Banks collapsing has many worried about recession

Can companies in your portfolio weather the storm?

3️⃣ simple metrics to give you the answer⤵️

Can companies in your portfolio weather the storm?

3️⃣ simple metrics to give you the answer⤵️

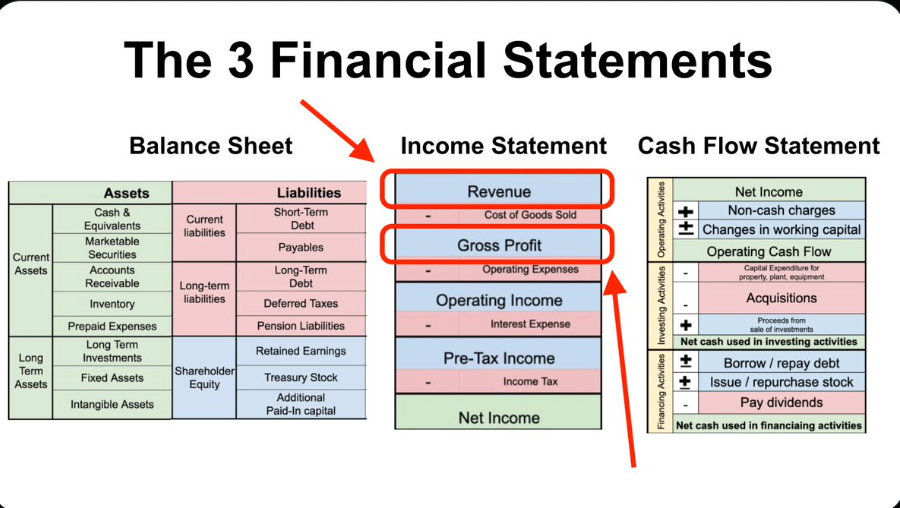

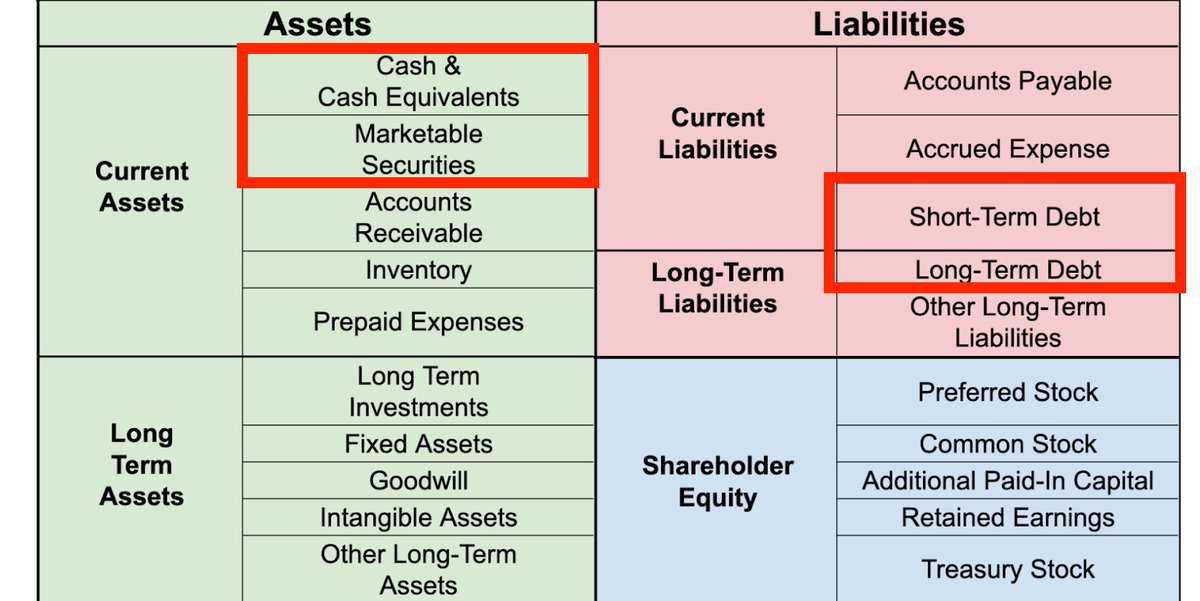

The first two metrics come from the BALANCE SHEET

1️⃣ Cash & Short-Term Investments

2️⃣ Debt (especially Long-Term)

This tells you a company's NET CASH position.

➕ Net Cash means more cash than debt

➖ Net Cash means more debt than cash

1️⃣ Cash & Short-Term Investments

2️⃣ Debt (especially Long-Term)

This tells you a company's NET CASH position.

➕ Net Cash means more cash than debt

➖ Net Cash means more debt than cash

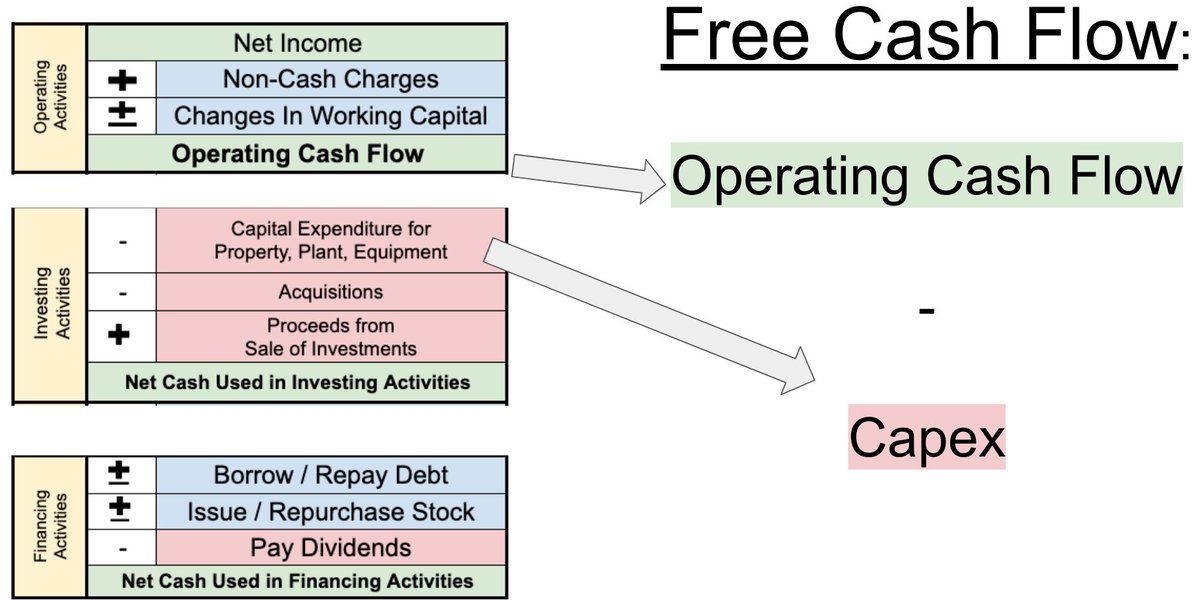

The last metric comes from the statement of CASH FLOWS

3️⃣ Free Cash Flow

The calculation⤵️

3️⃣ Free Cash Flow

The calculation⤵️

Think about it this way:

👉 The NET CASH position tells you if there's any gas sitting in the tank

👉 Free Cash Flow tells you if gas is GOING INTO or OUT OF the tank

The higher the net cash and FCF are, the better

👉 The NET CASH position tells you if there's any gas sitting in the tank

👉 Free Cash Flow tells you if gas is GOING INTO or OUT OF the tank

The higher the net cash and FCF are, the better

Put in one of 3 buckets

👉 FRAGILE: ➖ Net Cash & ➖ FCF

These will suffer when a crisis hits

👉 ROBUST: ➕ Net Cash & ➕ FCF

These will survive a crisis, but not get stronger

👉ANTIFRAGILE: ➕➕ Net Cash & ➕➕ FCF

These will get stronger BECAUSE OF the crisis. Here's how⤵️

👉 FRAGILE: ➖ Net Cash & ➖ FCF

These will suffer when a crisis hits

👉 ROBUST: ➕ Net Cash & ➕ FCF

These will survive a crisis, but not get stronger

👉ANTIFRAGILE: ➕➕ Net Cash & ➕➕ FCF

These will get stronger BECAUSE OF the crisis. Here's how⤵️

If you have TONS of cash and LOTS of FCF, you can do things others can't:

1️⃣ Acquire distressed competitors

2️⃣ Buyback your own shares on the cheap

3️⃣ Sell your products at a loss -- which you can survive, but drives the competition into bankruptcy

1️⃣ Acquire distressed competitors

2️⃣ Buyback your own shares on the cheap

3️⃣ Sell your products at a loss -- which you can survive, but drives the competition into bankruptcy

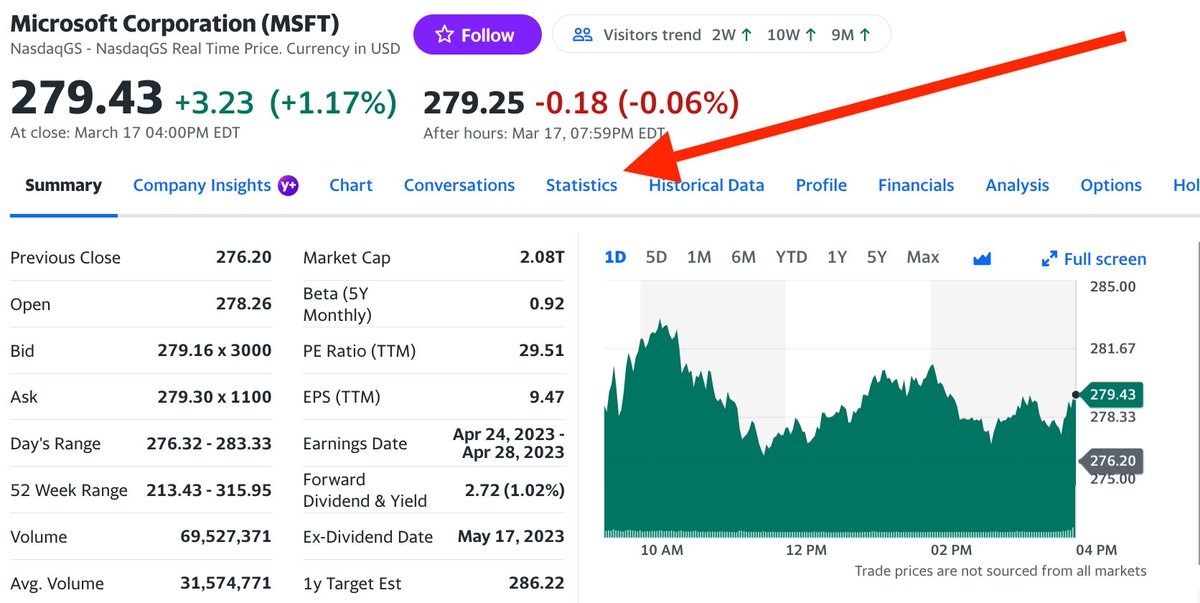

You can find all of these on Yahoo! Finance.

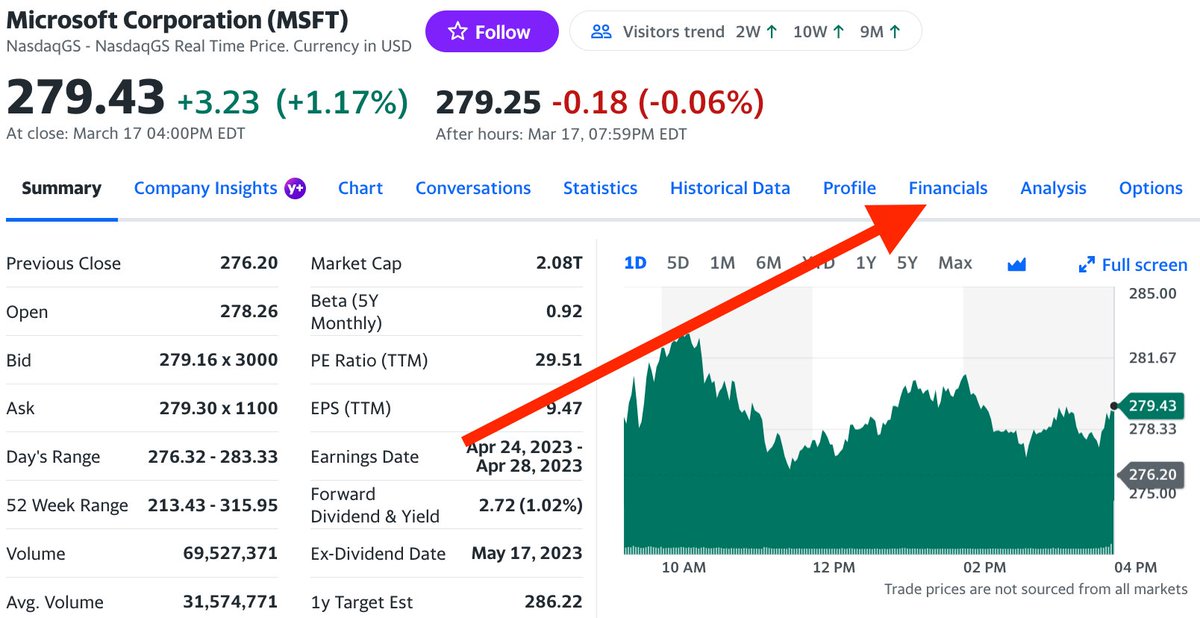

Let's use $MSFT as an example.

Click on the Statistics tab first

Let's use $MSFT as an example.

Click on the Statistics tab first

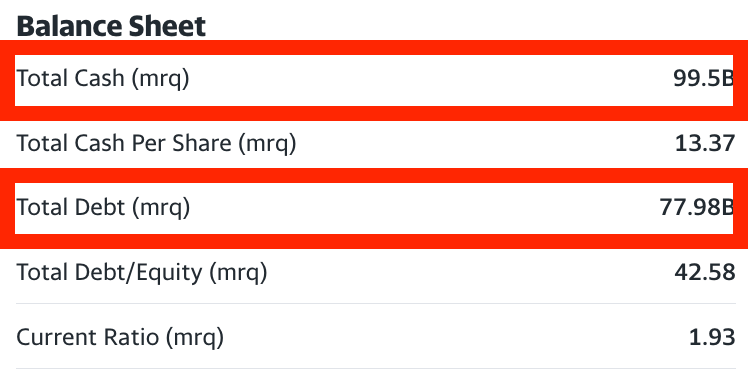

Here, we quickly see

👉 Cash: ~$100 Billion

👉 Debt: ~$78 Billion

Net Cash = ➕ $22 Billion

👉 Cash: ~$100 Billion

👉 Debt: ~$78 Billion

Net Cash = ➕ $22 Billion

Next, we check Free Cash Flow by clicking on

FINANCIALS

then on

CASH FLOW

FINANCIALS

then on

CASH FLOW

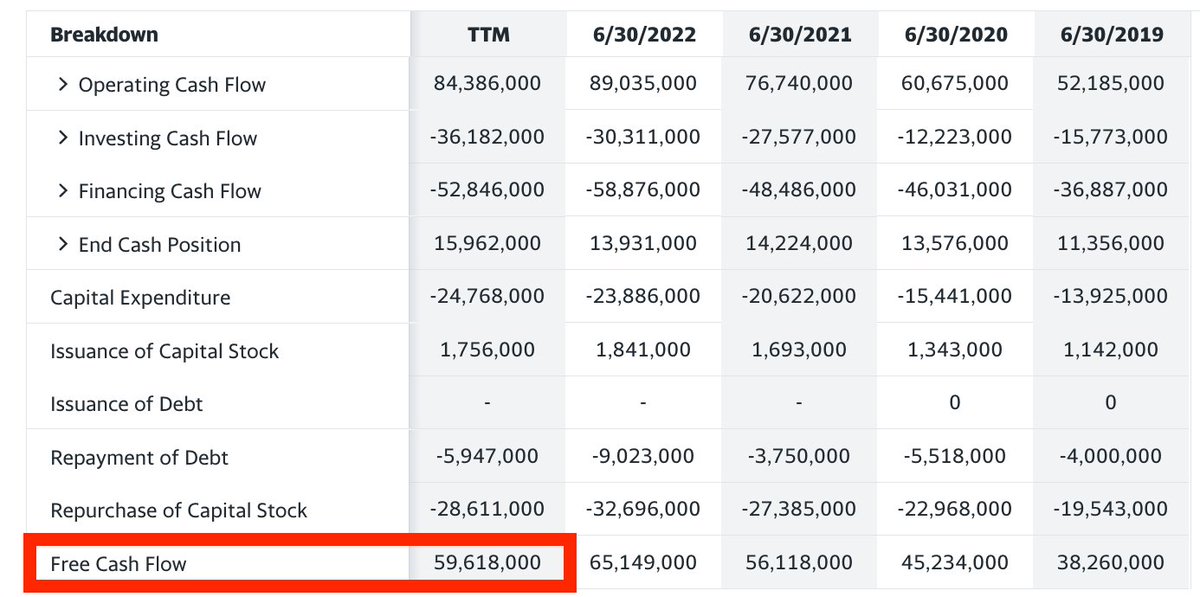

Scroll down and Free Cash Flow over the trailing twelve months (TTM) is calculated for you.

For $MSFT that's.....👀$60 Billion👀

Yes, you read that right. It has $60 Billion flowing into its accounts ANNUALLY right now

For $MSFT that's.....👀$60 Billion👀

Yes, you read that right. It has $60 Billion flowing into its accounts ANNUALLY right now

That does NOT mean $MSFT stock won't go down in a recession.

It DOES mean $MSFT will be able to do things others can't in a downturn.

And in the LONG-RUN, that *will* have a positive effect on $MSFT stock

It DOES mean $MSFT will be able to do things others can't in a downturn.

And in the LONG-RUN, that *will* have a positive effect on $MSFT stock

If focusing on the LONG-RUN matters to you as an investor, you'll love my FREE weekly, newsletter. 50,000+ investors are already subscribed.

Join us by entering your email here:

brianstoffel.com

Join us by entering your email here:

brianstoffel.com

To review

Check:

1️⃣ Cash & Short-Term Investments

2️⃣ Debt (especially Long-Term)

3️⃣ Free Cash Flow

Companies go in one of three buckets

👉 FRAGILE: Lots of debt, little cash, negative FCF

👉 ROBUST: Positive net cash, some FCF

👉 ANTIFRAGILE: MUCH more cash, LOTS of FCF

Check:

1️⃣ Cash & Short-Term Investments

2️⃣ Debt (especially Long-Term)

3️⃣ Free Cash Flow

Companies go in one of three buckets

👉 FRAGILE: Lots of debt, little cash, negative FCF

👉 ROBUST: Positive net cash, some FCF

👉 ANTIFRAGILE: MUCH more cash, LOTS of FCF

• • •

Missing some Tweet in this thread? You can try to

force a refresh