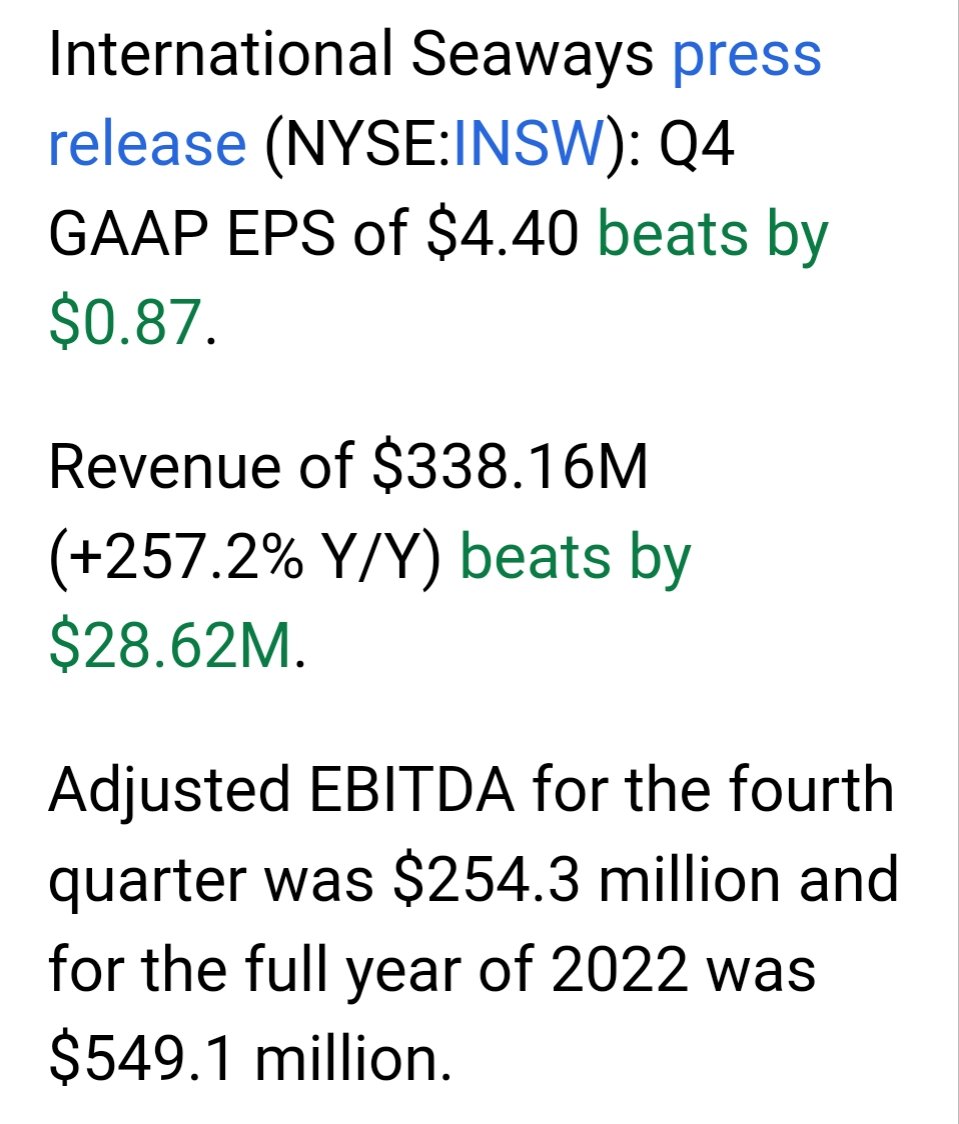

$INSW nice beat!

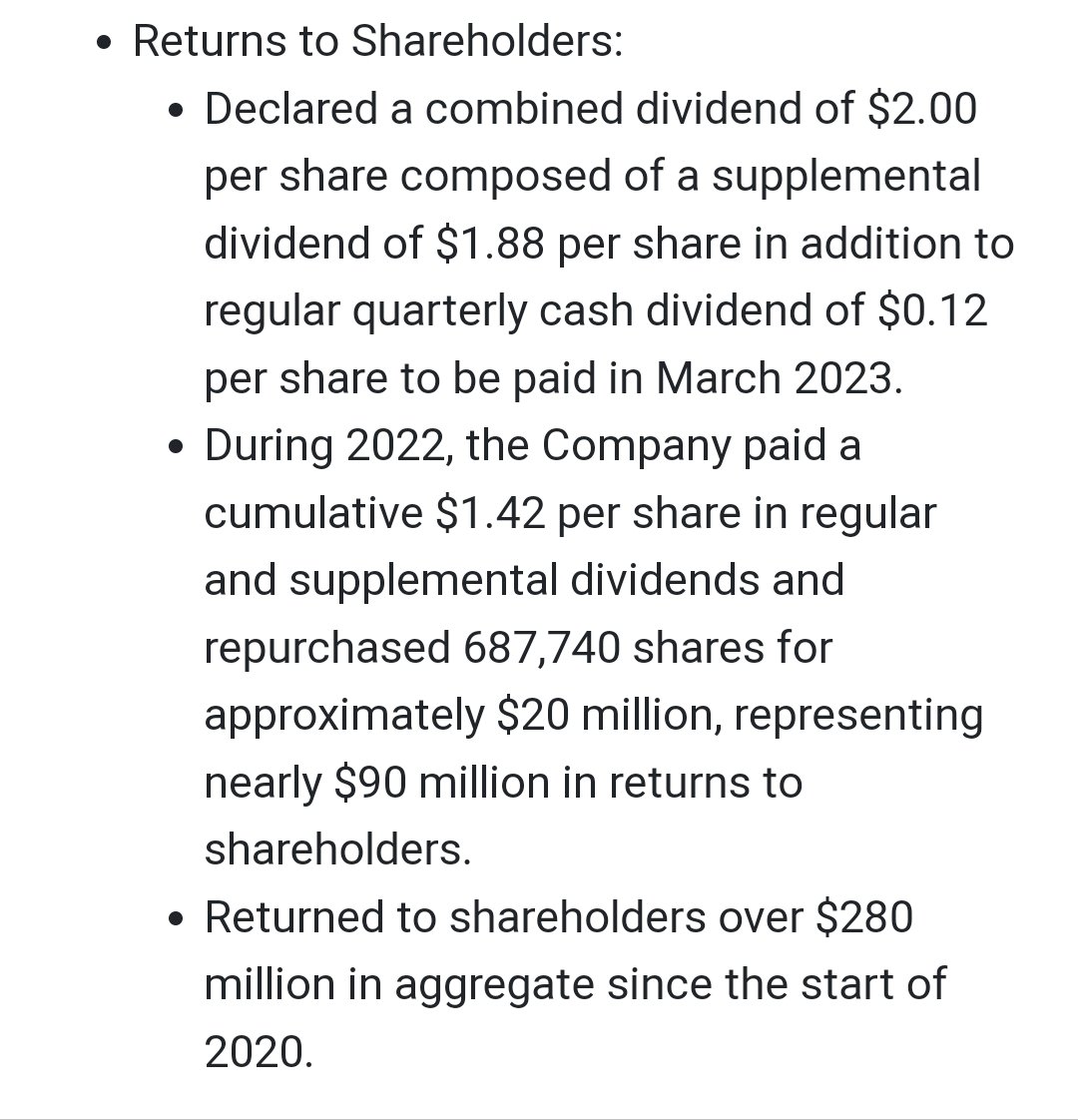

As I expected, special dividend

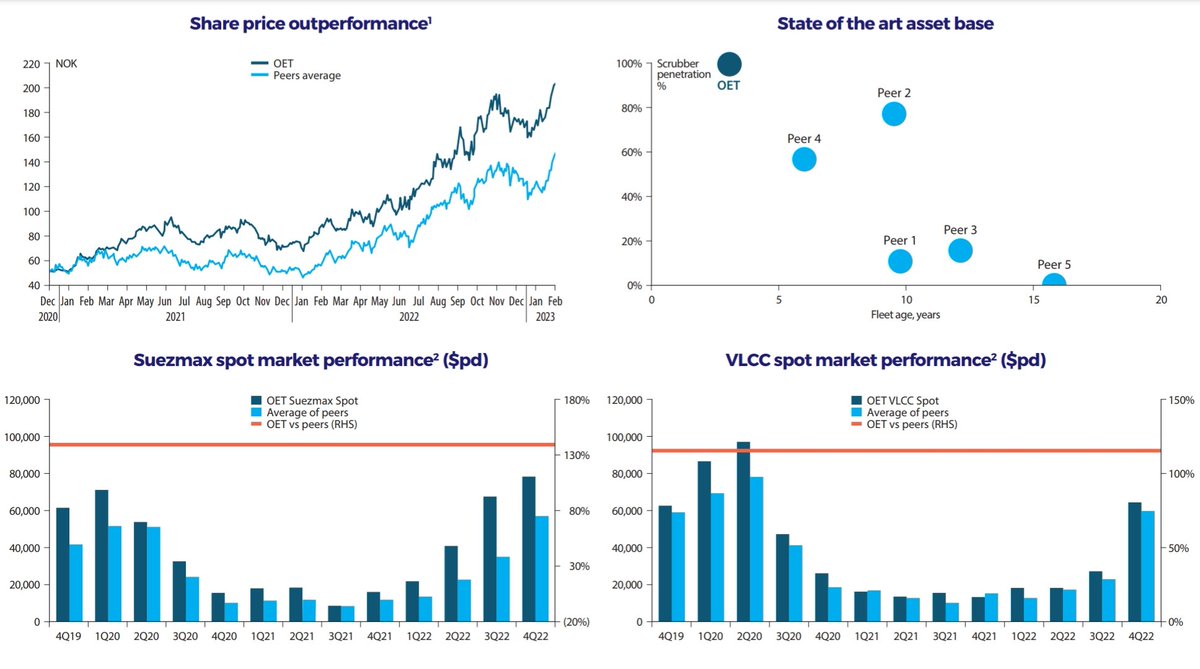

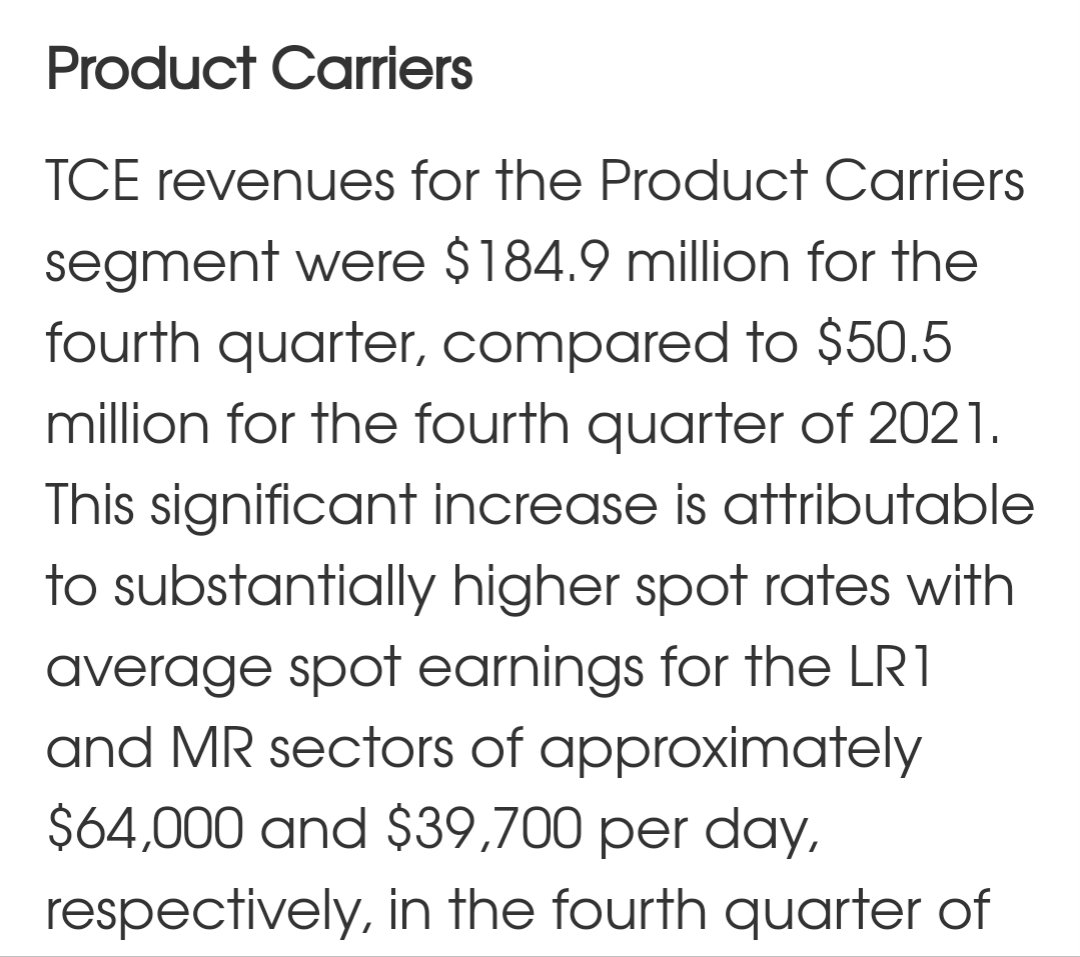

$INSW Q4 2022: interesting to compare to $STNG $ASC & now $HAFNI achieved rates

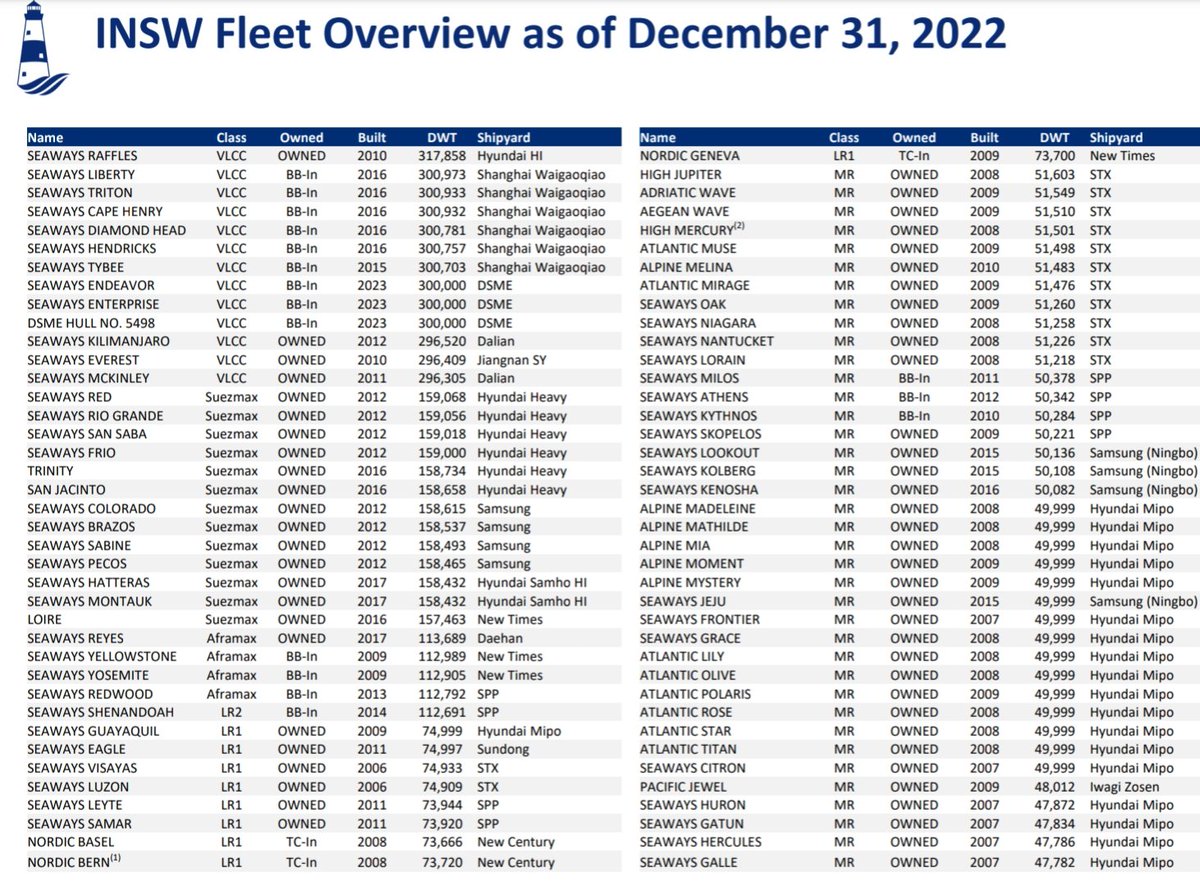

$INSW updated fleet list

• • •

Missing some Tweet in this thread? You can try to

force a refresh