How Investment Fund Carried Interest Works

A big thread 🧵(with graphics)

(American vs. European waterfalls)

A big thread 🧵(with graphics)

(American vs. European waterfalls)

1/ Background

An investment fund’s “waterfall” governs how the fund’s earnings are distributed between the GP and the LPs.

An investment fund’s “waterfall” governs how the fund’s earnings are distributed between the GP and the LPs.

2/ Background

Some funds have one waterfall that applies to all distributions of cash, securities, digital assets, or other property.

Some funds have one waterfall that applies to all distributions of cash, securities, digital assets, or other property.

3/ Background

Other funds have:

one waterfall for recurring income (such as rents in a real estate fund or interest income in a debt fund

and

a separate waterfall for capital events (like selling or refinancing a property).

Other funds have:

one waterfall for recurring income (such as rents in a real estate fund or interest income in a debt fund

and

a separate waterfall for capital events (like selling or refinancing a property).

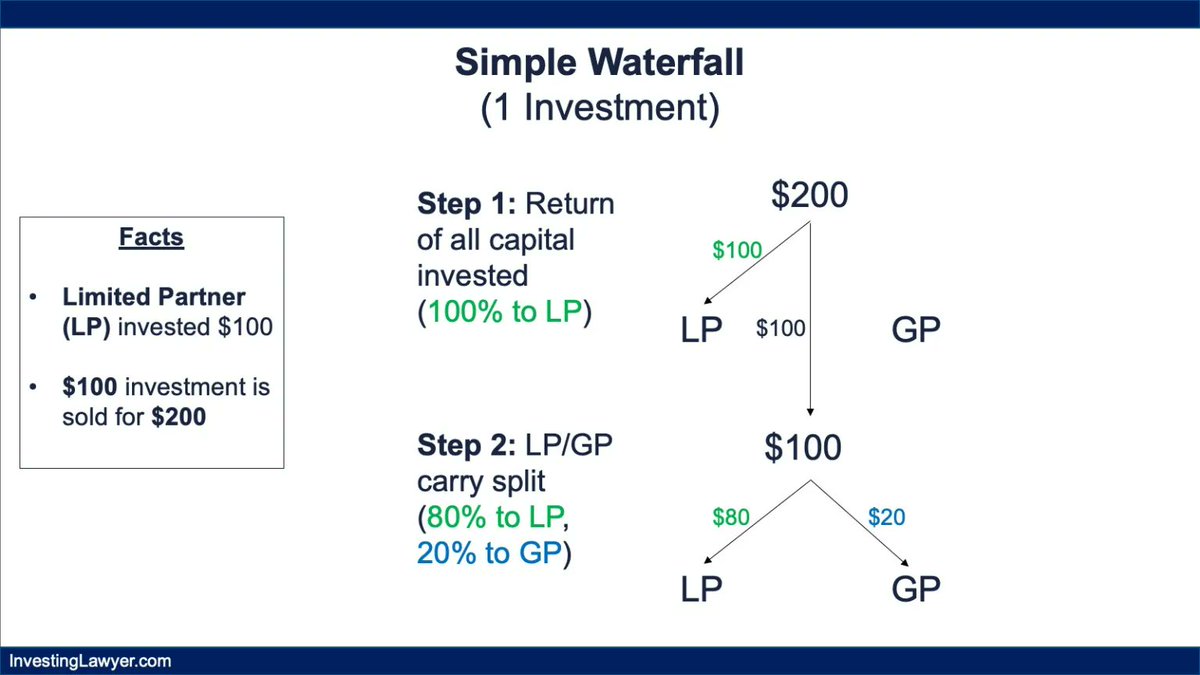

4/ Simple SPV Waterfall

In the most basic waterfall (for single-asset SPVs):

➡️First, 100% of distributions go to the LP until the LP receives all of its capital back – this is the “return of capital” step.

➡️Thereafter, 80% of distributions go to the LP and 20% to the GP.

In the most basic waterfall (for single-asset SPVs):

➡️First, 100% of distributions go to the LP until the LP receives all of its capital back – this is the “return of capital” step.

➡️Thereafter, 80% of distributions go to the LP and 20% to the GP.

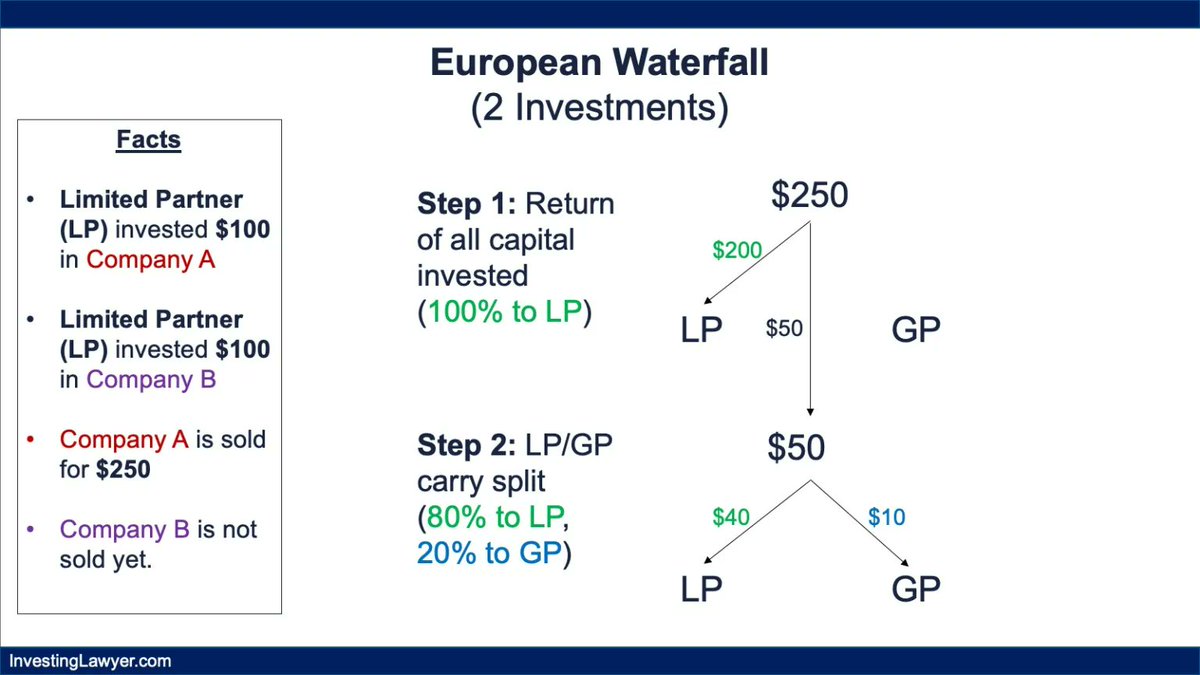

5/ European Waterfall

European waterfalls are one option for investment funds owning multiple assets.

European waterfalls are LP-friendly.

European waterfalls are one option for investment funds owning multiple assets.

European waterfalls are LP-friendly.

6/ European Waterfall

Example European waterfall:

➡️First, 100% of distributions go to the LP until the LP receives an amount equal to 100% of the capital it contributed to the fund.

➡️Next, the GP/LP profit split kicks in. For example, 80% to the LP and 20% to the GP.

Example European waterfall:

➡️First, 100% of distributions go to the LP until the LP receives an amount equal to 100% of the capital it contributed to the fund.

➡️Next, the GP/LP profit split kicks in. For example, 80% to the LP and 20% to the GP.

7/ European Waterfall

In the example above, the LP contributed $100 for investments in each of Company A and Company B.

Even though Company B hasn’t been sold yet, the LP gets a return of its Company B contributions before the GP gets a dime from the sale of Company A.

In the example above, the LP contributed $100 for investments in each of Company A and Company B.

Even though Company B hasn’t been sold yet, the LP gets a return of its Company B contributions before the GP gets a dime from the sale of Company A.

8/ European Waterfall

If the fund had 10 investments and the LP contributed $100 to fund each investment, the European waterfall would require that the LP receive $1,000 back before the GP/LP split kicks in.

If the fund had 10 investments and the LP contributed $100 to fund each investment, the European waterfall would require that the LP receive $1,000 back before the GP/LP split kicks in.

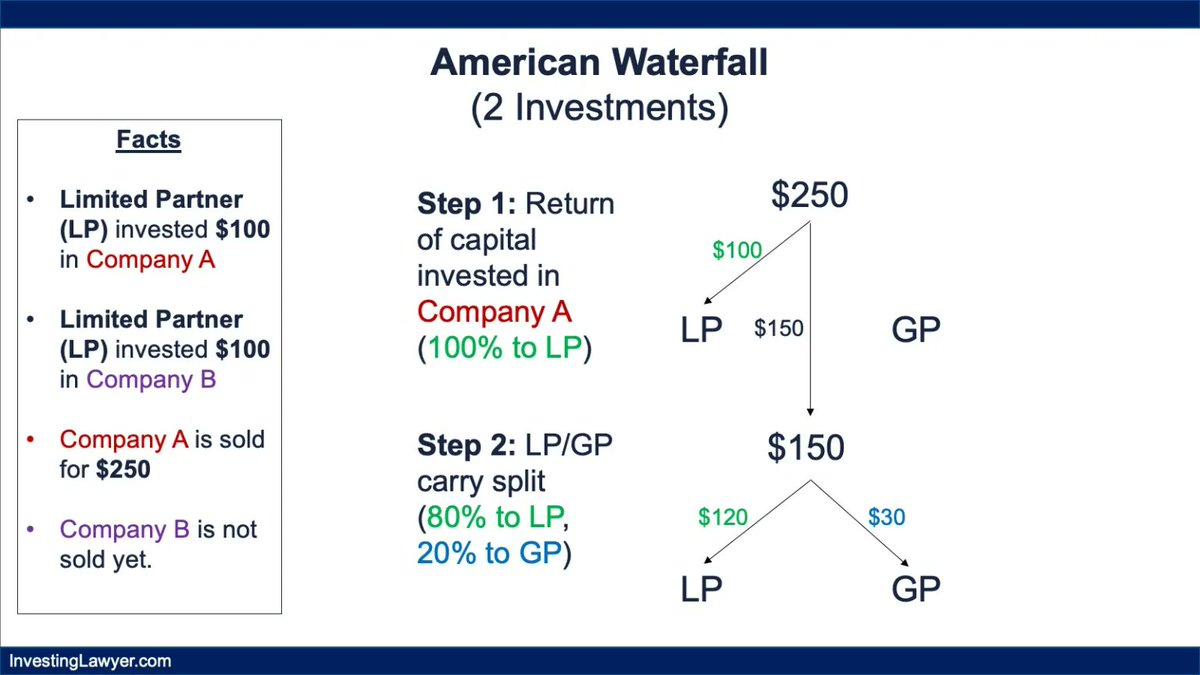

9/ American Waterfall

American waterfalls are a more GP-friendly waterfall for an investment fund with multiple assets.

There are a few different flavors of American waterfalls, but generally Step 1 only gives the LP a partial return of capital before the GP/LP split.

American waterfalls are a more GP-friendly waterfall for an investment fund with multiple assets.

There are a few different flavors of American waterfalls, but generally Step 1 only gives the LP a partial return of capital before the GP/LP split.

10/ American Waterfall

In the example below, Company A ($100 cost) is sold for $250. Company B ($100 cost) has not been sold.

In a European waterfall, the LP would receive $200 before the carry split begins.

In the example below, Company A ($100 cost) is sold for $250. Company B ($100 cost) has not been sold.

In a European waterfall, the LP would receive $200 before the carry split begins.

11/ American Waterfall

In the American waterfall, the LP only receives a return of capital invested in Company A ($100) in Step 1.

$150 runs through the GP/LP split, resulting in the GP receiving $30 of carried interest instead of $10 in the European waterfall.

In the American waterfall, the LP only receives a return of capital invested in Company A ($100) in Step 1.

$150 runs through the GP/LP split, resulting in the GP receiving $30 of carried interest instead of $10 in the European waterfall.

12/ American Waterfall

There are various ways to structure an American waterfall.

The Step 1 return of capital might include any of the following (going in order of GP-friendly to LP-friendly):

There are various ways to structure an American waterfall.

The Step 1 return of capital might include any of the following (going in order of GP-friendly to LP-friendly):

13/ American Waterfall

Option 1:

LP receives a return of contributions to fund (i) the cost basis of the investment sold and (ii) fund expenses related to the investment sold.

Option 1:

LP receives a return of contributions to fund (i) the cost basis of the investment sold and (ii) fund expenses related to the investment sold.

14/ American Waterfall

Option 2:

LP receives a return of contributions to fund (i) the cost basis of all investments that have been sold or permanently written down to zero and (ii) fund expenses related to investments that have been sold or permanently written down to zero.

Option 2:

LP receives a return of contributions to fund (i) the cost basis of all investments that have been sold or permanently written down to zero and (ii) fund expenses related to investments that have been sold or permanently written down to zero.

15/ American Waterfall

Option 3:

LP receives a return of contributions to fund (i) the cost basis of all investments that have been sold or permanently written down to zero and (ii) fund expenses related to all investments.

Option 3:

LP receives a return of contributions to fund (i) the cost basis of all investments that have been sold or permanently written down to zero and (ii) fund expenses related to all investments.

16/ Which Waterfall is More Common?

Most venture capital funds have European waterfalls.

Other asset types (such as private equity and real estate) are more likely than venture funds to have American waterfalls but many have European waterfalls as well.

Most venture capital funds have European waterfalls.

Other asset types (such as private equity and real estate) are more likely than venture funds to have American waterfalls but many have European waterfalls as well.

• • •

Missing some Tweet in this thread? You can try to

force a refresh