#MMT versus Reality

1. The main #MMT talking point these days is that high inflation doesn't discredit #MMT, because #MMT never said inflation wouldn't go up. That shows how detached the #MMT crew is from reality, as this year's death of #MMT has little to do with inflation...

1. The main #MMT talking point these days is that high inflation doesn't discredit #MMT, because #MMT never said inflation wouldn't go up. That shows how detached the #MMT crew is from reality, as this year's death of #MMT has little to do with inflation...

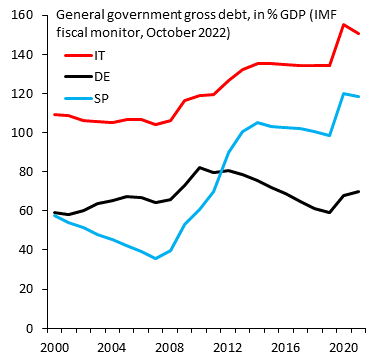

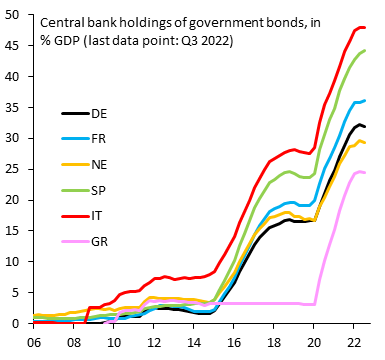

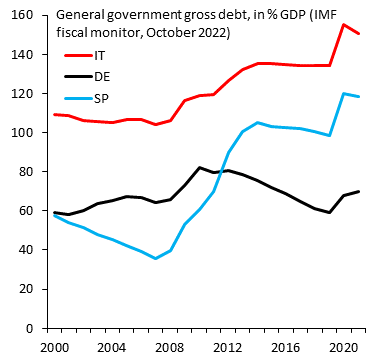

2. One example is Japan, which still has no inflation to speak of. The Yen went into a devaluation spiral mid-2022 anyway, because high debt forced the BoJ to keep interest rates low, sending the Yen weaker as global yields rose. High debt is a problem even with low inflation...

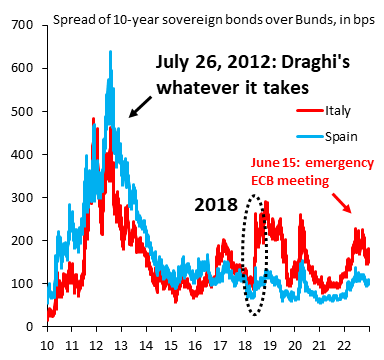

3. The UK bond market blow-up in September is another example. UK inflation wasn't materially higher than in other advanced economies. What caused the Gilt market blow-up was a poorly articulated fiscal expansion that was debt financed. Again, it wasn't about inflation...

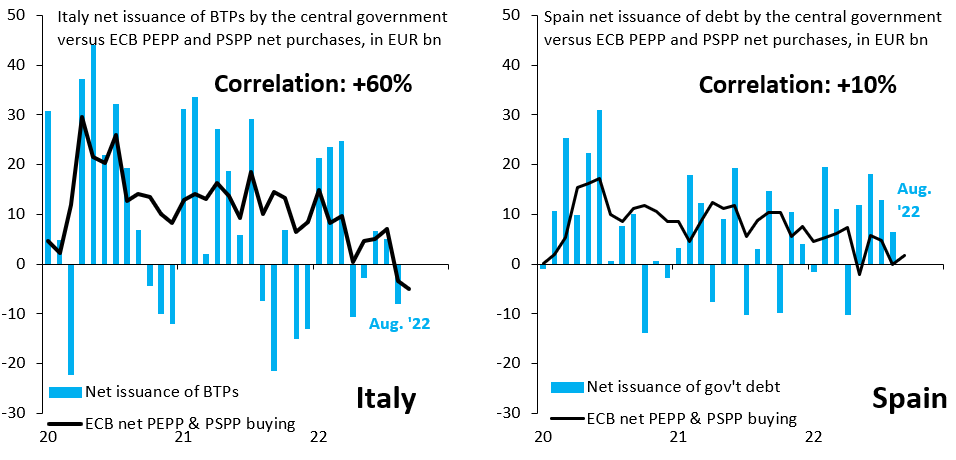

4. Where the #MMT crew gets dangerous is that it dismisses data points unfavorable to its US story. It does this by saying: "The US is special." We are NOT special. The US had a massive bond market tantrum in early 2020 that required huge Fed emergency QE to calm things down...

5. #MMT died in 2022. That's not about inflation. Instead, it's about markets sending many reminders that fiscal space is finite and that - if you do reckless debt run-ups - things can spiral out of control. Every EM economist knows this. The G10 #MMT crew now gets to relearn it.

• • •

Missing some Tweet in this thread? You can try to

force a refresh