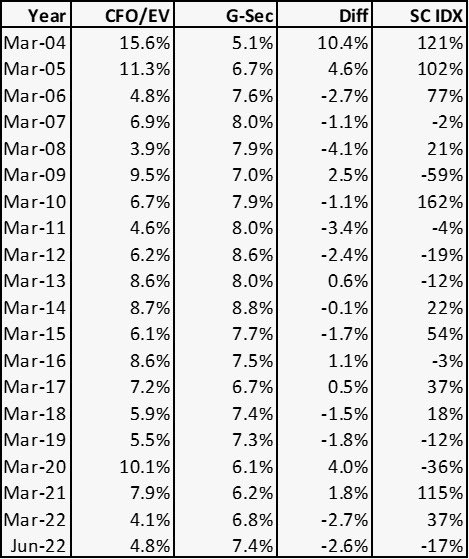

Some charts to help understand where each sector is at in terms of their aggregate profits and aggregate market cap. (1/9)

Starting with metals: does market know something that we don’t?

Starting with metals: does market know something that we don’t?

Healthcare: always bottoms when the line converges. So some more time before bottom?

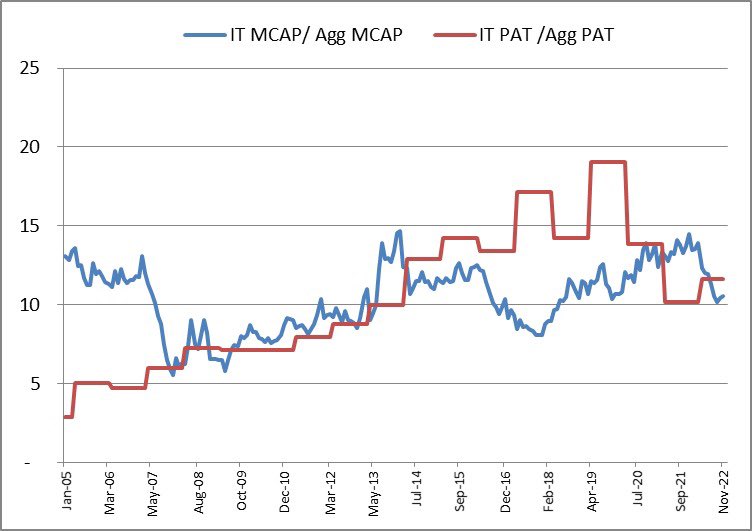

IT: bottom done? Possible accumulation phase now.

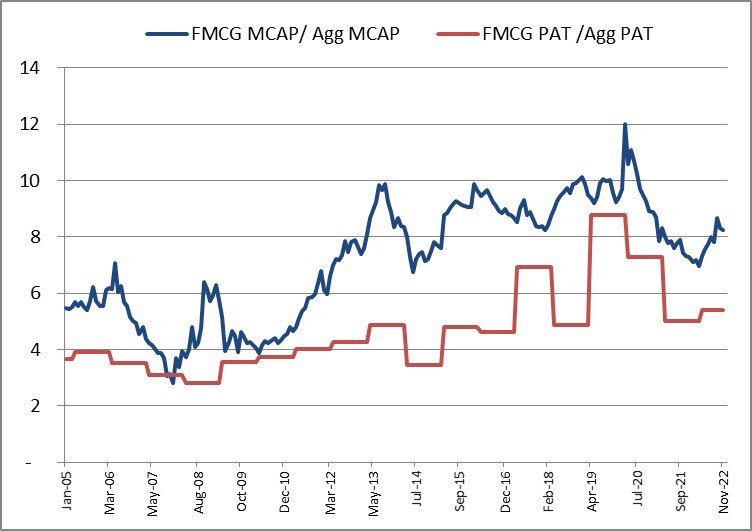

FMCG: Beginning of a new cycle?

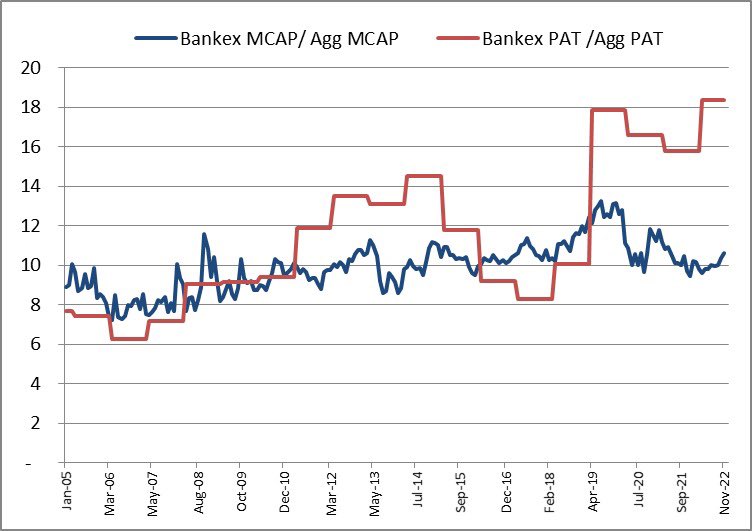

Banks: Undervalued?

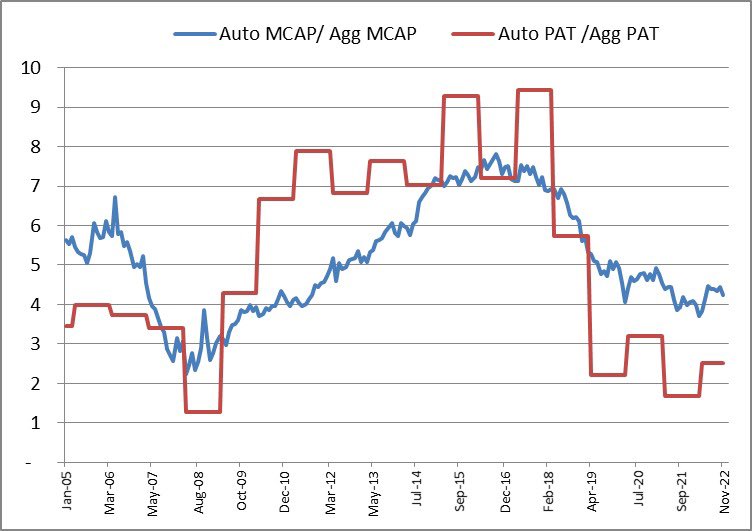

Auto: (perennial) dark horse?

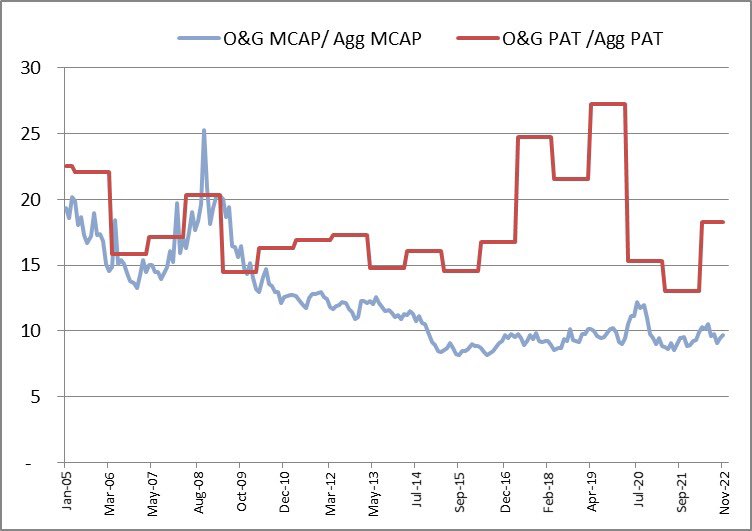

Oil & Gas: Lull continues

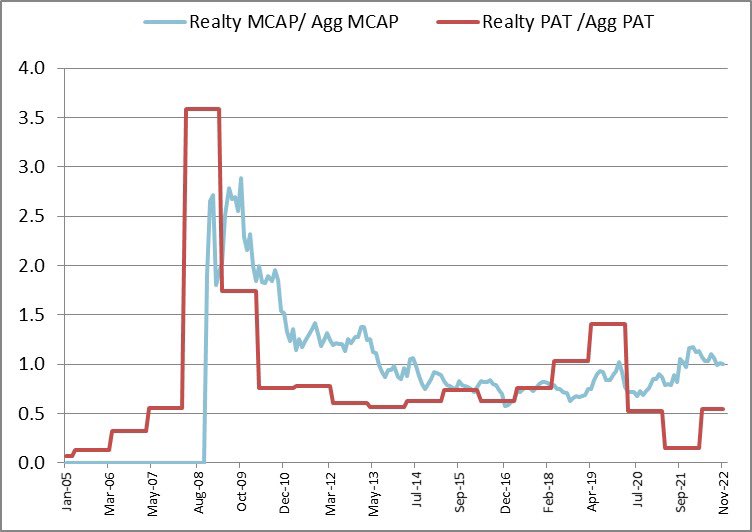

Realty: Nothing different

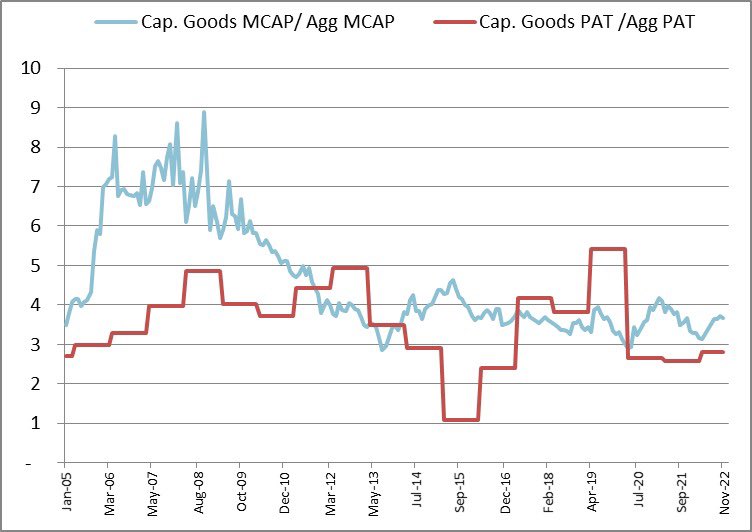

Cap goods: 2004 to 2007 like baby steps(s)?

• • •

Missing some Tweet in this thread? You can try to

force a refresh