Aaaaan we're live.

Trade the first expirables in #DeFi on contango.xyz

Code is unaudited. So before apeing in, maybe read a few notes below.

👇

Trade the first expirables in #DeFi on contango.xyz

Code is unaudited. So before apeing in, maybe read a few notes below.

👇

Contango's expirables are derivative instruments to buy or sell assets at a specific price and date in the future.

Read how they differ from futures and forwards: bit.ly/3UThLR4

Also, remember @FTX_Official? If you are looking for a DeFi alternative, we got you fam.

Read how they differ from futures and forwards: bit.ly/3UThLR4

Also, remember @FTX_Official? If you are looking for a DeFi alternative, we got you fam.

@FTX_Official We have a debt ceiling capped at 10k per pair, per currency, on the underlying fixed-rate market (@yield) so that you degens are not gonna degen too much. 🐒

Try the beta with small amounts & provide feedback on Discord or through this survey: bit.ly/3VQk4Wx

Try the beta with small amounts & provide feedback on Discord or through this survey: bit.ly/3VQk4Wx

@FTX_Official @yield What's this 10k debt ceiling thing?

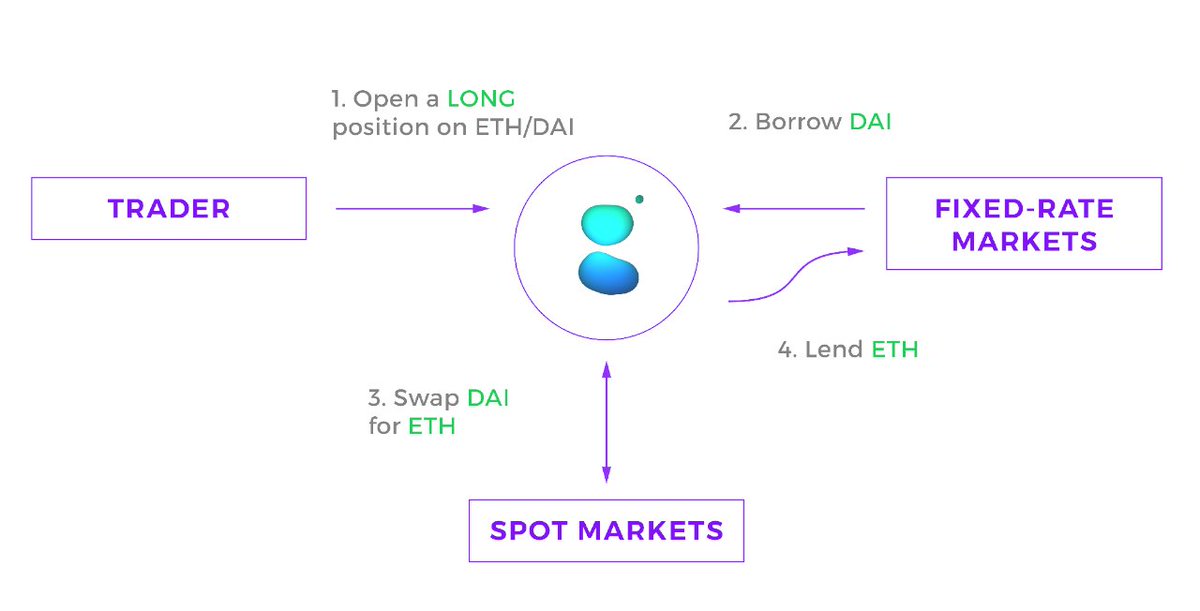

Basically, every time you open a position on Contango, you post some margin (collateral) and the missing capital is borrowed on the underlying fixed-rate market. That's your debt.

Basically, every time you open a position on Contango, you post some margin (collateral) and the missing capital is borrowed on the underlying fixed-rate market. That's your debt.

@FTX_Official @yield On Contango right now you can go long/short on:

1️⃣ ETHUSDC

2️⃣ ETHDAI

3️⃣ DAIUSDC

And you can choose between 2 maturities:

📆 December 22

📆 March 23

1️⃣ ETHUSDC

2️⃣ ETHDAI

3️⃣ DAIUSDC

And you can choose between 2 maturities:

📆 December 22

📆 March 23

@FTX_Official @yield So, for instance, on the ETH/USDC pair, Contango can only borrow as much as 10k of ETH and 10k of USDC on @yield (so 20k per pair).

Since 3 pairs and 2 maturities are available, the total debt ceiling is:

$20k * 3 * 2 = $120k

Since 3 pairs and 2 maturities are available, the total debt ceiling is:

$20k * 3 * 2 = $120k

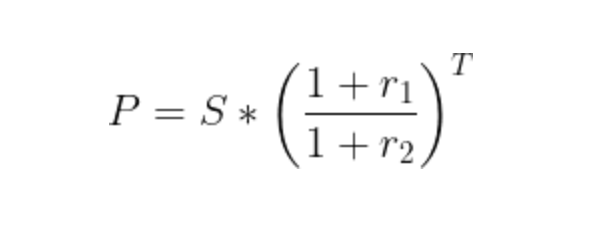

@FTX_Official @yield Remember that Contango's pricing mechanism uses:

1) interest rates from a fixed-rate market (now @yield, soon @NotionalFinance)

2) spot prices (@Uniswap)

Consider this when assessing smart-contract risk.

1) interest rates from a fixed-rate market (now @yield, soon @NotionalFinance)

2) spot prices (@Uniswap)

Consider this when assessing smart-contract risk.

@FTX_Official @yield @NotionalFinance @Uniswap Depending on the side you take on e.g. ETHUSDC, you'll post collateral:

- in USDC if you're going long

- in ETH if you're going short

Confused? Read this: bit.ly/3FwwlZ3

- in USDC if you're going long

- in ETH if you're going short

Confused? Read this: bit.ly/3FwwlZ3

@FTX_Official @yield @NotionalFinance @Uniswap We currently provide 3.5x leverage on ETH pairs, and 10x leverage on stable vs stable pairs.

Always monitor your margin & liquidation price: if your collateral loses value, top up or reduce position size.

Liquidations are carried out by the underlying fixed-rate markets.

Always monitor your margin & liquidation price: if your collateral loses value, top up or reduce position size.

Liquidations are carried out by the underlying fixed-rate markets.

@FTX_Official @yield @NotionalFinance @Uniswap What can you use Contango for?

1️⃣ trade expirable contracts on-chain (goodbye CeFi 👋)

2️⃣ arb prices between CeFi and DeFi

3️⃣ arb stable vs stable pairs with 10x leverage

4️⃣ arb interest rates on different chains & protocols (coming soon)

1️⃣ trade expirable contracts on-chain (goodbye CeFi 👋)

2️⃣ arb prices between CeFi and DeFi

3️⃣ arb stable vs stable pairs with 10x leverage

4️⃣ arb interest rates on different chains & protocols (coming soon)

@FTX_Official @yield @NotionalFinance @Uniswap Oh, almost forgot: trading fees are set to 0.

Read that again.

Yes, we’re not charging you anything to trade on Contango (you’re welcome).

Read that again.

Yes, we’re not charging you anything to trade on Contango (you’re welcome).

@FTX_Official @yield @NotionalFinance @Uniswap We'll soon launch on L1. We're working closely with @yield to deploy these new contracts. This way you'll have an expirable quoted on 2 different chains, arbitrum and mainnet. Price differences = arb opportunity.

@FTX_Official @yield @NotionalFinance @Uniswap Indeed we expect Contango to help bring rates into equilibrium across different chains and protocols.

We also expect Contango to bring alignment between CeFi and DeFi rates.

We also expect Contango to bring alignment between CeFi and DeFi rates.

For now, expect price differences between Contango and major CeFi futures venues like @binance. But that's good news, it's an arb opportunity.

Excited? Go try the beta and RT/like our first tweet 👇

Excited? Go try the beta and RT/like our first tweet 👇

https://twitter.com/Contango_xyz/status/1603383689475399689

• • •

Missing some Tweet in this thread? You can try to

force a refresh