Confused about which Tax Regime to choose? 🤔

🧾Old Regime with Deductions and Exemptions, or

📉New Regime with Lower Slab Rates, but Fewer Exemptions

Don't worry, this🧵will help you Decide Which Regime will be More Beneficial to You and Help you Save the Most Taxes💰

🧾Old Regime with Deductions and Exemptions, or

📉New Regime with Lower Slab Rates, but Fewer Exemptions

Don't worry, this🧵will help you Decide Which Regime will be More Beneficial to You and Help you Save the Most Taxes💰

✳️ Why do you have to opt for a Tax Regime?

→ CBDT (via circular no 04/2023) made it COMPULSORY for Employers to seek information from their Employees on which regime they wish to opt for?

→ The Employer shall deduct TDS accordingly.

→ CBDT (via circular no 04/2023) made it COMPULSORY for Employers to seek information from their Employees on which regime they wish to opt for?

→ The Employer shall deduct TDS accordingly.

→ If You FAIL to choose between the New and Old Tax Regime, the Employer will take the New Tax Regime as DEFAULT and Subtract the TDS under it.

This could mean a Higher TDS Outflow for you!!

→ However, you will have the option to Change it at the time of Filing your ITR.

This could mean a Higher TDS Outflow for you!!

→ However, you will have the option to Change it at the time of Filing your ITR.

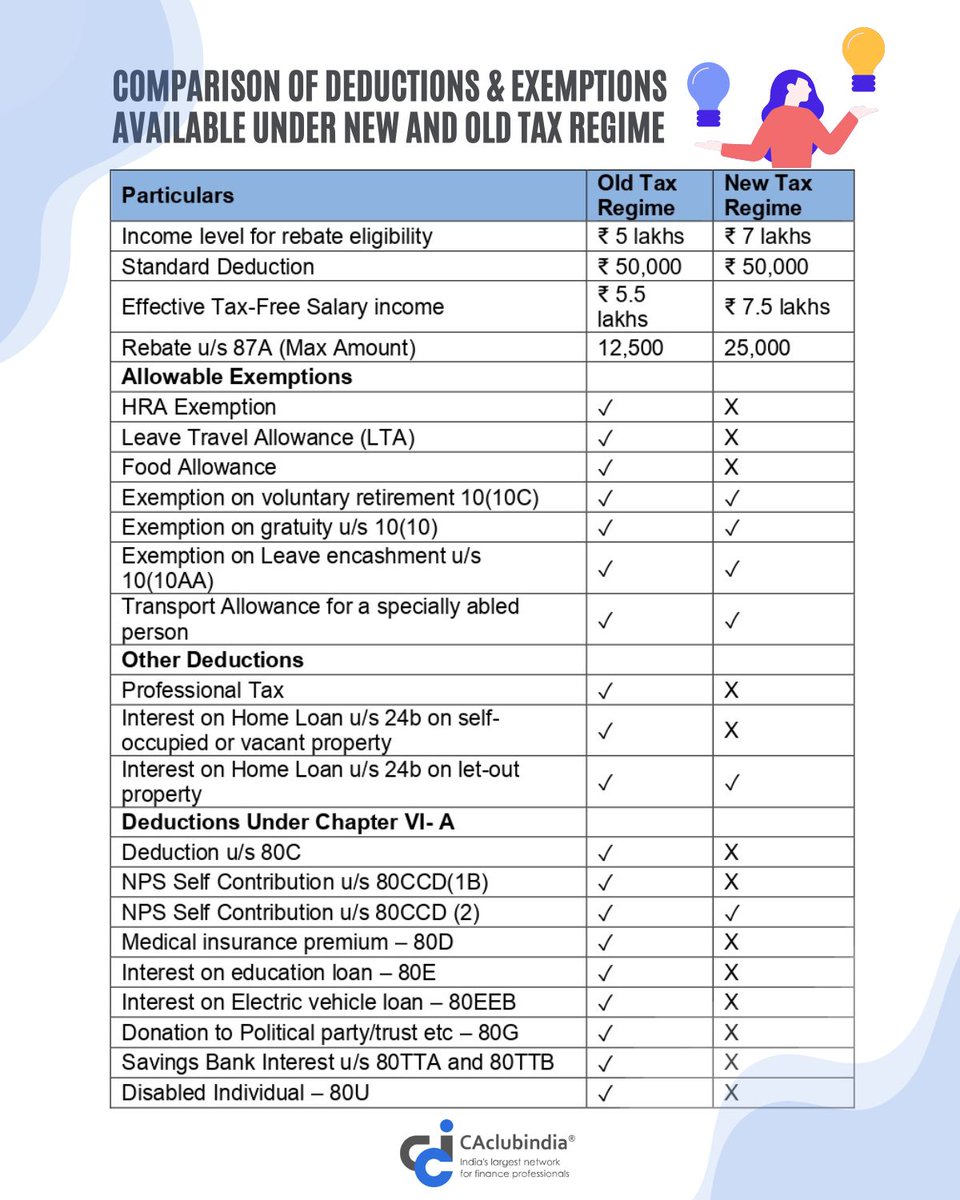

✳️ New vs Old Regime - How do they stack up?

🔅Basic Exemption Limit

🔸Old Regime - 2.5 Lakh

🔹New Regime - 3 Lakh

🔅Income Tax Rebate Limit

🔸Old Regime - 5 Lakh

🔹New Regime - 7 Lakh

🔅Standard Deduction

🔸Old Regime - 50,000

🔹New Regime - 50,000

🔅Basic Exemption Limit

🔸Old Regime - 2.5 Lakh

🔹New Regime - 3 Lakh

🔅Income Tax Rebate Limit

🔸Old Regime - 5 Lakh

🔹New Regime - 7 Lakh

🔅Standard Deduction

🔸Old Regime - 50,000

🔹New Regime - 50,000

🔅Income Tax Slab Rates

🔸Old Regime

0-2.5 Lakhs - Nil

2.5-5 Lakhs - 5%

5-10 Lakhs - 20%

Above 10 Lakhs - 30%

🔹New Regime

0-3 Lakhs - Nil

3-6 Lakhs - 5%

6-9 Lakhs - 10%

9-12 Lakhs - 15%

12-15 Lakhs - 20%

Above 15 Lakhs - 30%

Beautifully Summarized by @CA_HarshilSHETH

🔸Old Regime

0-2.5 Lakhs - Nil

2.5-5 Lakhs - 5%

5-10 Lakhs - 20%

Above 10 Lakhs - 30%

🔹New Regime

0-3 Lakhs - Nil

3-6 Lakhs - 5%

6-9 Lakhs - 10%

9-12 Lakhs - 15%

12-15 Lakhs - 20%

Above 15 Lakhs - 30%

Beautifully Summarized by @CA_HarshilSHETH

🔅Deductions and Exemptions Available

🔸Old Regime

- Investments under Section 80C (PPF, ELSS, EPF, Life Insurance Premium, Home Loan Principal, etc).

- Home Loan Interest Payment

- Health Insurance Premiums

🔸Old Regime

- Investments under Section 80C (PPF, ELSS, EPF, Life Insurance Premium, Home Loan Principal, etc).

- Home Loan Interest Payment

- Health Insurance Premiums

- Expenses on medical treatment, training or rehabilitation of a disabled dependent

- Treatment of self or dependent for specified disease

- Contribution to NPS

- Interest paid on Education Loan

- Donation to specified institutions

- Treatment of self or dependent for specified disease

- Contribution to NPS

- Interest paid on Education Loan

- Donation to specified institutions

- Disability of self

- House Rent Allowance

- Leave Travel Allowance

-Leave Encashment

- Mobile and Internet Reimbursement, Food Coupons or Vouchers, Uniform Allowance, etc.

- House Rent Allowance

- Leave Travel Allowance

-Leave Encashment

- Mobile and Internet Reimbursement, Food Coupons or Vouchers, Uniform Allowance, etc.

🔹New Regime

- Deduction towards Employer’s Contribution to NPS

- Expenses towards earnings from Family Pension upto 15,000

- Standard deduction of up to 30 percent of the annual value of the let-out property, in case of rental income from property

- Deduction towards Employer’s Contribution to NPS

- Expenses towards earnings from Family Pension upto 15,000

- Standard deduction of up to 30 percent of the annual value of the let-out property, in case of rental income from property

- Exemption on Voluntary Retirement 10(10C), Gratuity u/s 10(10) and Leave Encashment u/s 10(10AA)

- Deduction for additional employee cost

- Amount paid or deposited in the Agniveer Corpus Fund

- Deduction for additional employee cost

- Amount paid or deposited in the Agniveer Corpus Fund

- Also, Interest and maturity proceeds from schemes such as Public Provident Fund (PPF) and Sukanya Samriddhi account and Life Insurance Policies remain Tax-Exempt under the New Regime.

Beautifully Captured by @CAclubindia

Beautifully Captured by @CAclubindia

✳️Some Tips on How to Choose the Right Tax Regime for You

→ If you have income upto Rs 7 lakh then the New Tax Regime is better

→ If you have No Tax savings and Deductions to avail then consider going for the New Tax Regime

→ If you have income upto Rs 7 lakh then the New Tax Regime is better

→ If you have No Tax savings and Deductions to avail then consider going for the New Tax Regime

→ If you have just 80C Deduction of Rs 1.5 lakh then New Tax Regime might be better

→ If you can avail 80C Deduction and also have a Home Loan consider the Old Tax Regime

→ If you have an HRA Deduction to claim, the Old Tax Regime might be better for you.

→ If you can avail 80C Deduction and also have a Home Loan consider the Old Tax Regime

→ If you have an HRA Deduction to claim, the Old Tax Regime might be better for you.

✳️Now let's understand which Tax Regime will be More Beneficial for you depending on your Income Group

✅For Income = 8 Lakhs

- If Deductions + Exemptions > 212,500 : Old Regime - If Deductions + Exemptions < 212,500 : New Regime

✅For Income = 8 Lakhs

- If Deductions + Exemptions > 212,500 : Old Regime - If Deductions + Exemptions < 212,500 : New Regime

✅For Income = 9 Lakhs

- If Deductions + Exemptions > 262,500 : Old Regime

- If Deductions + Exemptions < 262,500 : New Regime

✅For Income up to 10 Lakhs

- If Deductions + Exemptions > 300,000 : Old Regime

- If Deductions + Exemptions < 300,000 : New Regime

- If Deductions + Exemptions > 262,500 : Old Regime

- If Deductions + Exemptions < 262,500 : New Regime

✅For Income up to 10 Lakhs

- If Deductions + Exemptions > 300,000 : Old Regime

- If Deductions + Exemptions < 300,000 : New Regime

✅For Income = 11 Lakhs

- If Deductions + Exemptions > 325,000 : Old Regime

- If Deductions + Exemptions < 325,000 : New Regime

✅For Income = 12 Lakhs

- If Deductions + Exemptions > 350,000 : Old Regime

- If Deductions + Exemptions < 350,000 : New Regime

- If Deductions + Exemptions > 325,000 : Old Regime

- If Deductions + Exemptions < 325,000 : New Regime

✅For Income = 12 Lakhs

- If Deductions + Exemptions > 350,000 : Old Regime

- If Deductions + Exemptions < 350,000 : New Regime

✅For Income = 13 Lakhs

- If Deductions + Exemptions > 362,000 : Old Regime

- If Deductions + Exemptions < 362,000 : New Regime

✅For Income = 14 Lakhs

- If Deductions + Exemptions > 375,000 : Old Regime

- If Deductions + Exemptions < 375,000 : New Regime

- If Deductions + Exemptions > 362,000 : Old Regime

- If Deductions + Exemptions < 362,000 : New Regime

✅For Income = 14 Lakhs

- If Deductions + Exemptions > 375,000 : Old Regime

- If Deductions + Exemptions < 375,000 : New Regime

✅For Income = 15 Lakhs

- If Deductions + Exemptions > 408,500 : Old Regime

- If Deductions + Exemptions < 408,500 : New Regime

✅For Income of 15.5 lakhs - 5 Cr

- If Deductions + Exemptions > 425,000 : Old Regime

- If Deductions + Exemptions < 425,000 : New Regime

- If Deductions + Exemptions > 408,500 : Old Regime

- If Deductions + Exemptions < 408,500 : New Regime

✅For Income of 15.5 lakhs - 5 Cr

- If Deductions + Exemptions > 425,000 : Old Regime

- If Deductions + Exemptions < 425,000 : New Regime

That's a Wrap!!

I have tried my best to Answer all your Queries regarding Old vs New Tax Regime 🤝

If you Liked this 🧵, Please Like 👍 and Retweet 🔃 the First Tweet to Share the Information with other Tax Payers.

I have tried my best to Answer all your Queries regarding Old vs New Tax Regime 🤝

If you Liked this 🧵, Please Like 👍 and Retweet 🔃 the First Tweet to Share the Information with other Tax Payers.

https://twitter.com/garimabajpai/status/1646144205960404993?t=mTolE0v7lEij0NGZjwv3sg&s=19

Follow me @garimabajpai to see more such Threads and Infographics on -

🔹Tax Saving

🔹Personal Finance

🔹Investing, and

🔹Startups

Do Remember to Hit the Bell 🔔 icon to Never miss a Thread/Infographic!!

Until then Happy Learning to you all!!

🔹Tax Saving

🔹Personal Finance

🔹Investing, and

🔹Startups

Do Remember to Hit the Bell 🔔 icon to Never miss a Thread/Infographic!!

Until then Happy Learning to you all!!

• • •

Missing some Tweet in this thread? You can try to

force a refresh