Abalance - Manufacturing Nonsense

viceroyresearch.org/2023/05/17/aba…

#Abalance issued two unsatisfactory responses to concerns raised in our report.

Mgmt’s rebuttal does not deserve a response, however shareholders do. We will address every management denial, point-by-point, below. 1/

viceroyresearch.org/2023/05/17/aba…

#Abalance issued two unsatisfactory responses to concerns raised in our report.

Mgmt’s rebuttal does not deserve a response, however shareholders do. We will address every management denial, point-by-point, below. 1/

SUPPLY CHAIN & SCOPE

Despite over 20 pages and dozens more references in our reports to this effect, management claim that our concern related to supply chain forced labor is “unfounded”. It does not elaborate. 2/

Despite over 20 pages and dozens more references in our reports to this effect, management claim that our concern related to supply chain forced labor is “unfounded”. It does not elaborate. 2/

Management denies that it trades with Chinese suppliers who utilize forced labor in Xinjiang. This is a bad hill to die on.

Viceroy have pulled detailed import data which highlights and names its Chinese suppliers. #Abalance cannot deny it conducts business with them. 3/

Viceroy have pulled detailed import data which highlights and names its Chinese suppliers. #Abalance cannot deny it conducts business with them. 3/

These suppliers are heavily implicated, directly or via their supply chain, in their use of forced labor in Xinjiang.

The USA has already placed restrictions on upwards supply chain partners of polisilicon suppliers, including those >2 degrees of seperation from #abalance 4/

The USA has already placed restrictions on upwards supply chain partners of polisilicon suppliers, including those >2 degrees of seperation from #abalance 4/

What internal controls, if any, does Abalance have to ensure its supply chain is not tainted by forced labor?

Why does Abalance continue to source material from businesses who have been implicated in forced labor?

#abalance 5/

Why does Abalance continue to source material from businesses who have been implicated in forced labor?

#abalance 5/

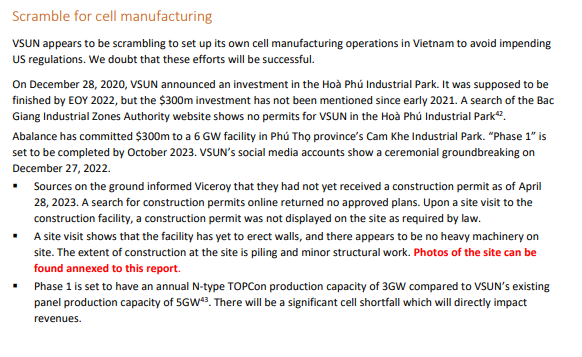

THE VSUN CONSTRUCTION SITE

Abalance allege that it received a construction permit on February 9, 2023. We have been unable to find any approved construction permits for the facility. #abalance 6/

Abalance allege that it received a construction permit on February 9, 2023. We have been unable to find any approved construction permits for the facility. #abalance 6/

We reiterate that a site visit conducted on the week ending May 12, 2023, no copies of the construction certificates were on display as required.

If management offer to provide a copy of this certificate, we will retract this concern. #abalance 7/

If management offer to provide a copy of this certificate, we will retract this concern. #abalance 7/

Phase 1 is set to have an annual N-type TOPCon production capacity of 3GW compared to VSUN’s existing panel production capacity of 5GW43 . There will be a significant cell shortfall which will directly impact revenues in the medium term. #abalance 8/

DUMPING & TRADE RESTRICTIONS

Management deny that #abalance is circumventing AD/CVD orders, and claim that they export solar panels in compliance with all laws and regulations of each country.

This is a lie. 9/

Management deny that #abalance is circumventing AD/CVD orders, and claim that they export solar panels in compliance with all laws and regulations of each country.

This is a lie. 9/

To be abundantly clear: #Abalance was specifically identified by the USA Department of Commerce’s (DoC) solar module AD/CVD investigation as circumventing AD/CVD orders. These orders have been in place since 2012. 10/

The DoC investigation aimed to ascertain the true origin of Solar Module products.

VSUN failed to respond to the DoC’s questionnaire, and was determined to be in breach of AD/CVD orders. #Abalance 11/

VSUN failed to respond to the DoC’s questionnaire, and was determined to be in breach of AD/CVD orders. #Abalance 11/

RESTRICTIONS (again), INVESTIGATIONS & EMPLOYEES

Bizzarely: #Abalance seems to muddle already addressed topics into an even less coherent response 12/

Bizzarely: #Abalance seems to muddle already addressed topics into an even less coherent response 12/

#Abalance state that its legal counsel and experts have provided appropriate explanations and responses the US DoC. As already discussed, this is patently untrue. The DoC have been extremely clear that VSUN’s submissions did not constitute an acceptable response. 13/

#Abalance then bizarrely state that they are also complying with a Department of Justice (DoJ) investigation. We applaud the transparency (or faux pas) but to brag about complying with a previously unknown DoJ investigation is a weird PR tactic. 14/

#Abalance does not see a problem with having large concentrations of employees in China. We note that despite adverse findings regarding its compliance by the DoC: VSUN sales managers based in China appear to actively advertise that VSUN can circumvent AD/CVD orders. 15/

CSUN RELATIONSHIP

#Abalance deny that there is any current relationship between them and CSUN.

This is an absurd hill to die on, and an unacceptable response from management. There are various well-documented links between VSUN and CSUN. 16/

#Abalance deny that there is any current relationship between them and CSUN.

This is an absurd hill to die on, and an unacceptable response from management. There are various well-documented links between VSUN and CSUN. 16/

JUNE 2024 COMPLIANCE

#Abalance acknowledge our concern that VSUN products are non-compliant and will be found in breach of AD/CVD orders post a grace period allowed by President Biden.

Abalance management completely deny this will be an issue. 17/

#Abalance acknowledge our concern that VSUN products are non-compliant and will be found in breach of AD/CVD orders post a grace period allowed by President Biden.

Abalance management completely deny this will be an issue. 17/

This grace period is intended to not negatively affect live projects and give project managers in the USA time to source compliant modules.

Being found non-compliant by the DoC, VSUN will face enormous duties or be restricted from trading in the USA. #Abalance 18/

Being found non-compliant by the DoC, VSUN will face enormous duties or be restricted from trading in the USA. #Abalance 18/

Our original report can be found here:

viceroyresearch.org/2023/05/16/aba…

We stand by our findings and reiterate our belief that #Abalance is uninvestible.

More to come. 19/19

viceroyresearch.org/2023/05/16/aba…

We stand by our findings and reiterate our belief that #Abalance is uninvestible.

More to come. 19/19

• • •

Missing some Tweet in this thread? You can try to

force a refresh