0/🧵 @Tether_to announced $1.48b profits for Q1 2023 - omfg, and a bit of colour on their reserves

“IS $USDT BACKED?” is the oldest question in crypto

IMO, the appropriate question should be -> “IS $USDT FAIRLY COLLATERALISED?”

Here’s how I personally look at $USDT reserving… twitter.com/i/web/status/1…

“IS $USDT BACKED?” is the oldest question in crypto

IMO, the appropriate question should be -> “IS $USDT FAIRLY COLLATERALISED?”

Here’s how I personally look at $USDT reserving… twitter.com/i/web/status/1…

1/🧵By Q1’23 @Tether_to had issued $79.4b of digital tokens, and held $81.8b of assets -> in other words had net assets for $2.4b

Is this over-collateralisation enough? It depends through which lens you look at Tether:

1) Money transmitter (i.e. just a servicer)

2) Bank/ fund

Is this over-collateralisation enough? It depends through which lens you look at Tether:

1) Money transmitter (i.e. just a servicer)

2) Bank/ fund

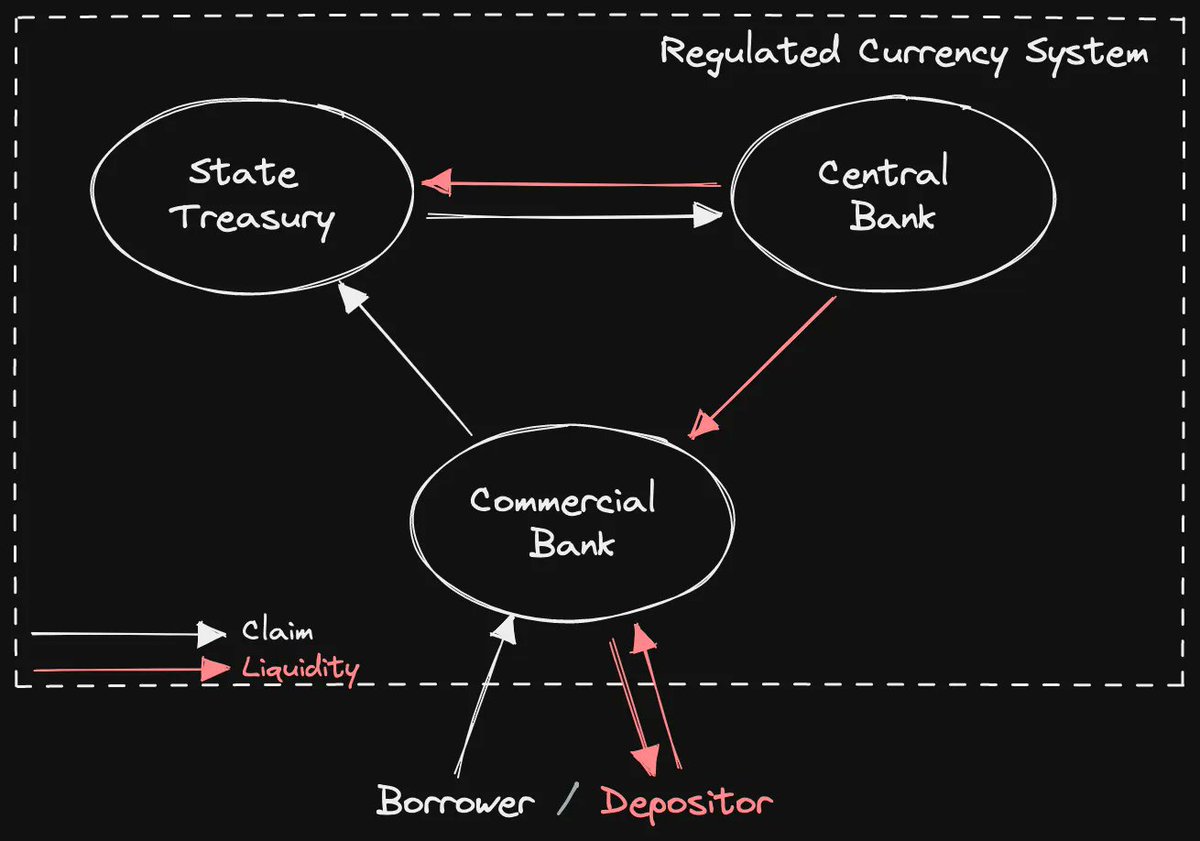

2/🧵What are *MONEY TRANSMITTERS*?

Money transmitters should be mere service providers, they:

- Take your cash, and keep it in quasi-cash assets

- Give you back receipt token/ representation of your cash

- Commit to give you back cash 1-for-1

@circle is issuing $USDC like this

Money transmitters should be mere service providers, they:

- Take your cash, and keep it in quasi-cash assets

- Give you back receipt token/ representation of your cash

- Commit to give you back cash 1-for-1

@circle is issuing $USDC like this

3/🧵Is @Tether_to a money transmitter?

Money transmitters have very (very) tight guidelines on how to store their reserves - and even like this they aren’t great, look at #SVB and @circle almost-debacle

Tether is definitely non-compliant with those guidelines, see yourself

Money transmitters have very (very) tight guidelines on how to store their reserves - and even like this they aren’t great, look at #SVB and @circle almost-debacle

Tether is definitely non-compliant with those guidelines, see yourself

4/🧵Ok so @Tether_to is not a money transmitter and has risk in their balance sheet

Is it a fund? Maybe

But Tether doesn’t want to be a fund, it wants to be a *BANK*

Why? Because banks can issue cheap liabiliites that are not securities - as Tether wants to do with $USDT

Is it a fund? Maybe

But Tether doesn’t want to be a fund, it wants to be a *BANK*

Why? Because banks can issue cheap liabiliites that are not securities - as Tether wants to do with $USDT

4/🧵 But banks (should) have adequate buffering for this privilege (ask @BIS_org)

Common Equity Tier 1 % is the best proxy we have to see whether this buffering is adequate

CET1 % = Equity Capital / Risk Weighted Assets

RWAs = like-for-like asset measure weighted for their… twitter.com/i/web/status/1…

Common Equity Tier 1 % is the best proxy we have to see whether this buffering is adequate

CET1 % = Equity Capital / Risk Weighted Assets

RWAs = like-for-like asset measure weighted for their… twitter.com/i/web/status/1…

5/🧵 Trying to apply standard risk-weights to @Tether_to, we see:

* c. 20% assets not for money transmitters

* c. $10b opaque/ risky assets may require significant weighting

* Huge impact of their $BTC position

Best/ worst scenario is 19.8% / 8.9% CET1 % (vs. EU average 14-15%)

* c. 20% assets not for money transmitters

* c. $10b opaque/ risky assets may require significant weighting

* Huge impact of their $BTC position

Best/ worst scenario is 19.8% / 8.9% CET1 % (vs. EU average 14-15%)

6/🧵 Below is my ultimate cheat-sheet for @Tether_to capital position:

* Gap of $1.5b with strict credit quality assumptions and punitive $BTC weighting

* Fair capitalisation with more benevolent assumptions

-> Tether’s capital position is tightly linked to their $BTC position

* Gap of $1.5b with strict credit quality assumptions and punitive $BTC weighting

* Fair capitalisation with more benevolent assumptions

-> Tether’s capital position is tightly linked to their $BTC position

7/🧵 *HOWEVER* analysis has several assumptions:

* No non-performing credit

* No add-ons for interest rate, as well as operational risk

* Limited add-ons for directional market risk

* Fair representation of all positions

A bit too much for a 0-yielding quasi-money like $USDT

* No non-performing credit

* No add-ons for interest rate, as well as operational risk

* Limited add-ons for directional market risk

* Fair representation of all positions

A bit too much for a 0-yielding quasi-money like $USDT

END/🧵 Here’s for the nerds (please @elonmusk don’t kill my S**s*a*ck link

open.substack.com/pub/dirtroads/…

@Tether_to $USDT @circle $USDC #stablecoins

open.substack.com/pub/dirtroads/…

@Tether_to $USDT @circle $USDC #stablecoins

• • •

Missing some Tweet in this thread? You can try to

force a refresh