Some observations on China crude imports, storage levels and product consumption.

Short thread...

1/n

Short thread...

1/n

Basics first:

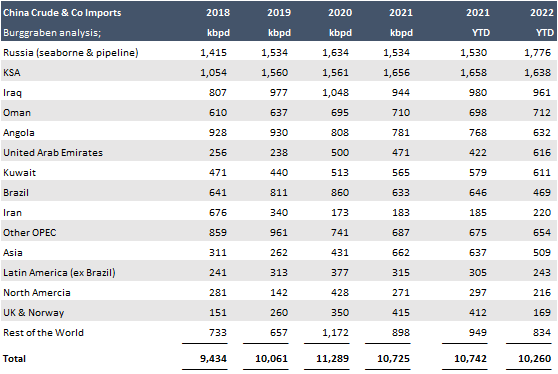

China's baseline crude imports are 10.5mbpd (pipe & seaborne).

It has an apparent consumption of up to 14.8mbpd which it satisfies from additional 4.1mbpd of its own production (on- and offshore) and storage (if need be).

2/n @kittysquiddy

China's baseline crude imports are 10.5mbpd (pipe & seaborne).

It has an apparent consumption of up to 14.8mbpd which it satisfies from additional 4.1mbpd of its own production (on- and offshore) and storage (if need be).

2/n @kittysquiddy

In 2020, China imported 11.3mbpd (1.2 more than 2019) to take advantage of distressed prices until storage went tank-top. That was "peak China".

YTD 2022, it's at 10.2mbpd, 0.5mbpd below 2021.

Note how it dropped EU crude to add 200kbpd Urals?

3/n

YTD 2022, it's at 10.2mbpd, 0.5mbpd below 2021.

Note how it dropped EU crude to add 200kbpd Urals?

3/n

So China loves cheaper but not more crude!

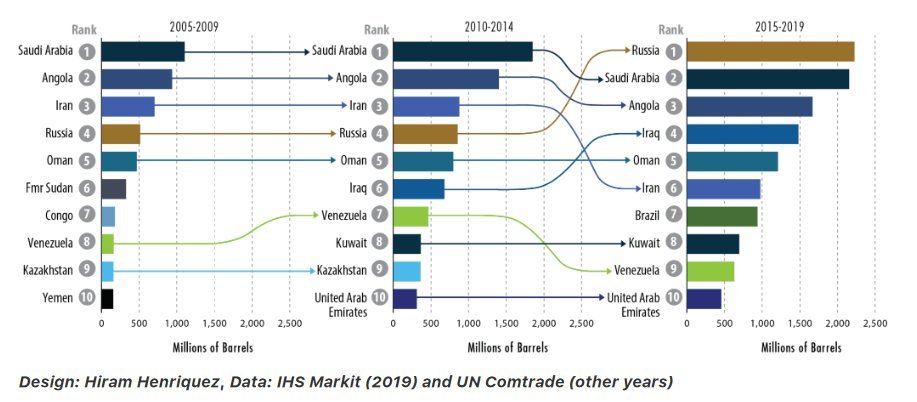

China's procurement strategy, dictated by a fine-tuned CCP quota system, is an intentional endeavor.

There’s a two-decade effort to diversify not just its oil import sources but also its trading routes to enhance energy security.

4/

China's procurement strategy, dictated by a fine-tuned CCP quota system, is an intentional endeavor.

There’s a two-decade effort to diversify not just its oil import sources but also its trading routes to enhance energy security.

4/

In that strategy, Russian imports are maxed out at or 20% of total imports but preferrably at 16%.

Evidence of that are RUS Oct imports, down 200kbpd & reversing elevated purchases bw April - Sept.

China however bought more KSA in Oct to match 2021. Relations matter!

5/n

Evidence of that are RUS Oct imports, down 200kbpd & reversing elevated purchases bw April - Sept.

China however bought more KSA in Oct to match 2021. Relations matter!

5/n

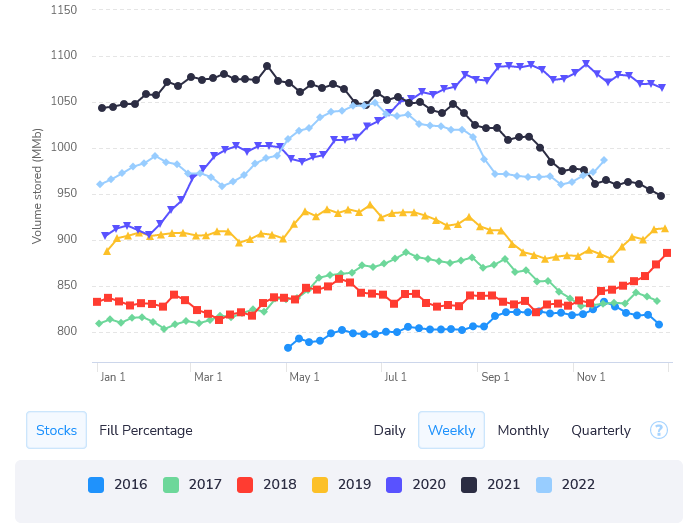

Can China buy more RUS crude to replenish SPRs?

Some, yes, but highly unlikely. More precisely, it could add 56mb to max out 403mb of SPR storage which is 86% full currently. That leaves aside crude quality needs, if any.

6/n Source: Kayrros

Some, yes, but highly unlikely. More precisely, it could add 56mb to max out 403mb of SPR storage which is 86% full currently. That leaves aside crude quality needs, if any.

6/n Source: Kayrros

There is more: China likes to negotiate for the right deal.

Think about that: The commercial negotiations for the ESPO oil pipeline contract took the 2 countries 15 years! Here some colour.

7/n

spglobal.com/commodityinsig…

Think about that: The commercial negotiations for the ESPO oil pipeline contract took the 2 countries 15 years! Here some colour.

7/n

spglobal.com/commodityinsig…

Meanwhile, China's storage is increasing again from elevated purchases in Sept, Oct & Nov while higher demand remains below such increased imports.

In case you haven't noticed: that is not bullish.

8/n Source: Kayrros

In case you haven't noticed: that is not bullish.

8/n Source: Kayrros

Nov consumption numbers are yet to arrive but higher real time imports & storage suggest runs were in line with 14.4mbpd in Sept to explain 1.2mbpd builds for past 3 weeks.

Did product stocks go down? Answer: IDK. Energy Aspects had them unchanged in Oct.

7/n

Did product stocks go down? Answer: IDK. Energy Aspects had them unchanged in Oct.

7/n

What is however noticable is that Q3 2022 refining margins were nil - that is gross margins!

That is the first time since we can measure it to see such depressed margins - not an incentive to push runs even in China's largely state-controlled context.

8/n

That is the first time since we can measure it to see such depressed margins - not an incentive to push runs even in China's largely state-controlled context.

8/n

Meanwhile, the rise in confirmed cases has now increased "Chinese oil demand at risk from lockdowns" to nearly 40% in mid-October (Figure 6).

That said, EA expect a slightly more permissive zero-Covid regime from November, comparable to June–August levels. Who knows.

9/n

That said, EA expect a slightly more permissive zero-Covid regime from November, comparable to June–August levels. Who knows.

9/n

More policy easing may be expected after the People's Congress in March, but even if Beijing begins to deploy more efficient vaccines (big if) by then, it will still require at 3 quarters to achieve a sufficient vaccination rate before a full reopening. Expect little.

10/n

10/n

So where I sit, China has 200kbpd room for higher jet consumption vs Sept in Q4 and otherwise this "reopening theatre" has played out and is priced in - at least on the crude import side that is..!

11/n Thx @UrbanKaoboy

11/n Thx @UrbanKaoboy

• • •

Missing some Tweet in this thread? You can try to

force a refresh