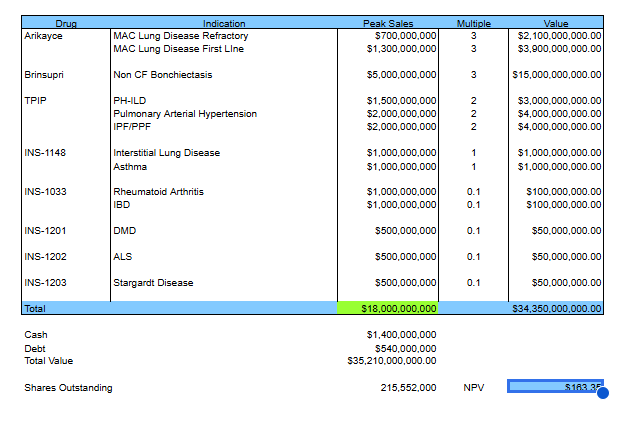

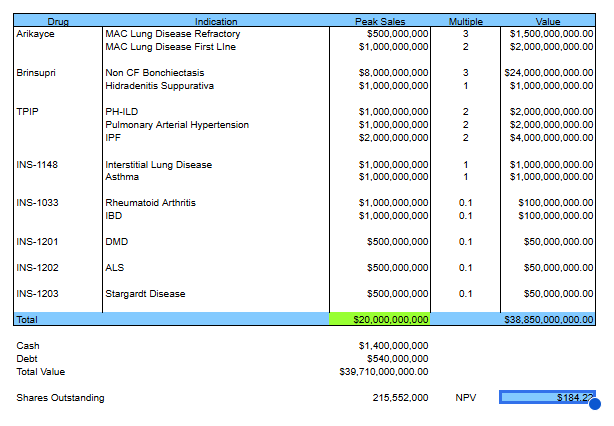

$INSM - A wonderful business that can do over $10 billion revenues at a wonderful price as its worth $150 minimum. I am a buyer and holder for as long as it remains wonderful.

$BBIO - A good business because it has a wonderful pipeline with 4 late stage drugs. The big issue is their massive debt. If anything goes wrong, that debt could be a big problem. It does trade at a wonderful price as I think its worth at least $100. I will hold it as long as things go well with drug launches and sales. If anything goes wrong, I got to sell before the debt drags it down.

$IDYA - A wonderful business with late stage oncology drug and a broad pipeline of other early stage drugs. Its still early, but it does have a very cheap valuation with my value around $60. I will hold it as long as my thesis plays out with good data from more drugs.

$PRAX - A wonderful business with 4 late and mid stage drugs. They could be a very big company in Seizures and Epilepsies in a few years. They also trade at a massive discount to their valuation. I think its worth at least $550. I will hold it for as long as my thesis continues to play out.

$IMNM - A great business at a decent price. The company has 1 late stage drug and several early stage drugs. Its only decently valued with my value around $26. If anything goes wrong, this get sold.

I have 2 companies on my watch list in biotech. They are wonderful businesses, but they are a bit expensive for my taste. One of them is close to a buy if it pulls back, but the other needs a strong correction to be worth buying.

May 6 • 6 tweets • 2 min read

My Top 5 Biotech:

I am putting out these reports because its my plan to sell all biotech but these 5. I might sell even these 5 if the sector gets crazy enough. I was 90% cash in 2021 and I don't mind going to 90% or more cash again.

$INSM:

Apr 13 • 11 tweets • 28 min read

My Fintech Framework:

I built a framework to take my 30 years of experience at picking companies and turn it into a framework I could use with AI. This is just my DD. Please do your own.

Tech Framework:

Attribution: I built this framework using Microsoft Copilot while doing 3 AI prompting certificated from Google, IBM and Vanderbilt. I have used it with many AI agent effectively.

Fintech Framework

FINTECH INVESTMENT FRAMEWORK

Version 2.0 — Full System (Fundamental Score + Value Score + Red Flags + Competitive Landscape)

Total Structure: 0–10 Fundamental Score + 0–10 Value Score

I. FUNDAMENTAL SCORE (0–10 Points)

Each category uses a 0–2 or 0–1 scoring band.

Total possible = 10 points.

3. Profitability (0–2 points)

Measures: Unit economics, operating leverage, and earnings quality.

0 points: No path to profitability within 24 months

1 point: Clear path to profitability within 12–24 months

2 points: Already profitable with expanding margins

4. Competitive Advantage / Moat (0–1 point)

Measures: Structural defensibility.

0 points: Weak or no moat

1 point: Strong moat (network effects, switching costs, data advantage, regulatory advantage, ecosystem lock-in)

5. TAM (0–1 point)

Measures: Realistic economic TAM, not headline TAM.

0 points: < $1B

1 point: ≥ $1B

6. Management (0–2 point)

Measures: Management Quality

0 points: Credibility issues; poor governance; repeated execution failures.

1 point: Mixed track record; some execution gaps but generally competent.

2 points: Proven operators; strong capital allocation; transparent communication; consistent execution.

Fundamental Score Interpretation:

8–10: Category-defining, elite, investable

6–7: Solid, investable with conditions

4–5: Watchlist only

0–3: Avoid

II. VALUE SCORE (0–10 Points)

Direct translation of the biotech Value Score into business fundamentals.

1. Economic TAM (0–2 points)

Measures: Realistic revenue opportunity after adjusting for penetration, pricing, competition, and regulation.

0 points: Small or structurally constrained TAM

1 point: Good TAM with moderate runway

2 points: Massive, expanding TAM with long-term compounding potential

Any major red flag can override both scores and move a company to Avoid.

A. Business Model Red Flags

Structurally negative unit economics

CAC rising faster than LTV

High churn masked by aggressive acquisition

Overreliance on one product or customer

No pricing power

B. Financial Red Flags

Heavy dilution

Unsustainable debt

Low-quality revenue (one-time, non-recurring)

Aggressive accounting practices

C. Regulatory Red Flags (Fintech-Specific)

Capital adequacy issues

Regulatory investigations

Fraud exposure

Compliance failures

High credit risk without proper reserves

D. Competitive Red Flags

No moat

Race-to-the-bottom pricing

Entrants with superior economics

Losing share in a growing market

E. Management Red Flags

Overpromising

Inconsistent guidance

Poor capital allocation

Hype-driven communication

IV. COMPETITIVE LANDSCAPE ANALYSIS

Contextual layer to interpret scores.

1. Category Position

Leader

Challenger

Niche

Commodity

2. Moat Type

Network effects

Switching costs

Data advantage

Regulatory advantage

Brand trust

Ecosystem lock-in

Its my desire to build a master thread and then put it on my highlights for sharing my 30 years of investing research framework for Biotech companies. I consider Fundamentals tell me what to buy. Its a measure on company quality. Valuation tells me when I should buy. It tells me If I am overpaying or getting a bargain on buying any company. Combining fundamentals, valuation and patience has done very well for me in investing for many years. I am sharing this to give you my framework so that it may inspire you in building your own framework.

The Fundamental Framework:

Fundamental Score (0–10): Full Criteria

A 6‑category rubric, with 4 categories scored 0–2 and 2 categories scored 0–1, for a maximum of 10 points.

1. Science & Platform Strength (0–2)

2 points — Strongly differentiated science; validated or de‑risked mechanism; platform can generate multiple assets. Think RNAi or ADC like technologies that lead to multiple big drugs.

1 point — Plausible, partially validated science; some differentiation; platform potential but unproven. Think one hit wonders or early stage concept companies with unvalidated technology.

0 points — Weak or non‑differentiated mechanism; unclear biology; no platform leverage.

2. Pipeline Depth & Breadth (0–2)

2 points — Multiple credible shots on goal; diversified by indication, modality, or stage; clear sequencing strategy.

1 point — Some pipeline depth but concentrated risk; limited diversification.

2 points — Strong, consistent, statistically meaningful efficacy and safety; reproducible across cohorts or studies. Best in Class data, First in Class mechanism or Breakthrough Therapy is a strong sign.

1 point — Early or mixed data; promising signals but not yet robust.

0 — Weak, inconsistent, negative, or unsafe data.

4. Management Quality & Execution (0–2)

Follow what they promise and then what they actually deliver. Take notes on calls and make sure they live up to what they promise.

1 point — Realistic economic TAM ≥ $1B for the company’s actual monetizable opportunity (pricing, reimbursement, share, duration, competition). Make sure to consider partners take.

0 points — Economic TAM < $1B or structurally constrained.

6. Cash Runway & Balance Sheet (0–1)

1 point — At least 2 years of cash runway at current or reasonably projected burn; low near‑term dilution risk.

0 points — <2 years runway or high likelihood of near‑term, punitive financing.

May 30, 2025 • 7 tweets • 5 min read

🧵 $VKTX Profile:

This is my updated profile for Viking. They are 1 of my 5 Innovators. They are in the mid stage and moving into later stages of development. They have some validation, but still a long way to get across that finish line.

Management:

Intro to Management:

I have been following this company on and off for several years, so I know the management well. So far, I had time to catch up on the company by listening to several of their webcasts and presentations over the last few months. I have been impressed with their management team thus far. There are a few key areas of business that I think a management team has to demonstrate expertise in to build a long term winning biotech company.

Clinical Development:

They need expertise at advancing drugs through the clinical development process. So far, the company has advanced two programs through the end of phase 2 with MASH and Obesity. That shows they have some ability to move through clinical development but still have a way to go before reaching successful approval. They should be starting a phase 3 soon for the subcutaneous injection in obesity in Q2 of 2025. The oral phase 2 study should start in second half of 2025.

Regulatory Development:

They need expertise at navigating the regulatory process with the FDA. So far, they haven't had to deal much with the FDA. They are just starting phase 3. It will take some time before they get to that point. We will have to wait and see how it goes.

Managing Balance Sheet:

They need expertise at managing the balance sheet. They have $853 million in cash and no debt. They burned about $52 million in their Q1 quarter. Their costs will ramp as they advance into phase 3. They just signed a deal for manufacturing which included $150 million over the next 3 years. They also started a buyback for $250 million. I don't think that is a wise choice when they need cash to run phase 3 trials and build a commercial sales team. I am watching their cash flow statements, and I have not seen any buying of their stock yet. I think they know better.

Commercial Sales:

The final key expertise for a management team is the ability to build a successful commercial sales team. So far, they have no commercial products, and they are still quite a way from being commercial. We will have to see if they decide to partner or go it alone with commercial sales.

Apr 21, 2025 • 5 tweets • 2 min read

Over the weekend, I spent a ton of time picking through the $NBI and $ARKG looking for ideas. I shared my comments on many, but not all the companies I looked at. Here is a list of links to those threads.

$NBI part 1:

They have 35 holdings in the $ARKG and I am going to look at them all and give you my opinion.

$TWST is a DNA company that makes and sell DNA sequences to biotech companies. I don't see them becoming a very huge company. I think the potential is actually small. One of the reasons I sold them when I really got to know the company.

Apr 12, 2025 • 7 tweets • 2 min read

There was a lot of hype over the FDA announcement for replacing animal testing with AI modeling over time. A lot of the companies in the TechBio space rocketed higher yesterday. The market is not smart enough to know the winners and losers. It paints with a broad brush. My plan over the coming weeks it does dig into these TechBio companies. This has been a major theme of mine for years now. With all my study of the space, I will be able to help you sort the winners from the pack.

Here is the link to the FDA announcement where they are going to replace animal testing with alternatives over time. That is right. The huge pop in the TechBio names seems to be very premature. Nothing it going to change right away.

I know in a market that is super bubbly with the indexes trading at over 27x earnings many investors are wondering where to put their money. I know I have been looking and searching for value of any kind in this market.

1/ #Tech is a very big space, but there are some key themes here I am focused on as I think they are still innovative and disruptive. They are #Cloud, #Cybersecturity and #Automation.

Jun 19, 2024 • 21 tweets • 4 min read

🧵Innovation: (Part 2)

I know in a market that is super bubbly with the indexes trading at over 27x earnings many investors are wondering where to put their money. I know I have been looking and searching for value of any kind in this market.

1/ The next major theme is Financial Technology called #FinTech. This has been very disruptive to the old school financial industry which has been very complicated and unfriendly to consumers for many decades. I know last year I abandoned my obsolete old bank for fintech.

Jun 19, 2024 • 21 tweets • 4 min read

🧵Innovation: (Part 1)

I know in a market that is super bubbly with the indexes trading at over 27x earnings many investors are wondering where to put their money. I know I have been looking and searching for value of any kind in this market.

1/ I have been an innovation investor for many years. I put out a thread a few years ago about my thematic investing style. Some of my top themes at the time where #AI, #Automation, #Cybersecurity in Tech, #Fintech, #TechBio and #CRISPR in Biotech.

Apr 27, 2024 • 14 tweets • 3 min read

🧵Looking at $RXRX Platform:

Here I am going to look at the platform for @RecursionPharma and attempt to value this company as a sum of the parts.

1/ The Recursion platform comes in the technology pieces. They are the Data Collection, Mapping and Machine Learning. I will look at each of these parts.

Apr 18, 2024 • 15 tweets • 3 min read

The Biotech Report:

This covers all my companies since my last report in March. I will cover my 3 new companies here too.

$RXRX

This is going to be for companies not inside the $XBI. I will post companies here as I come across biotech names and check them out.

$ABSI is a company using synthetic biology to create antibodies and AI to model and design antibodies. They are working on generative AI platform to allow for antibody development. Its a massive bubble at 2x valuation. I love it at the right price.

Apr 13, 2024 • 34 tweets • 5 min read

🧵The Little Book of Biotech: Part 4

This is going to be part 4 as I ran into the thread limit for the number of companies each thread will show. Make sure to go back and check out Part 1, Part 2, and Part 3.

$FATE is a iPSC cell company working on CAR-NK and CAR-T therapies. I have owned them for many years, but opted to sell them recently as they have failed over and over again in the last several years. Time to move on.

Apr 11, 2024 • 32 tweets • 6 min read

🧵The Little Book of Biotech: Part 3

This is going to be part 3 as I ran into the thread limit for the number of companies each thread will show. Make sure to go back and check out Part 1 and Part 2.

$RXRX is actually my top pick right now. They are using robotics to do experiments and collect data to feed into their super computer and use AI to develop drugs. This is the future of drug discovery. It should, over time, reduce costs and improve rates of success.

Apr 9, 2024 • 25 tweets • 5 min read

🧵The Little Book of Biotech: Part 2

This is going to be part 2 as I ran into the thread limit for the first set of companies. Don't forget to look at my first 30 companies.

$FOLD is an old ERT company working in rare diseases which changed into gene therapies. I use to own them for a while so I know they have had some success and some failure along the way. Its a solid company, but I am moving beyond gene therapy to gene editing now.

Apr 7, 2024 • 32 tweets • 6 min read

🧵The Little Book of Biotech:

I plan to go through every company in the $XBI and do my DD. Then leave a post in this thread for my quick take on each company. Make sure you book mark this thread. I will start building it today and try to add every day at least 1 company.

$CYTK is a company working in muscle biology starting with heart indications. They have 3 late stage indications and a few early stage indications. They have about $700 million cash and burn about $450 million. Very impressive company on 1st look. Added to my list to advance.

Mar 28, 2024 • 12 tweets • 2 min read

My Top 10 Ideas

This is updated since earnings.

#1 $RXRX is still my top pick. They blend AI technology and biology to discovery drugs. They have a technology platform which could change the way we develop drugs. Its still very early, and it has to validate the platform works with human data.

Jan 20, 2024 • 23 tweets • 4 min read

🧵A lesson from the past:

I know no one wants to hear about bubbles popping, but you are gonna. I lived through many bubbles and I avoided all of them. I am going to tell you why because maybe it will save someone from the next bubble popping.

1/ I started out in the mid 1990's. I read all of Ben Graham's works and learned from him about the real science of fundamentals and valuation. I learned about buying great companies at a cheap price.

Jan 15, 2024 • 6 tweets • 1 min read

🧵The Biotech Report for $CRBU:

They did a press release along with a presentation for JPM. I was tempted to promote them above Gingko to my #2 position, but I am holding off.

I think they need data to show their version of immune evasion works. They are also solely focused on cell therapies with no other platform development. They are not doing any gene editing programs or regen medicine.