#EKIEnergy

#Redflag

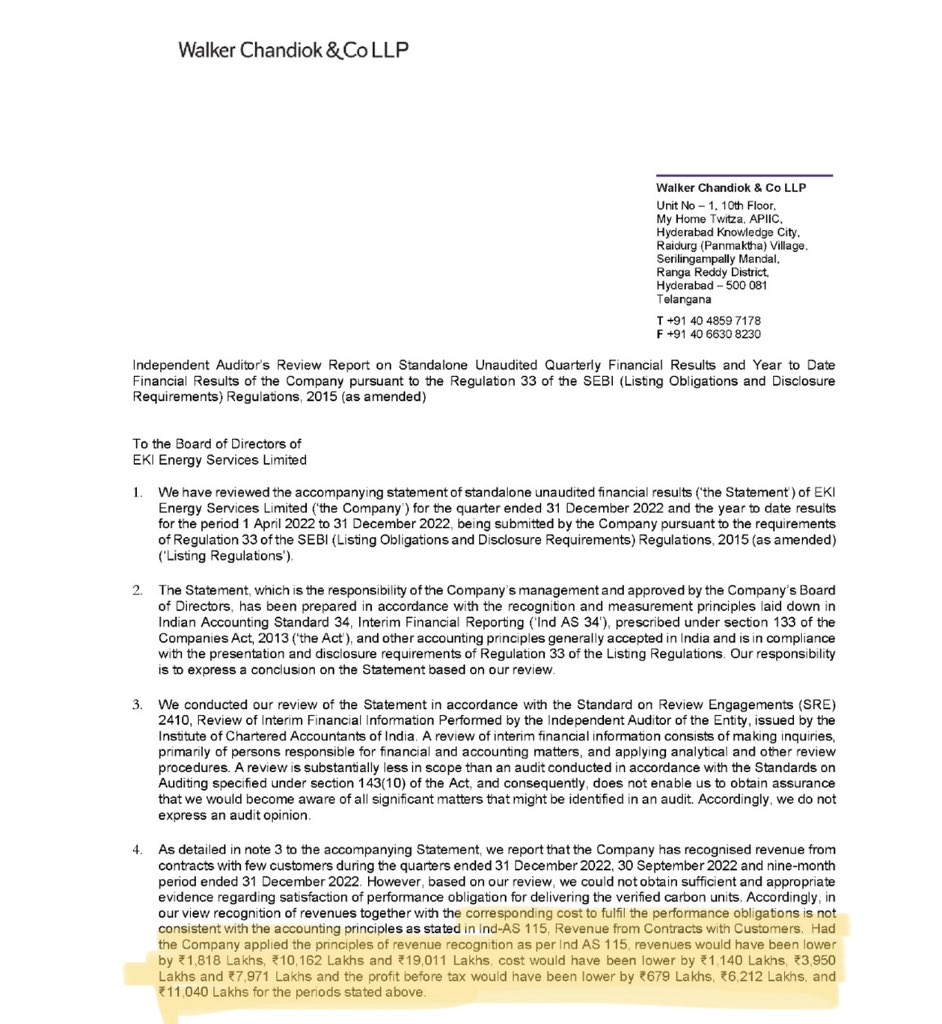

The latest Q3 Results of EKI Energy has uncovered a dark truth : non-compliance with IndAS 115, Revenue Recognition.

Auditor Walker Chandiok (Grant Thornton) today issued a qualified report.

Is this just the tip of the iceberg?

Like & share for max reach!

#Redflag

The latest Q3 Results of EKI Energy has uncovered a dark truth : non-compliance with IndAS 115, Revenue Recognition.

Auditor Walker Chandiok (Grant Thornton) today issued a qualified report.

Is this just the tip of the iceberg?

Like & share for max reach!

Reported Figures for 9M-

Revenue - 1384 Cr

PBT - 347 Cr

PAT - 260 Cr

As per Auditor -

Revenue - 1194 Cr (-14%)

PBT - 237 Cr (-32%)

PAT - 177 Cr (-32%)

Generally company also have Concall post results,this time there is no mention of concall.

Revenue - 1384 Cr

PBT - 347 Cr

PAT - 260 Cr

As per Auditor -

Revenue - 1194 Cr (-14%)

PBT - 237 Cr (-32%)

PAT - 177 Cr (-32%)

Generally company also have Concall post results,this time there is no mention of concall.

Dark clouds of doubt now loom over the previous auditor D.N. Jhamb, who issued unqualified report in Sep-22, and resigned on 8-Dec-22 citing reasons of pre-occupation.

Now the bigger question is whether revenue recognised in earlier years are as per IndAS requirements or not?

Now the bigger question is whether revenue recognised in earlier years are as per IndAS requirements or not?

More interestingly - In 4-Nov-20, just before there IPO, Anmol Bohra & Co also resigned as Auditor citing the same reason of pre-occupation.

Last 4 year Auditors & Audit Fees -

FY19 0.25 Lakhs - Anmol Bohra

FY20 0.28 Lakhs - Anmol Bohra

FY21 1.90 Lakhs - D.N. Jhamb

FY22 7.22 Lakhs - D.N. Jhamb

Now Walker Chandiok - which comes with qualified report

FY19 0.25 Lakhs - Anmol Bohra

FY20 0.28 Lakhs - Anmol Bohra

FY21 1.90 Lakhs - D.N. Jhamb

FY22 7.22 Lakhs - D.N. Jhamb

Now Walker Chandiok - which comes with qualified report

The eye brow raising question is Whether it’s previous 4 year financial were relying on which stock has been on its dream run

IPO came at 40(adjusted split)

Made a high of 3150 (7875%)

Now trading at 1097 ~ corrected by more than 65% from highs

IPO came at 40(adjusted split)

Made a high of 3150 (7875%)

Now trading at 1097 ~ corrected by more than 65% from highs

A good read from Bloomberg on EKI Energy raising question on its business

bloomberg.com/news/features/…

bloomberg.com/news/features/…

Clarification from the company 's Investor Presentation. It mainly talks about the difference between the opinion of Auditor/Accounting Principles and Management over recognition of the revenue for the period 9M ended on 31st Dec -22

Question of accounting gimmick remain same

Question of accounting gimmick remain same

Adding more redlfags on EKI Subsidiary financials & their status of audit

- Unaudited

- Auditor have signed FS but no Audit Report available

- Audited by old auditor who resigned earlier due to pre-commitments

Attaching pics for reference & link to FS enkingint.org/investors/

- Unaudited

- Auditor have signed FS but no Audit Report available

- Audited by old auditor who resigned earlier due to pre-commitments

Attaching pics for reference & link to FS enkingint.org/investors/

• • •

Missing some Tweet in this thread? You can try to

force a refresh