I rarely pay attention to macro forecasts. I’d rather spend time looking for great businesses selling cheap.

However, one person I listen to on macro is Stan Druckenmiller. Just finished listening to his presentation at the USC 🧵👇

1/15

However, one person I listen to on macro is Stan Druckenmiller. Just finished listening to his presentation at the USC 🧵👇

1/15

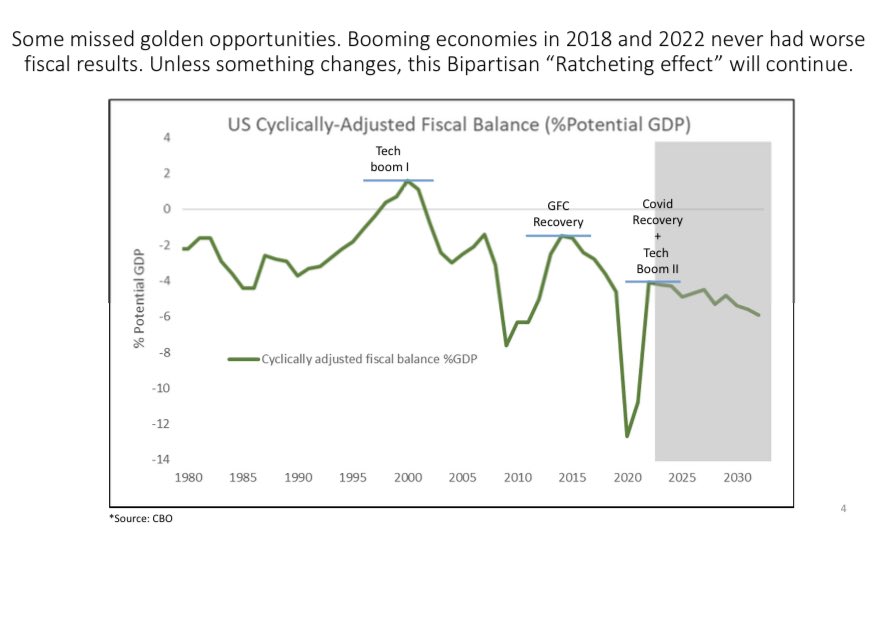

US fiscal position is on unsustainable path. US is already spending almost 40% of all taxes on seniors. In 20 years this will rise to 60%.

2/15

2/15

During the last decade, US debt grew from $15T to $31T today, a level only comparable to that after WWII.

“But what is worse is that this debt does not account for what the government has promised it will pay you in terms of social security and Medicare.”

3/15

“But what is worse is that this debt does not account for what the government has promised it will pay you in terms of social security and Medicare.”

3/15

The fiscal gap is how much taxes need to be raised to maintain the current magnitude of safety nets in the future. Today that measure is 7.7% of GDP. This is equivalent to a 40% increase in all Federal taxes collected, or, a cut of 35% in federal spending.

4/15

4/15

He concludes: “It is time that we let go of the false pretense that cutting entitlements is a choice. It is not. Either we cut them today or we will have to cut them much more tomorrow.”

5/15

5/15

Q: “Is it harder to invest today than before?”

A: “Yes, because I have never seen a roadmap for the current situation. I have never seen this movie before.”

“I read that 7 stocks are responsible for 85% of the S&P rise this year. It reminds me very much of Nifty Nifty era.”… twitter.com/i/web/status/1…

A: “Yes, because I have never seen a roadmap for the current situation. I have never seen this movie before.”

“I read that 7 stocks are responsible for 85% of the S&P rise this year. It reminds me very much of Nifty Nifty era.”… twitter.com/i/web/status/1…

On his investment process

I am waiting for the fat pitch and constantly reevaluate my process. The good thing about playing big is you don’t get lazy. I just want to stay alive financially until the chaos comes, because it’s coming. I don’t see the fat pitches currently.

7/15

I am waiting for the fat pitch and constantly reevaluate my process. The good thing about playing big is you don’t get lazy. I just want to stay alive financially until the chaos comes, because it’s coming. I don’t see the fat pitches currently.

7/15

“I am not as good an investor as I was in my 30s and 40s years ago. I can predict better I don’t pull the trigger the way when I was young. I only hire people in their 20s. Once you have the scars I have, it wears on you.”

8/15

8/15

“You have to have humility. If someone ever asked me what made me so successful, my first answer would be having an open mind. I had positions where I was sure I would hold them for 2 years and a week later I was short. Because conditions changed. And if conditions change, you… twitter.com/i/web/status/1…

Not positive on China: “A lot of its growth was “semi-capitalist”, but Xi proved himself to be “Maoist”. “There is room for only one monopoly in China - him.”

10/15

10/15

The mitigating factor is the mutual self-destruction. Zi knows that if he takes Taiwan, will take every semiconductor fab that TSMC has in 30 minutes.

Thinks China will not invade Taiwan in the next 3-5 years, but if economy weakens, chances will be higher.

11/15

Thinks China will not invade Taiwan in the next 3-5 years, but if economy weakens, chances will be higher.

11/15

Thinks Generative AI has the potential to be as transformative and even bigger than the Internet. This is going to create change and change leads to stock price changes.

Long $NVDA, $MSFT as AI beneficiaries. Doing more work to understand the future winners.

12/15

Long $NVDA, $MSFT as AI beneficiaries. Doing more work to understand the future winners.

12/15

His current positioning: short USD, long Gold, Euro, Oil, AUD.

13/15

13/15

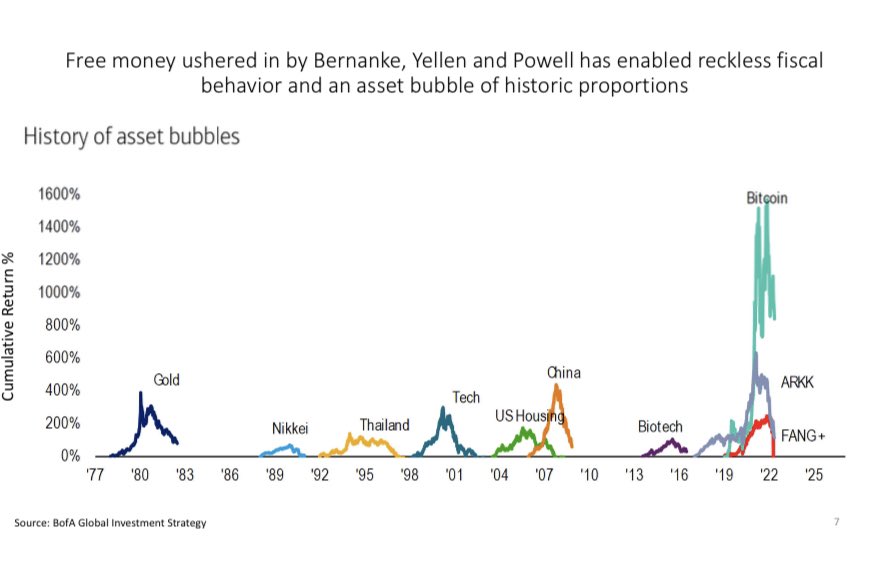

Druckenmiller recommended the book by Edward Chancellor “The price of time“ which he called Tour de Force. One lesson from the book which studied all financial bubbles over the past 500 years is that they were all followed by the worst economic outcomes.

amzn.to/3LRg97N

amzn.to/3LRg97N

“I am worried there are more “dead bodies” ahead, I just don’t know where they are. I knew them in ‘07-08. I don’t think SVB was the last one.”

/END

/END

• • •

Missing some Tweet in this thread? You can try to

force a refresh