Is the European energy shock over?

1. The Euro (black) is back to pre-war levels and common measures for the Euro zone terms-of-trade - the ratio of export to import prices - have also risen lots (blue). Many are using this to claim the energy shock is over, but that's WRONG...

1. The Euro (black) is back to pre-war levels and common measures for the Euro zone terms-of-trade - the ratio of export to import prices - have also risen lots (blue). Many are using this to claim the energy shock is over, but that's WRONG...

2. To start with, while gas prices in Europe have fallen from insane levels in Aug. '22, they're hugely above pre-COVID levels. Spot (black) and one-year ahead TTF gas prices (blue) are 260% above 2018-2019 averages. The hit to European - and German - competitiveness is HUGE!

3. How come gas prices fell?. Putin turning off Nordstream shifted the supply curve to the left from S to S'. Prices rose and consumption fell. The economy shifted away from gas to coal, moving demand from D to D'. Gas prices fell, but the hit to profits & demand is still there.

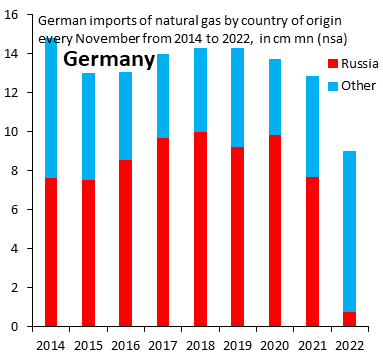

4. Falling gas prices are wrongly seen as a signal the energy shock ended. That'd only be true if the supply curve shifted back to the right from S' to S. We know that's NOT the case. Imports of gas by Germany are down -40% from 2019 levels. The shock is massive and ongoing...

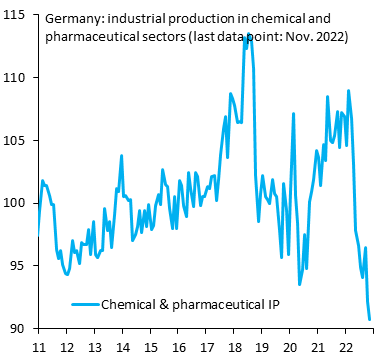

5. German industry is undergoing a massive shift and retooling. Whole sectors of production have become unprofitable and certain product lines have been shut down, never to reopen. Chemicals and pharmaceuticals are the prime example. Output is down -15% from a year ago...

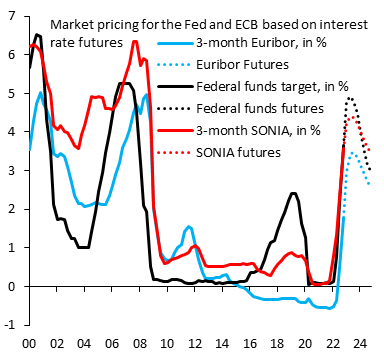

6. Lots of policy and market implications. The shift to the left of the supply curve is NOT inflationary but deflationary, since it's a hit to output that will bring recession. ECB hikes are hard to justify, which is why markets price cuts further out the money market curve...

7. Of course, there is the important matter that Europe did NOT go into recession in 2022, something I had forecast. The fact that Europe dodged recession was mostly due to one-offs like a rebound in auto & chip production that will fade. See this thread.

https://twitter.com/RobinBrooksIIF/status/1613129410873270272

8. As far as the Euro goes, markets currently give the wrong interpretation to the fall in gas prices. First, prices are still super high. Second, they've fallen as demand and activity are getting crushed. Fair value of the Euro is down massively. Our estimate is EUR/$ at 0.9...

• • •

Missing some Tweet in this thread? You can try to

force a refresh